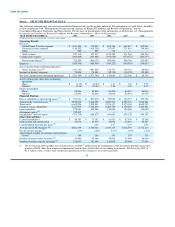

MoneyGram 2008 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2008 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

Table of Contents

focusing on initiatives designed to lower costs of international remittances which, if implemented, may adversely impact our business,

financial position and results of operations.

Any intentional or negligent violation by us of the laws and regulations set forth above could lead to significant fines or penalties and

could limit our ability to conduct business in some jurisdictions. Regulators in the United States and other jurisdictions are showing a

greater inclination than they have in the past to hold money services businesses like ours to higher standards of agent training and

monitoring for possible violations of laws and regulations by agents. Our systems, employees and processes may not be sufficient to

detect and prevent an intentional or negligent violation of the laws and regulations set forth above by our agents which could also lead to

us being subject to significant fines or penalties. In addition to those direct costs, a failure by us or our agents to comply with applicable

laws and regulations also could seriously damage our reputation and brands and result in diminished revenue and profit and increased

operating costs.

In connection with the Capital Transaction, we recognized significant losses in our investment portfolio. As a result, we were not in

compliance for a brief period of time with the minimum net worth requirements of the states in which we are licensed to conduct our

money transfer and other payment services businesses, as well as certain other requirements of one state. This failure to meet minimum

net worth or other requirements may result in certain states imposing fines and other penalties in the future.

Changes in laws, regulations or other industry practices and standards, or interpretations of legal or regulatory requirements may occur

which could increase our compliance and other costs of doing business, require significant systems redevelopment, reduce the market for

or value of our products or services or render our products or services less profitable or obsolete and have an adverse effect on our results

of operations. Changes in the laws affecting the kinds of entities that are permitted to act as money transfer agents (such as changes in

requirements for capitalization or ownership) could adversely effect our ability to distribute our services and the cost of providing such

services, both by us and our agents. Many of our high volume agents are in the check cashing industry. Any regulatory action that

adversely affects check cashers could also cause this portion of our agent base to decline. If onerous regulatory requirements were

imposed on our agents, the requirements could lead to a loss of agents, which, in turn, could lead to a loss of retail business.

Failure by us or our agents to comply with the laws and regulatory requirements of applicable regulatory authorities could result in,

among other things, revocation of required licenses or registrations, loss of approved status, termination of contracts with banks or retail

representatives, administrative enforcement actions and fines, class action lawsuits, cease and desist orders and civil and criminal

liability. The occurrence of one or more of these events could have a material adverse effect on our business, financial condition and

results of operations.

We conduct money transfer transactions through agents in some regions that are politically volatile or, in a limited number of cases,

are subject to certain OFAC restrictions.

We conduct money transfer transactions through agents in some regions that are politically volatile or, in a limited number of cases, are

subject to certain OFAC restrictions. While we have instituted policies and procedures to protect against violations of law, it is possible

that our money transfer service or other products could be used by wrong-doers in contravention of U.S. law or regulations. In addition to

monetary fines or penalties that we could incur, we could be subject to reputational harm that could adversely impact the value of our

stockholders' investments.

We face security risks related to our electronic processing and transmission of confidential customer information. A material breach

of security of our systems could adversely affect our business.

Any significant security or privacy breaches in our facilities, computer networks and databases could harm our business and reputation,

cause inquiries and fines or penalties from regulatory or governmental authorities and cause a loss of customers. We discovered an

unlawful data server attack and suffered potential improper data access by unauthorized persons in late 2006. We rely on encryption

software and other technologies to provide security for processing and transmission of confidential customer information. Advances in

computer capabilities, new discoveries in the field of cryptography or other events or developments, including improper acts by third

parties, may result in a compromise or breach of the security measures we use to protect customer transaction data. We may

20