SunTrust 2004 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2004 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

MANAGEMENT’S DISCUSSION continued

SUNTRUST 2004 ANNUAL REPORT 21

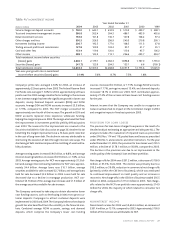

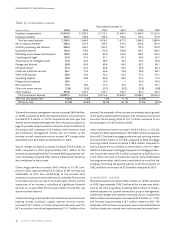

ALLOWANCE FOR LOAN AND LEASE LOSSES

The ALLL represents the ALLL Committee’s estimate of probable

losses inherent in the existing loan portfolio. The ALLL is increased

by the provision for loan losses charged to expense and reduced by

loans charged off, net of recoveries. The ALLL is determined based

on management’s assessment of reviews and evaluations of larger

loans that meet the Company’s definition of impairment and the

size and current risk characteristics of pools of homogeneous loans,

i.e., loans having similar characteristics, within the portfolio.

Impaired loans include loans classified as nonaccrual, except for

smaller balance homogeneous loans, where it is probable that

SunTrust will be unable to collect the scheduled payments of princi-

pal and interest according to the contractual terms of the loan

agreement. When a loan is deemed impaired, the amount of

allowance required is measured by a careful analysis of the most

probable source of repayment, including the present value of the

loan’s expected future cash flow, the fair value of the underlying

collateral less costs of disposition, or the loan’s estimated market

value. In these measurements, management uses assumptions and

methodologies that are relevant to estimating the level of impaired

and unrealized, but inherent, losses in the portfolio. To the extent

that the data supporting such assumptions and methodologies are

continuously evolving, management’s judgement and experience

play a key roll in enhancing the ALLL process over time.

The ALLL Committee estimates probable losses inherent in pools of

loans that have similar characteristics by an evaluation of several

factors: historical loss experience, current internal risk ratings based

on the Company’s internal risk rating system, internal portfolio

trends such as increasing or decreasing levels of delinquencies and

concentrations, and external influences such as changes in eco-

nomic or industry conditions.

The Company’s financial results are substantially influenced by the

Company’s process for determining an appropriate level for its ALLL.

This process involves management’s analysis of complex internal

and external variables, and it requires that management exercise

subjective judgment to estimate an appropriate reserve level. As a

result of the uncertainty associated with this subjectivity, the

Company cannot assure the precision of the amount reserved,

should it experience sizeable loan or lease losses in any particular

period. For example, changes in the financial condition of individual

borrowers, economic conditions, historical loss experience, or the

condition of various markets in which collateral may be sold could

require the Company to significantly decrease or increase the level

of the ALLL and the associated provision for loan losses. Such an

adjustment could materially benefit or adversely affect net income.

For additional discussion of the allowance for loan and lease losses

see pages 31 through 34.

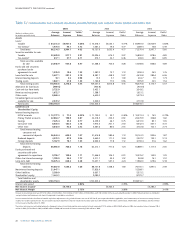

ESTIMATES OF FAIR VALUE

Fair value is defined as the amount at which a financial instrument

could be exchanged in a transaction between willing, unrelated par-

ties in a normal business transaction. The estimation of fair value is

significant to a number of SunTrust’s assets, including loans held for

sale, investment securities, mortgage servicing rights (MSRs), other

real estate owned (OREO), other repossessed assets, as well as

assets and liabilities associated with derivative financial instru-

ments. These are all recorded at either fair value or at the lower of

cost or fair value.

Fair value is based on quoted market prices for the same instrument

or for similar instruments adjusted for any differences in terms. If

market prices are not available, then fair value is estimated using

modeling techniques such as discounted cash flow analyses. In

instances where required by GAAP, the Company uses discount rates

in its determination of the fair value of certain assets and liabilities

such as retirement and postretirement benefit obligations and

mortgage servicing rights. The fair values of mortgage servicing

rights are based on discounted cash flow analyses utilizing dealer

consensus prepayment speeds and market discount rates.A change

in the discount rate could increase or decrease the values of those

assets and liabilities. Discount rates used are those considered to be

commensurate with the risks involved.

Investment securities and most derivative financial instruments are

based on quoted market prices. If quoted market prices are not

available, fair values are based on the quoted prices of similar instru-

ments.The fair values of loans held for sale are based on anticipated

liquidation values.The fair values of other real estate owned and

other repossessed assets are typically determined based on

appraisals by third parties, less estimated selling costs. Changes in

the assumptions used to value these assets and liabilities such as

prepayment speeds or interest market rates could result in an

increase or decrease in fair value and could result in either a benefi-

cial or adverse impact on the financial results.

Estimates of fair value are also required in performing an impair-

ment analysis of goodwill. The Company reviews goodwill for

impairment on an annual basis, or more often if events or circum-

stances indicate the carrying value may not be recoverable. An

impairment would be indicated if the carrying value of goodwill of a

reporting unit exceeds the fair value of a reporting unit. In deter-

mining the fair value of SunTrust’s reporting units, management

uses discounted cash flow models which require assumptions about

the Company’s revenue growth rate and the cost of equity.

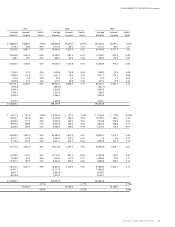

RECENT ACCOUNTING DEVELOPMENTS

The Company adopted the provisions of several new accounting

pronouncements in the current year, including Financial Accounting

Standards Board Interpretation (FIN) No. 46(R), FASB Staff Position

(FSP) No. 106-2, Staff Accounting Bulletin (SAB) No. 105, and the

effective provisions of EITF Issue No. 03-1. The provisions of these

pronouncements and the related impact to the Company are dis-

cussed in the Accounting Policies Adopted section of Note 1 to the

Consolidated Financial Statements beginning on page 73.