SunTrust 2004 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2004 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

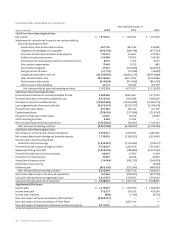

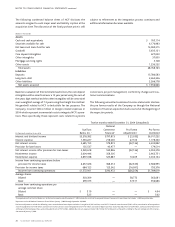

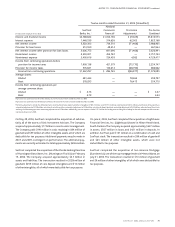

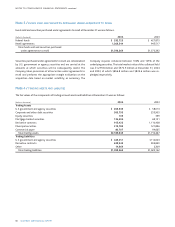

76 SUNTRUST 2004 ANNUAL REPORT

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS continued

stock-based employee compensation plan are included in Note 16

to the Consolidated Financial Statements.

ACCOUNTING POLICIES ADOPTED

In December 2003, the FASB issued Interpretation (FIN) No. 46

(Revised),“Consolidation of Variable Interest Entities, an Interpre-

tation of ARB No. 51” (FIN 46(R)). FIN 46(R) addresses consolida-

tion by business enterprises of VIEs and revises FIN 46 to provide

different implementation dates based on the types of entities sub-

ject to the Interpretation and based on whether a company had

adopted FIN 46. The Interpretation is based on the concept that an

enterprise controlling another entity through interests other than

voting interests should consolidate the controlled entity. An enter-

prise that holds a majority of the variable interests is considered the

primary beneficiary and would consolidate the VIE. The Company

adopted FIN 46(R) as of March 31, 2004, and the adoption did not

have a material impact on the Company’s financial position or

results of operations. The required disclosures related to the

Company’s significant variable interests in VIEs are included in Note

17 to the Consolidated Financial Statements.

In March 2004, the Securities Exchange Commission (SEC) Staff

issued Staff Accounting Bulletin (SAB) No. 105, “Application of

Accounting Principles to Loan Commitments,” which addresses the

accounting treatment for loan commitments accounted for as

derivative instruments. Interest rate lock commitments (IRLCs) rep-

resent commitments to extend credit at specified interest rates. In

the normal course of business, the Company enters into derivatives,

consisting primarily of mortgage-backed security (MBS) forward

sale contracts, to offset the change in value of its IRLCs related to

residential mortgage loans that are intended to be held for sale.

Estimates of the degree to which IRLCs are expected to result in

closed residential mortgage loans are used to determine appropri-

ate levels of MBS forward sale contracts.

The SAB references SFAS No. 149,“Amendment of Statement 133

on Derivative Instruments and Hedging Activities,” as the primary

guidance for IRLC recognition, where IRLCs are classified as deriva-

tive financial instruments.Additionally, Emerging Issues Task Force

(EITF) Issue No. 02-3, “Issues Involved in Accounting for Derivative

Contracts Held for Trading Purposes and Contracts Involved in

Energy Trading and Risk Management Activities,” provides guidance

that the absence of an active exchange or market for derivative

financial instruments renders its recorded value at inception as zero,

with subsequent fair values recorded as assets or liabilities.The esti-

mated fair value of IRLCs is derived from current MBS prices, and no

fair value is recorded at inception with subsequent changes in value

recorded in earnings. Accordingly, the Company accounts for IRLCs

associated with mortgages to be held for sale as freestanding

derivative financial instruments in accordance with SFAS No.

133, as amended by SFAS No. 149, and EITF Issue No. 02-3.

However, originated IRLCs that are intended for investment fall

under SFAS No. 149 paragraph 7(e) and are not treated as derivative

financial instruments.

SAB No. 105 permits the recognition of servicing assets only when

the servicing asset has been contractually separated from the

underlying loan by sale or securitization of the loan where servicing

is retained.Additionally, the SAB prohibits entities from recording

internally-developed intangible assets as part of the loan com-

mitment derivative. SAB No. 105 is effective for mortgage loan

commitments that are accounted for as derivatives and are entered

into after March 31, 2004.The adoption of SAB No. 105 did not have

a material impact on the Company’s financial position or results

of operations.

In May 2004, the FASB issued FASB Staff Position (FSP) No. 106-2,

“Accounting and Disclosure Requirements Related to the Medicare

Prescription Drug, Improvement and Modernization Act of 2003,”

which provides guidance on how companies should account for the

impact of the Medicare Prescription Drug, Improvement and

Modernization Act of 2003 (the “Act”) on its post retirement health

care plans.To encourage employers to retain or provide post retire-

ment drug benefits, beginning in 2006 the federal government will

provide non-taxable subsidy payments to employers that sponsor

prescription drug benefits to retirees that are “actuarially equiva-

lent” to the Medicare benefit. The Company has determined,

through independent third party consultation, that its post retire-

ment health care plans’ prescription drug benefits are actuarially

equivalent to Medicare Part D benefits to be provided under the Act.

The Company adopted the provisions of the FSP effective July 1,

2004, based on a remeasurement of the accumulated post

retirement benefit obligation (“APBO”) as of January 1, 2004.The

adoption of the FSP did not have a material impact on the

Company’s financial position or results of operations.The required

disclosures related to the Company’s APBO and net periodic post

retirement benefit cost are included in Note 16 to the Consolidated

Financial Statements.

RECENTLY ISSUED ACCOUNTING PRONOUNCEMENTS

In December 2003, the American Institute of Certified Public

Accountants (AICPA) issued Statement of Position (SOP) 03-3,

“Accounting for Loans or Certain Debt Securities Acquired in a

Transfer.” The SOP addresses the accounting for differences

between contractual cash flows and cash flows expected to be col-

lected from an investor’s initial investment in loans or debt securi-

ties acquired in a transfer if those differences relate to a

deterioration of credit quality. The SOP also prohibits companies

from “carrying over” or creating a valuation allowance in the initial

accounting for loans acquired that meet the scope criteria of the

SOP.The SOP is effective for loans acquired in fiscal years beginning

after December 15, 2004.The adoption of this SOP is not expected

to have a material impact on the Company’s financial position or

results of operations.

In March 2004, the EITF reached a consensus on EITF Issue No. 03-1,

“The Meaning of Other-Than-Temporary Impairment and Its

Application to Certain Investments.”The Issue provides guidance for

evaluating whether several types of investments, including debt

securities classified as held to maturity and available for sale under

SFAS 115, “Accounting for Certain Investments in Debt and Equity