MoneyGram 2008 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2008 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

Table of Contents

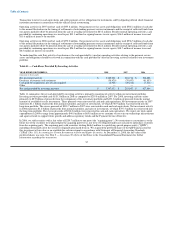

CRITICAL ACCOUNTING POLICIES

The preparation of financial statements in conformity with GAAP requires estimates and assumptions that affect the reported amounts of

assets and liabilities, revenues and expenses, and related disclosures in the Consolidated Financial Statements. Actual results could differ

from those estimates. On a regular basis, management reviews its accounting policies, assumptions and estimates to ensure that our

financial statements are presented fairly and in accordance with GAAP.

Critical accounting policies are those policies that management believes are most important to the portrayal of our financial position and

results of operations, and that require management to make estimates that are difficult, subjective or complex. Based on these criteria,

management has identified and discussed with the Audit Committee the following critical accounting policies and estimates, including

the methodology and disclosures related to those estimates. See Note 3 — Summary of Significant Accounting Policies of the Notes to

Consolidated Financial Statements for a comprehensive list of our accounting policies.

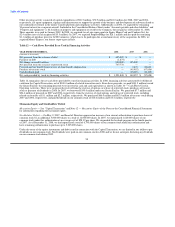

Fair Value of Investment Securities — We hold investment securities classified as trading and available-for-sale. Trading securities are

recorded at fair value, with unrealized gains and losses reported in the Consolidated Statements of (Loss) Income. Available-for-sale

securities are also recorded at fair value, with unrealized gains and losses recorded net of tax in accumulated other comprehensive income

in stockholders' deficit.

We measure fair value in accordance with SFAS No. 157, Fair Value Measurements, which defines fair value as an "exit price," or the

exchange price that would be received for an asset or paid to transfer a liability in an orderly transaction between market participants on

the measurement date. SFAS No. 157 establishes a three-level hierarchy for fair value measurements based upon the observability of the

inputs to the valuation of an asset or liability, and requires that the use of observable inputs be maximized and the use of unobservable

inputs be minimized. The fair value hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets

or liabilities and the lowest priority to unobservable inputs.

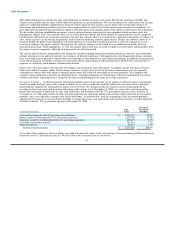

The degree of management judgment involved in determining the fair value of an investment is dependent upon the availability of quoted

market prices or observable market parameters. Fair value for the majority of our investments is estimated using quoted market prices in

active markets, broker quotes or industry-standard models that utilize independently sourced market parameters. These independently

sourced market parameters are observable in the marketplace, can be derived from observable data or are supported by observable levels

at which transactions for similar securities are executed in the marketplace. Examples of such parameters include, but are not limited to,

interest rate yield curves, reported trades, broker or dealer quotes, issuer spreads, benchmark securities, bids, offers and reference data.

We receive prices from an independent pricing service for the vast majority of the fair value of our trading and available-for-sale

investments. We verify these prices through periodic internal valuations, as well as through comparison to comparable securities, any

broker quotes received and liquidation prices. The independent pricing service will only provide a price for an investment if there is

sufficient observable market information to obtain objective pricing. We receive prices from an independent pricing service for

investments classified as obligations of states and political subdivisions, commercial mortgage-backed securities, residential mortgage-

backed securities, U.S. government agencies, corporate debt securities, preferred and common stock and certain other asset- backed

securities.

For investments that are not actively traded, or for which there is not sufficient observable market information, we estimate fair value

using broker quotes when available. When such quotes are not available, as well as to verify broker quotes received, we estimate fair

value using industry-standard pricing models, discount margins for comparable securities adjusted for differences in our security, risk and

liquidity premiums observed in the market place, default rates, prepayment speeds, loss severity and information specific to the

underlying collateral to the investment. We maximize the use of market observable information to the extent possible and make our best

estimate of the assumptions that a similar market participant would make. Investments which are primarily valued through the use of

broker quotes or internal valuations include those classified as other asset-backed securities and certain commercial mortgage-backed

securities.

65