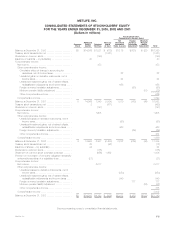

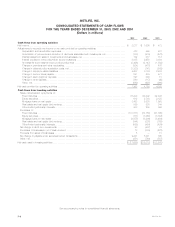

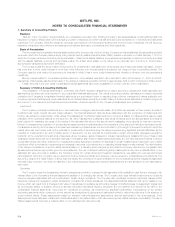

MetLife 2003 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2003 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

|

|

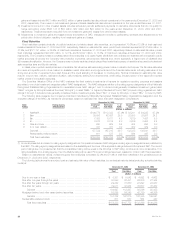

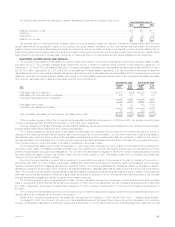

The table below provides a summary of the notional amount and fair value of derivative financial instruments held at December 31, 2003 and 2002:

2003 2002

Current Market Current Market

or Fair Value or Fair Value

Notional Notional

Amount Assets Liabilities Amount Assets Liabilities

(Dollars in millions)

Financial futures ************************************************* $ 1,348 $ 8 $ 30 $ 4 $ — $ —

Interest rate swaps *********************************************** 9,944 189 36 3,866 196 126

Floors ********************************************************** 325 5 — 325 9 —

Caps ********************************************************** 9,345 29 — 8,040 — —

Financial forwards ************************************************ 1,310 2 3 1,945 — 12

Foreign currency swaps******************************************* 4,710 9 796 2,371 92 181

Options ******************************************************** 6,065 7 — 6,472 9 —

Foreign currency forwards ***************************************** 695 5 32 54 — 1

Credit default swaps ********************************************* 615 2 1 376 2 —

Total contractual commitments *********************************** $34,357 $256 $898 $23,453 $308 $320

Variable Interest Entities

The Company has adopted the provisions of FIN 46 and FIN 46(r). See ‘‘— Recent Accounting Standards.’’ At December 31, 2003, FIN 46(r) did

not require the Company to consolidate any additional VIEs that were not previously consolidated.

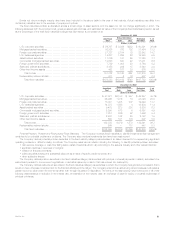

The following table presents the total assets of and maximum exposure to loss relating to VIEs for which the Company has concluded that (i) it is the

primary beneficiary and which will be consolidated in the Company’s financial statements beginning March 31, 2004, and (ii) it holds significant valuable

interests but it is not the primary beneficiary and which will not be consolidated:

December 31, 2003

Primary Not Primary

Beneficiary(1) Beneficiary

Maximum Maximum

Total Exposure Total Exposure

Assets(2) to Loss(3) Assets(2) to Loss(3)

(Dollars in millions)

SPEs:

Asset-backed securitizations and Collateralized debt obligations ****************************** $ — $ — $2,400 $20

Non-SPEs:

Real estate joint ventures(4) ************************************************************ 617 238 42 59

Other limited partnerships(5)************************************************************ 29 27 459 10

Total ***************************************************************************** $646 $265 $2,901 $89

(1) Had the Company consolidated these VIEs at December 31, 2003, the transition adjustments would have been $10 million, net of income tax.

(2) The assets of the asset-backed securitizations and collateralized debt obligations are reflected at fair value as of December 31, 2003. The assets of

the real estate joint ventures and other limited partnerships are reflected at the carrying amounts at which such assets would have been reflected on

the Company’s balance sheet had the Company consolidated the VIE from the date of its initial investment in the entity.

(3) The maximum exposure to loss of the asset-backed securitizations and collateralized debt obligations is equal to the carrying amounts of retained

interests. In addition, the Company provides collateral management services for certain of these structures for which it collects a management fee.

The maximum exposure to loss relating to real estate joint ventures and other limited partnerships is equal to the carrying amounts plus any unfunded

commitments, reduced by amounts guaranteed by other partners.

(4) Real estate joint ventures include partnerships and other ventures, which engage in the acquisition, development, management and disposal of real

estate investments.

(5) Other limited partnerships include partnerships established for the purpose of investing in public and private debt and equity securities, as well as

limited partnerships established for the purpose of investing in low-income housing that qualifies for federal tax credits.

Securities Lending

The Company participates in a securities lending program whereby blocks of securities, which are included in investments, are loaned to third

parties, primarily major brokerage firms. The Company requires a minimum of 102% of the fair value of the loaned securities to be separately maintained

as collateral for the loans. Securities with a cost or amortized cost of $25,121 million and $16,196 million and an estimated fair value of $26,387 million

and $17,625 million were on loan under the program at December 31, 2003 and 2002, respectively. The Company was liable for cash collateral under

its control of $27,083 million and $17,862 million at December 31, 2003 and 2002, respectively. Security collateral on deposit from customers may not

be sold or repledged and is not reflected in the consolidated financial statements.

Separate Account Assets

The Company manages each separate account’s assets in accordance with the prescribed investment policy that applies to that specific separate

account. The Company establishes separate accounts on a single client and multi-client commingled basis in conformity with insurance laws. Generally,

separate accounts are not chargeable with liabilities that arise from any other business of the Company. Separate account assets are subject to the

Company’s general account claims only to the extent that the value of such assets exceeds the separate account liabilities, as defined by the account’s

contract. The Company reports separately as assets and liabilities investments held in separate accounts and liabilities of the separate accounts. The

Company reports substantially all separate account assets at their fair market value. Investment income and gains or losses on the investments of

separate accounts accrue directly to contractholders, and, accordingly, the Company does not reflect them in its consolidated statements of income and

cash flows. The Company reflects in its revenues fees charged to the separate accounts by the Company, including mortality charges, risk charges,

policy administration fees, investment management fees and surrender charges. Effective January 1, 2004, in accordance with new accounting

guidance, approximately $1,678 million of separate account assets will be transferred to investments with a corresponding transfer of separate account

liabilities to future policy benefits and policyholder account balances.

MetLife, Inc.

40