MoneyGram 2008 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2008 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

Table of Contents

MONEYGRAM INTERNATIONAL, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

as Level 3. If no broker quote is available, or if such quote cannot be corroborated by market data or internal valuations, the Company

will perform internal valuations utilizing externally developed cash flow models. These pricing models are based on market observable

spreads and, when available, observable market indices. The pricing models also use inputs such as the rate of future prepayments and

expected default rates on the principal, which are derived by the Company based on the characteristics of the underlying structure and

historical prepayment speeds experienced at the interest rate levels projected for the underlying collateral. The pricing models for certain

asset-backed securities also include significant non-observable inputs such as internally assessed credit ratings for non-rated securities

combined with externally provided credit spreads. Observability of market inputs to the valuation models used for pricing certain of the

Company's investments has deteriorated with the disruption to the credit markets as overall liquidity and trading activity in these sectors

has been substantially reduced. Accordingly, securities valued using a pricing model have consistently been classified as Level 3 financial

instruments since January 1, 2008.

Derivatives and Other Financial Instruments — Derivatives and other financial instruments consist of interest rate swaps, foreign

currency forward contracts and embedded derivatives contained in the Series B Stock and the put options related to trading investments.

As the Company's derivative agreements are not exchange traded, the valuations are determined using pricing models with inputs that are

observable in the market or that can be derived principally from, or corroborated by, observable market data. The Company's derivative

agreements related to interest rate swaps and foreign currency forward contracts are well-established products, allowing the use of pricing

models that are widely accepted in the industry. These models reflect the contractual terms of the derivatives, including the period to

maturity, and market-based parameters such as the price of the Company's common stock, interest rates, volatility, credit spreads and the

credit quality of the counterparty. For the interest rate swaps and forward contracts, these models do not contain a high level of

subjectivity as the methodologies used in the models do not require significant judgment and the inputs are readily observable.

Accordingly, the Company has classified its interest rate swaps and forward contracts as Level 2 financial instruments. The fair value of

the embedded derivatives are estimated using a partial differential equation methodology and, to the extent possible, market observable or

market corroborated data. However, certain assumptions, particularly the future volatility of the Company's common stock price, are

subjective as market data is either unobservable or may not be available on a consistent basis. Given the significance of the future

volatility to the fair value estimate, the Company has classified its embedded derivatives as Level 3 financial instruments. The fair value

of the put options related to trading investments is valued using the expected cash flows from the instruments assuming their exercise in

June 2010 and discounted at a rate corroborated by market data for a financial institution comparable to the put option counter-party, as

well as the Company's interest rate on its Notes. The discounted cash flows of the put option are then reduced by the estimated fair value

of the trading investments. Given the subjectivity of the discount rate and the estimated fair value of the trading investments, the

Company has classified its put options related to trading investments as Level 3 financial instruments. The Company has elected under

FAS 159, The Fair Value Option for Financial Assets and Financial Liabilities, to apply fair value accounting to its put options relating

to trading investments. As a result, the fair value of the put options will be remeasured each period, with the change in fair value

recognized in earnings.

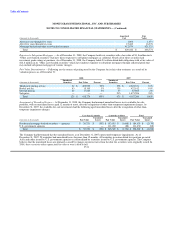

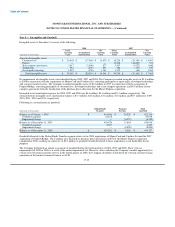

Following are the Company's financial assets which are recorded at fair value by SFAS No. 157 hierarchy level as of December 31, 2008;

the Company had no financial liabilities recorded at fair value as of December 31, 2008. The amount shown as "Cash equivalents

(substantially restricted)" does not reflect the entire balance in the "Cash and cash equivalents" line in the Consolidated Balance Sheets as

cash is not subject to fair value measurement.

F-25