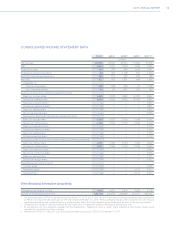

Chrysler 2015 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2015 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

|

|

14 2015 | ANNUAL REPORT

Risk Factors

Risk Factors

We face a variety of risks in our business. The risks and uncertainties described below are not the only ones facing

us. Additional risks and uncertainties that we are unaware of or that we currently believe to be immaterial, may also

become important factors that affect us.

Risks Related to Our Business, Strategy and Operations

Our profitability depends on reaching certain minimum vehicle sales volumes. If our vehicle sales deteriorate,

particularly sales of our pickup trucks, larger utility vehicles and minivans, our results of operations and financial

condition will suffer.

Our success requires us to achieve certain minimum vehicle sales volumes. As is typical for an automotive

manufacturer, we have significant fixed costs and, therefore, changes in vehicle sales volume can have a

disproportionately large effect on our profitability. For example, assuming constant pricing, mix and cost of sales per

vehicle, that all results of operations were attributable to vehicle shipments and that all other variables remain constant,

a ten percent decrease in our 2015 vehicle shipments would reduce our Adjusted Earnings Before Interest and Taxes

(“Adjusted EBIT”) by approximately 29 percent for 2015, without considering actions and cost containment measures

we may take in response to decreased vehicle sales.

In addition, our profitability in the U.S., Canada, Mexico and Caribbean islands (“NAFTA”), a region which contributed

a majority of our profit in 2015, is particularly dependent on demand for our pickup trucks, larger utility vehicles and

minivans. A shift in demand away from these vehicles within the NAFTA region, and towards compact and mid-size

passenger cars, whether in response to higher fuel prices or other factors, could adversely affect our profitability.

Our pickup trucks, larger utility vehicles and minivans accounted for approximately 41 percent of our total U.S. retail

vehicle sales in 2015 and the profitability of this portion of our portfolio is approximately 39 percent higher than that of

our overall U.S. retail portfolio on a weighted average basis. A shift in demand such that U.S. industry market share for

pickup trucks, larger utility vehicles and minivans deteriorated by 10 percentage points, whether in response to higher

fuel prices or other factors, holding other variables constant, including overall industry sales and our market share of

each vehicle segment, would have reduced the Group’s Adjusted EBIT by approximately 10 percent for 2015. This

estimate does not take into account any other changes in market conditions or actions that the Group may take in

response to shifting consumer preferences, including production and pricing changes.

Our dependence within the NAFTA region on pickup trucks, larger utility vehicles and minivans is expected to increase

further as we intend to shift production in that region away from compact and mid-size passenger cars.

Moreover, we tend to operate with negative working capital as we generally receive payments from vehicle sales

to dealers within a few days of shipment, whereas there is a lag between the time when parts and materials are

received from suppliers and when we pay for such parts and materials; therefore, if vehicle sales decline we will suffer

a significant negative impact on cash flow and liquidity as we continue to pay suppliers during a period in which we

receive reduced proceeds from vehicle sales. If vehicle sales decline, or if they were to fall short of our assumptions,

due to financial crisis, renewed recessionary conditions, changes in consumer confidence, geopolitical events, inability

to produce sufficient quantities of certain vehicles, limited access to financing or other factors, our financial condition

and results of operations would be materially adversely affected.