MetLife 2003 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2003 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

|

|

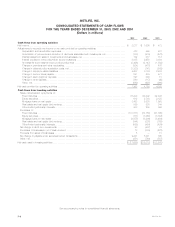

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Summary of Accounting Policies

Business

‘‘MetLife’’ or the ‘‘Company’’ refers to MetLife, Inc., a Delaware corporation (the ‘‘Holding Company’’), and its subsidiaries, including Metropolitan Life

Insurance Company (‘‘Metropolitan Life’’) is a leading provider of insurance and other financial services to a broad spectrum of individual and institutional

customers. The Company offers life insurance, annuities, automobile and homeowners insurance and mutual funds to individuals, as well as group

insurance, reinsurance and retirement and savings products and services to corporations and other institutions.

Basis of Presentation

The accompanying consolidated financial statements include the accounts of (i) the Holding Company and its subsidiaries: (ii) partnerships and joint

ventures in which the Company has a majority voting interest; and (iii) variable interest entities (‘‘VIEs’’) created or acquired on or after February 1, 2003 of

which the Company is deemed to be the primary beneficiary. Closed block assets, liabilities, revenues and expenses are combined on a line by line basis

with the assets, liabilities, revenues and expenses outside the closed block based on the nature of the particular item. See Note 6. Intercompany

accounts and transactions have been eliminated.

The Company uses the equity method of accounting for investments in real estate joint ventures and other limited partnership interests in which it

has more than a minor equity interest or more than minor influence over the partnership’s operations, but does not have a controlling interest. The

Company uses the cost method of accounting for interests in which it has a minor equity investment and virtually no influence over the partnership’s

operations.

Minority interest related to consolidated entities included in other liabilities was $950 million and $491 million at December 31, 2003 and 2002,

respectively. This increase was the direct result of the change in MetLife’s ownership of RGA to approximately 52% in 2003 compared to 59% in 2002.

Certain amounts in the prior years’ consolidated financial statements have been reclassified to conform with the 2003 presentation.

Summary of Critical Accounting Estimates

The preparation of financial statements in conformity with GAAP requires management to adopt accounting policies and make estimates and

assumptions that affect amounts reported in the consolidated financial statements. The critical accounting policies, estimates and related judgments

underlying the Company’s consolidated financial statements are summarized below. In applying these policies, management makes subjective and

complex judgments that frequently require estimates about matters that are inherently uncertain. Many of these policies, estimates and related judgments

are common in the insurance and financial services industries; others are specific to the Company’s businesses and operations.

Investments

The Company’s principal investments are in fixed maturities, mortgage loans and real estate, all of which are exposed to three primary sources of

investment risk: credit, interest rate and market valuation. The financial statement risks are those associated with the recognition of impairments and

income, as well as the determination of fair values. The assessment of whether impairments have occurred is based on management’s case-by-case

evaluation of the underlying reasons for the decline in fair value. Management considers a wide range of factors about the security issuer and uses its

best judgment in evaluating the cause of the decline in the estimated fair value of the security and in assessing the prospects for near-term recovery.

Inherent in management’s evaluation of the security are assumptions and estimates about the operations of the issuer and its future earnings potential.

Considerations used by the Company in the impairment evaluation process include, but are not limited to: (i) the length of time and the extent to which the

market value has been below cost; (ii) the potential for impairments of securities when the issuer is experiencing significant financial difficulties; (iii) the

potential for impairments in an entire industry sector or sub-sector; (iv) the potential for impairments in certain economically depressed geographic

locations; (v) the potential for impairments of securities where the issuer, series of issuers or industry has suffered a catastrophic type of loss or has

exhausted natural resources; (vi) unfavorable changes in forecasted cash flows on asset-backed securities; and (vii) other subjective factors, including

concentrations and information obtained from regulators and rating agencies. In addition, the earnings on certain investments are dependent upon market

conditions, which could result in prepayments and changes in amounts to be earned due to changing interest rates or equity markets. The determination

of fair values in the absence of quoted market values is based on: (i) valuation methodologies; (ii) securities the Company deems to be comparable; and

(iii) assumptions deemed appropriate given the circumstances. The use of different methodologies and assumptions may have a material effect on the

estimated fair value amounts. In addition, the Company enters into certain structured investment transactions, real estate joint ventures and limited

partnerships for which the Company may be deemed to be the primary beneficiary and, therefore, may be required to consolidate such investments. The

accounting rules for the determination of the primary beneficiary are complex and require evaluation of the contractual rights and obligations associated

with each party involved in the entity, an estimate of the entity’s expected losses and expected residual returns and the allocation of such estimates to

each party.

Derivatives

The Company enters into freestanding derivative transactions primarily to manage the risk associated with variability in cash flows or changes in fair

values related to the Company’s financial assets and liabilities or to changing fair values. The Company also uses derivative instruments to hedge its

currency exposure associated with net investments in certain foreign operations. The Company also purchases investment securities, issues certain

insurance policies and engages in certain reinsurance contracts that embed derivatives. The associated financial statement risk is the volatility in net

income which can result from (i) changes in fair value of derivatives not qualifying as accounting hedges; (ii) ineffectiveness of designated hedges; and

(iii) counterparty default. In addition, there is a risk that embedded derivatives requiring bifurcation are not identified and reported at fair value in the

consolidated financial statements. Accounting for derivatives is complex, as evidenced by significant authoritative interpretations of the primary

accounting standards which continue to evolve, as well as the significant judgments and estimates involved in determining fair value in the absence of

quoted market values. These estimates are based on valuation methodologies and assumptions deemed appropriate in the circumstances. Such

assumptions include estimated volatility and interest rates used in the determination of fair value where quoted market values are not available. The use of

different assumptions may have a material effect on the estimated fair value amounts.

MetLife, Inc.

F-8