Asus 2015 Annual Report Download - page 244

Download and view the complete annual report

Please find page 244 of the 2015 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

|

|

240

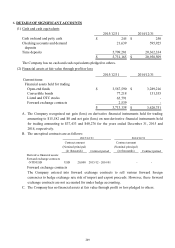

(9) Impairment of financial assets

A. The Company assesses at end of each financial reporting period whether there is objective

evidence that a financial asset or a group of financial assets is impaired as a result of one or

more events that occurred after the initial recognition of the asset (a “loss event”) and that loss

event has an impact on the estimated future cash flows of the financial asset or group of

financial assets that can be reliably estimated.

B. The criteria that the Company uses to determine whether there is objective evidence of an

impairment loss is as follows:

(A) Significant financial difficulty of the issuer or debtor;

(B) A breach of contract, such as a default or delinquency in interest or principal payments;

(C) The Company granted the borrower a concession that a lender would not otherwise

consider for economic or legal reasons relating to the borrower’s financial difficulty;

(D) It becomes probable that the borrower will enter bankruptcy or other financial

reorganization;

(E) The disappearance of an active market for that financial asset because of financial

difficulties;

(F) Observable data indicating that there is a measurable decrease in the estimated future cash

flows from a group of financial assets since the initial recognition of those assets, although

the decrease cannot yet be identified with the individual financial asset in the group,

including adverse changes in the payment status of borrowers in the group or national or

local unfavorable economic conditions that correlate with defaults on the assets in the

group;

(G) Information about significant changes with an adverse effect that have taken place in the

technology, market, economic or legal environment in which the issuer operates, and

indicates that the cost of the investment in the equity instrument may not be recovered; or

(H) A significant or prolonged decline in the fair value of an investment in an equity instrument

below its cost.

C. When the Company assesses that there has been objective evidence of impairment and an

impairment loss has occurred, accounting for impairment is made as follows according to the

category of financial assets:

(A) Financial assets measured at amortised cost

The amount of the impairment loss is measured as the difference between the asset’s

carrying amount and the present value of estimated future cash flows discounted at the

financial asset’s original effective interest rate, and is recognized in profit or loss. If, in a

subsequent period, the amount of the impairment loss decreases and the decrease can be

related objectively to an event occurring after the impairment loss was recognized, the

previously recognized impairment loss is reversed through profit or loss to the extent that

the carrying amount of the asset does not exceed its amortised cost that would have been at

the date of reversal had the impairment loss not been recognized previously. Impairment

loss is recognized and reversed by adjusting the carrying amount of the asset through the

use of an impairment allowance account.