MetLife 2003 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2003 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

|

|

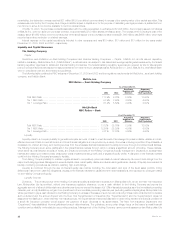

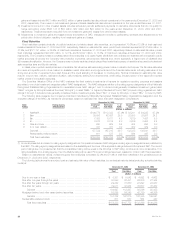

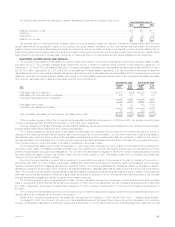

The following table presents the estimated fair value of the Company’s total fixed maturities classified as performing, potential problem, problem and

restructured at:

December 31, 2003 December 31, 2002

Estimated % of Estimated % of

Fair Value Total Fair Value Total

(Dollars in millions)

Performing *********************************************************************** $167,125 99.6% $139,452 99.4%

Potential problem ***************************************************************** 282 0.2 450 0.3

Problem ************************************************************************* 264 0.2 358 0.3

Restructured ********************************************************************* 81 0.0 28 0.0

Total ******************************************************************** $167,752 100.0% $140,288 100.0%

Fixed Maturity Impairment. The Company classifies all of its fixed maturities as available-for-sale and marks them to market through other

comprehensive income. All securities with gross unrealized losses at the consolidated balance sheet date are subjected to the Company’s process for

identifying other-than-temporary impairments. The Company writes down to fair value securities that it deems to be other-than-temporarily impaired in the

period the securities are deemed to be so impaired. The assessment of whether such impairment has occurred is based on management’s case-by-

case evaluation of the underlying reasons for the decline in fair value. Management considers a wide range of factors, as described below, about the

security issuer and uses its best judgment in evaluating the cause of the decline in the estimated fair value of the security and in assessing the prospects

for near-term recovery. Inherent in management’s evaluation of the security are assumptions and estimates about the operations of the issuer and its

future earnings potential.

Considerations used by the Company in the impairment evaluation process include, but are not limited to, the following:

)length of time and the extent to which the market value has been below amortized cost;

)potential for impairments of securities when the issuer is experiencing significant financial difficulties, including a review of all securities of the

issuer, including its known subsidiaries and affiliates, regardless of the form of the Company’s ownership;

)potential for impairments in an entire industry sector or sub-sector;

)potential for impairments in certain economically depressed geographic locations;

)potential for impairments of securities where the issuer, series of issuers or industry has suffered a catastrophic type of loss or has exhausted

natural resources; and

)other subjective factors, including concentrations and information obtained from regulators and rating agencies.

The Company’s review of its fixed maturities for impairments includes an analysis of the total gross unrealized losses by three categories of

securities: (i) securities where the estimated fair value had declined and remained below amortized cost by less than 20%; (ii) securities where the

estimated fair value had declined and remained below amortized cost by 20% or more for less than six months; and (iii) securities where the estimated

value had declined and remained below amortized cost by 20% or more for six months or greater. The first two categories have generally been adversely

impacted by the downturn in the financial markets and overall economic conditions. While all of these securities are monitored for potential impairment,

the Company’s experience indicates that the first two categories do not present as great a risk of impairment, and often, fair values recover over time as

the factors that caused the declines improve.

The Company records writedowns as investment losses and adjusts the cost basis of the fixed maturities accordingly. The Company does not

change the revised cost basis for subsequent recoveries in value. Writedowns of fixed maturities were $338 million and $1,264 million for the years

ended December 31, 2003 and 2002, respectively. The Company’s three largest writedowns totaled $125 million and $352 million for the years ended

December 31, 2003 and 2002, respectively. The circumstances that gave rise to these impairments were either financial restructurings or bankruptcy

filings. During the years ended December 31, 2003 and 2002, the Company sold fixed maturities with a fair value of $30,714 million and $14,597 million

at a loss of $486 million and $894 million, respectively.

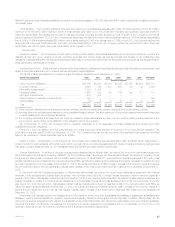

The following table presents the total gross unrealized losses for fixed maturities where the estimated fair value had declined and remained below

amortized cost by:

December 31, 2003

Gross

Unrealized % of

Losses Total

(Dollars in millions)

Less than 20% *************************************************************************************** $677 91.1%

20% or more for less than six months ******************************************************************** 22 3.0

20% or more for six months or greater ******************************************************************* 44 5.9

Total **************************************************************************************** $743 100.0%

The gross unrealized loss related to the Company’s fixed maturities at December 31, 2003 was $743 million. These fixed maturities mature as

follows: 1% due in one year or less; 23% due in greater than one year to five years; 18% due in greater than five years to ten years; and 58% due in

greater than ten years (calculated as a percentage of amortized cost). Additionally, such securities are concentrated by sector in U.S. corporates (34%),

mortgage-backed (17%) and foreign corporates (11%); and are concentrated by industry in mortgage-backed (13%), utilities (12%) and finance (8%)

(calculated as a percentage of gross unrealized loss). Non-investment grade securities represent 6% of the $30,881 million fair value and 20% of the

$743 million gross unrealized loss on fixed maturities.

MetLife, Inc.

32