Sallie Mae 2015 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2015 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

|

|

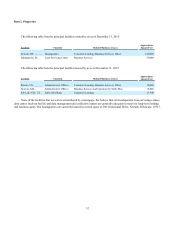

25

2015, the Bank had a Common Equity Tier 1 risk-based capital ratio of 14.4 percent, a Tier 1 risk-based capital ratio of 14.4

percent, a Total risk-based capital ratio of 15.4 percent and a Tier 1 leverage ratio of 12.3 percent.

If the Bank fails to satisfy regulatory risk-based or leverage capital requirements, it may be subject to serious regulatory

sanctions that could prevent us from successfully executing our business plan and may have a material adverse effect on our

business, results of operations, financial position and cash flows. See Item 1. "Business — Supervision and Regulation —

Regulation of Sallie Mae Bank — Regulatory Capital Requirements."

Unfavorable results from required annual stress tests conducted by us may adversely affect our capital position.

The Dodd-Frank Act imposes stress test requirements on banking organizations with total consolidated assets, averaged

over the four most recent consecutive quarters, of more than $10 billion, an asset threshold which the Bank meets. Under the

FDIC’s implementing regulations, the Bank is required to conduct annual stress tests utilizing scenarios provided by the FDIC

and publish a summary of those results. The Bank must conduct its first annual stress test under the rules in the 2016 stress

testing cycle and submit the results of that stress test to the FDIC by July 31, 2016. Published summary results will be required

to include certain measures that evaluate the Bank’s ability to absorb losses in severely adverse economic and financial

conditions. Our regulators may require the Bank to raise additional capital or take other actions, or may impose restrictions on

our business, based on the results of the stress tests. We may not be able to raise additional capital if required to do so, or may

not be able to do so on terms which are advantageous to us or our current shareholders. Any such capital raises, if required, may

also be dilutive to our existing stockholders.

Operations

Failure of our operating systems or infrastructure or inability to adapt to changes could disrupt our business, cause

significant losses, result in regulatory action or damage our reputation.

Our business is dependent on our ability to process and monitor large numbers of transactions in compliance with legal

and regulatory standards and our product specifications. As processing demands change and our loan portfolios grow in both

volume and differing terms and conditions, developing and maintaining our operating systems and infrastructure become

increasingly challenging. There is no assurance we can adequately or efficiently develop, maintain or acquire access to such

systems and infrastructure.

Our loan originations and the servicing, financial, accounting, data processing or other operating systems and facilities

that support them may fail to operate properly, become disabled as a result of events beyond our control or be unable to be

rapidly configured to timely address regulatory changes, in each case potentially adversely affecting our ability to process these

transactions. Any such failure could adversely affect our ability to service our clients, result in financial loss or liability to our

clients, disrupt our business, result in regulatory action or cause reputational damage. Despite the plans and facilities we have in

place, our ability to conduct business may be adversely affected by a disruption in the infrastructure that supports our

businesses. This may include a disruption involving electrical, communications, Internet, transportation or other services used

by us or third-parties with which we conduct business. Notwithstanding our efforts to maintain business continuity, a disruptive

event impacting our processing locations could adversely affect our business, financial condition, results of operations and cash

flows.

Our business processes are becoming increasingly dependent upon technological advancement, and we could lose market

share if we are not able to keep pace with rapid changes in technology.

Our future success depends, in part, on our ability to underwrite and approve loans, and process loan applications and

payments and provide other customer services in a safe, automated manner with high-quality service standards. The volume of

loan originations we are able to process is based, in large part, on the systems and processes we have implemented and

developed. These systems and processes are becoming increasingly dependent upon technological advancement, such as the

ability to process loans and payments over the Internet via personal computers or mobile devices, accept electronic signatures

and provide initial decisions instantly. Our future success also depends, in part, on our ability to develop and implement

technology solutions that anticipate and keep pace with continuing changes in technology, industry standards and client

preferences. We may not be successful in anticipating or responding to these developments on a timely basis. We have made,

and need to continue to make, investments in our technology platform to provide competitive products and services. If