MetLife 2003 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2003 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

|

|

MetLife Funding had total outstanding liabilities, including accrued interest payable, of $1,042 million and $400 million, respectively, consisting primarily of

commercial paper.

Credit Facilities. The Company maintains committed and unsecured credit facilities aggregating $2.5 billion ($1 billion expiring in 2004, $1.3 billion

expiring in 2005 and $175 million expiring in 2006). If these facilities were drawn upon, they would bear interest at varying rates in accordance with the

respective agreements. The facilities can be used for general corporate purposes and also as back-up lines of credit for the Company’s commercial

paper programs. At December 31, 2003, the Company had drawn approximately $49 million under the facilities expiring in 2005 at interest rates ranging

from 4.08% to 5.48% and approximately $50 million under a facility expiring in 2006 at an interest rate of 1.69%. In April 2003, the Company replaced an

expiring $1 billion five-year credit facility with a $1 billion 364-day credit facility. In May 2003, the Company replaced an expiring $140 million three-year

credit facility with a $175 million three-year credit facility, which expires in 2006.

Liquidity Uses

Insurance Liabilities. The Company’s principal cash outflows primarily relate to the liabilities associated with its various life insurance, property and

casualty, annuity and group pension products, operating expenses and income taxes, as well as principal and interest on its outstanding debt

obligations. Liabilities arising from its insurance activities primarily relate to benefit payments under the aforementioned products, as well as payments for

policy surrenders, withdrawals and loans.

Investment and Other. Additional cash outflows include those related to obligations of securities lending and dollar roll activities, investments in real

estate, limited partnerships and joint ventures, as well as litigation-related liabilities.

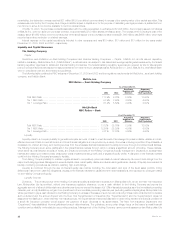

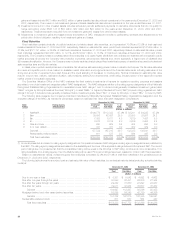

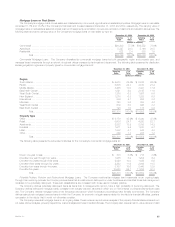

The following table summarizes the Company’s major contractual obligations as of December 31, 2003:

Contractual Obligations Total 2004 2005 2006 2007 2008 Thereafter

(Dollars in millions)

Other long-term liabilities(1)****************************** $87,086 $4,391 $3,812 $3,475 $3,763 $2,934 $68,711

Long-term debt(2) ************************************* 5,646 126 1,413 653 28 32 3,394

Partnership investments(3) ****************************** 1,380 1,380 ———— —

Operating leases ************************************** 1,545 210 192 168 145 113 717

Mortgage commitments ******************************** 679679———— —

Shares subject to mandatory redemption(2)**************** 350—————350

Capital leases***************************************** 74 8 9 10 11 12 24

Total************************************************* $96,760 $6,794 $5,426 $4,306 $3,947 $3,091 $73,196

(1) Other long-term liabilities include guaranteed interest contracts, structured settlements, pension closeouts and certain annuity policies.

(2) Amounts differ from the balances presented on the consolidated balance sheets. The amounts above do not include related premiums and discounts

or capital leases which are presented separately.

(3) The Company anticipates that these amounts could be invested in these partnerships any time over the next five years, but are presented in the

current period, as the timing of the fulfillment of the obligation cannot be predicted.

As of December 31, 2003, the Company had no material, individually or in the aggregate, purchase obligations and pension and other

postretirement benefit obligations.

On April 11, 2003, an affiliate of the Company elected not to make future payments required by the terms of a non-recourse loan obligation. The

book value of this loan was $15 million at December 31, 2003. The Company’s exposure under the terms of the applicable loan agreement is limited

solely to its investment in certain securities held by an affiliate.

Letters of Credit. At December 31, 2003 and 2002, the Company had outstanding approximately $828 million and $625 million, respectively, in

letters of credit from various banks, all of which expire within one year. Since commitments associated with letters of credit and financing arrangements

may expire unused, these amounts do not necessarily reflect the actual future cash funding requirements.

Support Agreements. In addition to the support agreements described above, Metropolitan Life entered into a net worth maintenance agreement

with New England Life Insurance Company (‘‘NELICO’’) at the time Metropolitan Life merged with New England Mutual Life Insurance Company. Under

the agreement, Metropolitan Life agreed, without limitation as to the amount, to cause NELICO to have a minimum capital and surplus of $10 million, total

adjusted capital at a level not less than the company action level RBC, as defined by state insurance statutes, and liquidity necessary to enable it to meet

its current obligations on a timely basis. At December 31, 2003, the capital and surplus of NELICO was in excess of the minimum capital and surplus

amount referenced above, and its total adjusted capital was in excess of the most recent referenced RBC-based amount calculated at December 31,

2003.

In connection with the Company’s acquisition of GenAmerica, Metropolitan Life entered into a net worth maintenance agreement with General

American. Under the agreement, Metropolitan Life agreed, without limitation as to amount, to cause General American to have a minimum capital and

surplus of $10 million, total adjusted capital at a level not less than 180% of the company action level RBC, as defined by state insurance statutes, and

liquidity necessary to enable it to meet its current obligations on a timely basis. The agreement was subsequently amended to provide that, for the five

year period from 2003 through 2007, total adjusted capital must be maintained at a level not less than 200% of the company action level RBC, as

defined by state insurance statutes. At December 31, 2003, the capital and surplus of General American was in excess of the minimum capital and

surplus amount referenced above, and its total adjusted capital was in excess of the most recent referenced RBC-based amount calculated at

December 31, 2003.

Metropolitan Life has also entered into arrangements for the benefit of some of its other subsidiaries and affiliates to assist such subsidiaries and

affiliates in meeting various jurisdictions’ regulatory requirements regarding capital and surplus and security deposits. In addition, Metropolitan Life has

entered into a support arrangement with respect to a subsidiary under which Metropolitan Life may become responsible, in the event that the subsidiary

becomes the subject of insolvency proceedings, for the payment of certain reinsurance recoverables due from the subsidiary to one or more of its

cedents in accordance with the terms and conditions of the applicable reinsurance agreements.

MetLife, Inc. 25