SunTrust 2004 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2004 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

44 SUNTRUST 2004 ANNUAL REPORT

MANAGEMENT’S DISCUSSION continued

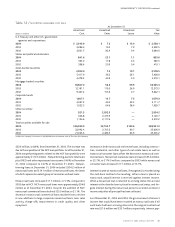

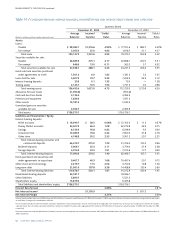

Net short-term unsecured borrowings, including wholesale domes-

tic and foreign deposits and fed funds, totaled $16.5 billion and

$15.9 billion at December 31, 2004 and 2003, respectively.

Commercial paper related to Three Pillars, which was consolidated

during the third quarter of 2003 and deconsolidated during the first

quarter of 2004, was $3.2 billion at December 31, 2003. Mortgage

refinance activity during the last few years has influenced the bal-

ance of loans held for sale, which has been funded using short-term

unsecured borrowings. Refinance activity slowed in 2004 relative to

2003 with production of $30.8 billion and $43.7 billion, respec-

tively. However, the production in the fourth quarter of 2004 was

$8.5 billion compared to $6.3 billion in the same period last year.

The balance of loans held for sale was $6.6 billion and $5.6 billion at

December 31, 2004 and December 31, 2003, respectively.

The Company maintains access to a diversified base of wholesale

funding sources.These sources include fed funds purchased, securi-

ties sold under agreements to repurchase, negotiable certificates of

deposit, offshore deposits, Federal Home Loan Bank advances,

Global Bank Note issuance and commercial paper issuance.As of

December 31, 2004, SunTrust Bank had $14.3 billion remaining

under its Global Bank Note program.This capacity reflects $1.5 bil-

lion of senior debt issued during the first quarter of 2004, $350 mil-

lion of subordinated debt issued during the fourth quarter of 2004,

and a $10 billion increase to the program, completed on March 31,

2004. The Global Bank Note program was established to expand

funding and capital sources to include both domestic and interna-

tional investors. Liquidity is also available through unpledged secu-

rities in the investment portfolio and capacity to securitize loans,

including single-family mortgage loans.The Company’s credit rat-

ings are important to its access to unsecured wholesale borrowings.

Significant changes in these ratings could change the cost and avail-

ability of these sources.The Company manages reliance on short-

term unsecured borrowings as well as total wholesale funding

through policies established and reviewed by ALCO.

The Company has a contingency funding plan that stresses the liq-

uidity needs that may arise from certain events such as agency rat-

ing downgrades, rapid loan growth, or significant deposit runoff.The

plan also provides for continual monitoring of net borrowed funds

dependence and available sources of liquidity. Management

believes the Company has the funding capacity to meet the liquid-

ity needs arising from potential events.

Liquidity for the Parent Company is measured comparing sources of

liquidity in unpledged securities and short-term investments rela-

tive to its short-term debt. As of December 31, 2004, the Parent

Company had $978 million in such sources compared to short-term

debt of $534 million.The Parent Company also has $1.5 billion of

availability remaining on its current shelf registration statement for

the issuance of debt. As discussed in Note 14 to the Consolidated

Financial Statements, subsidiary banks are subject to regulation

that may limit their ability to pay dividends to their holding com-

pany.The Georgia Department of Banking and Finance limits divi-

dends to 50% of the subsidiary banks’ prior year’s net income,

without its prior approval. SunTrust Bank has exceeded this limita-

tion since 2000 and has received the necessary approvals for divi-

dends beyond this amount. Additionally, the subsidiary banks are

limited under Federal regulations based on the prior two years’ net

retained earnings plus the current year’s net retained earnings.

During 2005, the subsidiary banks can pay $544 million, plus the

current year’s earnings without prior approval from the appropriate

regulatory agency. Subsequent to December 31, 2004, National

Bank of Commerce (NBC) utilized $150 million of this dividend

capacity as part of the legal reorganization of other certain NCF

subsidiaries.

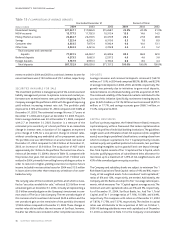

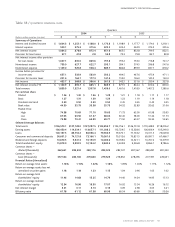

As detailed in Table 17, the Company had $77.0 billion in total com-

mitments to extend credit at December 31, 2004 that were not

recorded on the Company’s balance sheet. Commitments to extend

credit are arrangements to lend to a customer who has complied

with predetermined contractual obligations.The Company also had

$11.1 billion in letters of credit as of December 31, 2004, most of

which are standby letters of credit that provide that SunTrust Bank

fund if certain future events occur.Of this, approximately $5.6 bil-

lion support variable-rate demand obligations (VRDOs) remarketed

by SunTrust and other agents.VRDOs are municipal securities which

are remarketed by the agent on a regular basis, usually weekly. In

the event that the securities are unable to be remarketed, SunTrust

Bank would fund under the letters of credit.

Certain provisions of long-term debt agreements and the lines of

credit prevent the Company from creating liens on, disposing of, or

issuing (except to related parties) voting stock of subsidiaries.

Further, there are restrictions on mergers, consolidations, certain

leases, sales or transfers of assets, and minimum shareholders’

equity ratios. As of December 31, 2004, the Company was in com-

pliance with all covenants and provisions of these debt agreements.

OFF-BALANCE SHEET ARRANGEMENTS

In the normal course of business, the Company engages in financial

transactions that, in accordance with GAAP, are either not recorded

on the Company’s balance sheet or may be recorded on the

Company’s balance sheet at an amount that differs from the full

contract or notional amount of the transaction.These transactions

are structured to meet the financial needs of customers, manage

the Company’s credit, market or liquidity risks, diversify funding

sources, or optimize capital.

As a financial services provider, the Company routinely enters into

commitments to extend credit, including, but not limited to, loan

commitments, financial and performance standby letters of credit

and financial guarantees.While these contractual obligations could

potentially result in material current or future effects on financial

condition, results of operations, liquidity, capital expenditures, capi-

tal resources, or significant components of revenues or expenses,

based on historical experience, a significant portion of commit-

ments to extend credit expire without being drawn upon. Such

commitments are subject to the same credit policies and approval