United Airlines 2010 Annual Report Download - page 125

Download and view the complete annual report

Please find page 125 of the 2010 United Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

|

|

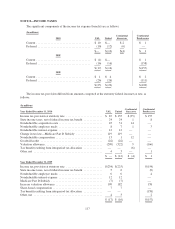

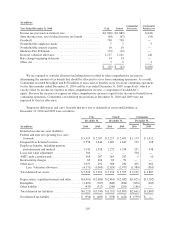

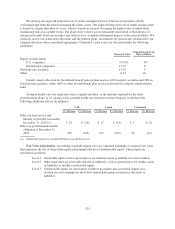

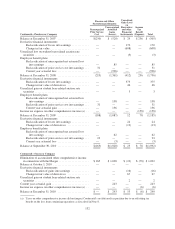

Net periodic benefit cost for the years ended December 31, included the following components (in millions):

2010

Pension Benefits Other Postretirement Benefits

UAL United

Continental

Successor

Continental

Predecessor UAL United

Continental

Successor

Continental

Predecessor

Service cost ...................... $27 $ 6 $ 21 $ 50 $ 33 $ 30 $ 3 $ 7

Interest cost ...................... 51 9 42 119 120 116 4 10

Expected return on plan assets ....... (39) (9) (30) (82) (2) (2) — —

Curtailment gain .................. (7) — (7) — — — — —

Amortization of prior service cost

(credit) ....................... (2) (2) — 7 — — — 16

Special termination benefits ......... 4 — 4 — — — — —

Amortization of unrecognized actuarial

(gain) loss ..................... 1 1 — 65 (12) (12) — (3)

Net periodic benefit cost ............ $35 $ 5 $ 30 $159 $139 $132 $ 7 $ 30

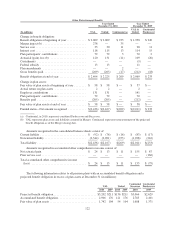

2009 2008

Pension Benefits

Other

Postretirement

Benefits Pension Benefits

Other

Postretirement

Benefits

UAL &

United

Continental

Predecessor

UAL &

United

Continental

Predecessor

UAL &

United

Continental

Predecessor

UAL &

United

Continental

Predecessor

Service cost ............ $ 6 $ 65 $ 28 $ 11 $ 6 $ 59 $ 32 $ 12

Interest cost ............ 8 153 114 15 8 149 122 15

Expected return on plan

assets ............... (7) (89) (4) — (10) (157) (4) —

Curtailment gain ........ (1) — (9) — — — (1) —

Amortization of prior

service cost .......... — 10 — 21 — 10 — 21

Amortization of

unrecognized actuarial

(gain) loss ........... 2 111 (20) (2) (2) 34 (17) (1)

Net periodic benefit

cost ................ $ 8 $250 $109 $ 45 $ 2 $ 95 $132 $ 47

Settlement charges

(included in special

items) ............... — 29 — — — 52 — —

Net benefit expense ...... $ 8 $279 $109 $ 45 $ 2 $ 147 $132 $ 47

The Continental settlement charges in 2009 and 2008, which were classified as special items, are non-cash

charges related to lump sum distributions from the Continental pilot-only defined benefit pension plan to pilots

who retired. Settlement accounting is required if, for a given year, the cost of all settlements exceeds, or is

expected to exceed, the sum of the service cost and interest cost components of net periodic pension expense for

a plan. Under settlement accounting, unrecognized plan gains or losses must be recognized immediately in

proportion to the percentage reduction of the plan’s projected pension benefit obligation.

123