Chrysler 2013 Annual Report Download - page 135

Download and view the complete annual report

Please find page 135 of the 2013 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

|

|

134 Consolidated

Financial Statements

at 31 December 2013

Notes

The definition of “unusual” adopted by the Group differs from the definition provided in the Consob Communication of 28 July 2006, under

which unusual and/or abnormal transactions are those which – because of their significance or materiality, the nature of the counterparty, the

object of the transaction, the method for determination of the transfer price or the timing of the event (e.g., close to year-end) – could give rise

to doubts regarding the accuracy/completeness of the information in the financial statements, conflicts of interest, the proper safeguarding of

corporate assets or protection of non-controlling interests.

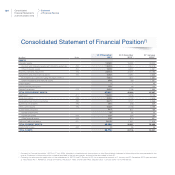

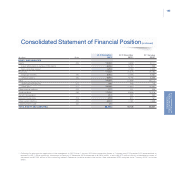

For the Consolidated statement of financial position, a mixed format has been selected to present current and non-current assets and

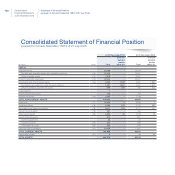

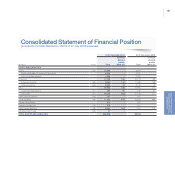

liabilities, as permitted by IAS 1. More specifically, the Group’s financial statements include both industrial companies and financial services

companies. The investment portfolios of financial services companies are included in current assets, as the investments will be realized in

their normal operating cycle. However, the financial services companies only obtain a portion of their funding from the market; the remainder

is obtained from Fiat S.p.A. through the Group’s treasury companies (included under industrial activities), which provide funding both to

industrial companies and financial services companies in the Group, as the need arises. This financial service structure within the Group does

not allow the separation of financial liabilities funding the financial services operations (whose assets are reported within current assets) and

those funding the industrial operations. Presentation of financial liabilities as current or non-current based on their date of maturity would not

facilitate comparison with financial assets, which are categorized on the basis of their normal operating cycle. Disclosure as to the due date of

liabilities is provided in Note 27.

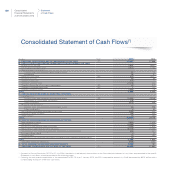

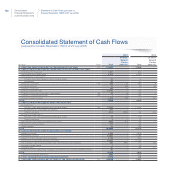

The Statement of cash flows is presented using the indirect method.

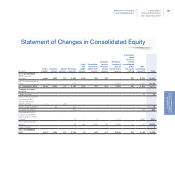

In connection with the requirements of Consob Resolution No. 15519 of 27 July 2006 relating to the format of the financial statements, specific

supplementary Income statement, Statement of financial position and Statement of cash flows formats have been added for related party

transactions.

Significant accounting policies

Basis of consolidation

Subsidiaries

Subsidiaries are entities controlled by the Group, as defined in IAS 27 – Consolidated and Separate Financial Statements. Control exists

when the Group has the power, directly or indirectly, to govern the financial and operating policies of an entity so as to obtain benefits from its

activities. Subsidiaries are consolidated from the date that control commences until the date that control ceases. Equity attributable to non-

controlling interests and non-controlling interests in the profit/(loss) of consolidated subsidiaries are presented separately from the interests

of the owners of the parent in the Consolidated statement of financial position and Income statement respectively. Losses applicable to non-

controlling interests that exceed the minority’s interests in the subsidiary’s equity are allocated against the non-controlling interests.

Changes in the Group’s ownership interests in subsidiaries that do not result in the loss of control are accounted for as equity transactions.

The carrying amounts of the Equity attributable to owners of the parent and Non-controlling interests are adjusted to reflect the changes

in their relative interests in the subsidiaries. Any difference between the book value of the non-controlling interests and the fair value of the

consideration paid or received is recognized directly in the Equity attributable to the owners of the parent.

If the Group loses control of a subsidiary, a gain or loss is recognized in the Income statement and is calculated as the difference between (i)

the aggregate of the fair value of the consideration received and the fair value of any retained interest and (ii) the carrying amount of the assets

(including goodwill) and liabilities of the subsidiary and any non-controlling interests. Any profits or losses recognized in Other comprehensive

income/(losses) in respect of the measurement of the assets of the subsidiary are reclassified to the Income statement when the Group loses

control of the subsidiary if, in accordance with relevant IFRS, these gains and losses would be reclassified to the Income statement on the

disposal of the related assets or liabilities.