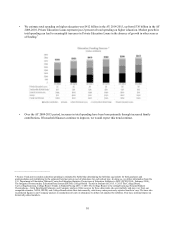

Sallie Mae 2015 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2015 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

|

|

15

Deposit Insurance and Assessments

Deposits at the Bank are insured up to the applicable legal limits by the FDIC - administered Deposit Insurance Fund (the

"DIF"), which is funded primarily by quarterly assessments on insured banks. An insured bank's assessment is calculated by

multiplying its assessment rate by its assessment base. A bank's assessment base and assessment rate are determined each

quarter.

The Bank’s insurance assessment base currently is its average consolidated total assets minus its average tangible equity

during the assessment period. The Bank’s assessment rate is determined by the FDIC using a number of factors, including the

results of supervisory evaluations, the Bank’s capital ratios and its financial condition, as well as the risk posed by the Bank to

the DIF. Assessment rates for insured banks also are subject to adjustment depending on a number of factors, including

significant holdings of brokered deposits in certain instances and the issuance or holding of certain types of debt.

Deposits

With respect to brokered deposits, an insured depository institution must be well-capitalized in order to accept, renew or

roll over such deposits without FDIC clearance. An adequately capitalized insured depository institution must obtain a waiver

from the FDIC to accept, renew or roll over brokered deposits. Undercapitalized insured depository institutions generally may

not accept, renew or roll over brokered deposits. For more information on the Bank’s deposits, see Item 7. “Management's

Discussion and Analysis of Financial Condition and Results of Operations — Key Financial Measures — Funding Sources”.

Regulatory Examinations

The Bank currently undergoes regular on-site examinations by the Bank’s regulators, which examine for adherence to a

range of legal and regulatory compliance responsibilities. A regulator conducting an examination has complete access to the

books and records of the examined institution. The results of the examination are confidential. The cost of examinations may be

assessed against the examined institution as the agency deems necessary or appropriate.

Source of Strength

Under the Dodd-Frank Act, we are required to serve as a source of financial strength to the Bank and to commit resources

to support the Bank in circumstances when we might not do so absent the statutory requirement. Any loan by us to the Bank

would be subordinate in right of payment to depositors and to certain other indebtedness of the Bank.

Community Reinvestment Act

The Community Reinvestment Act requires the FDIC to evaluate the record of the Bank in meeting the credit needs of its

local community, including low- and moderate-income neighborhoods. These evaluations are considered in evaluating mergers,

acquisitions and applications to open a branch or facility. Failure to adequately meet these criteria could result in additional

requirements and limitations on the Bank.

Privacy Laws

The federal banking regulators, as required by the Gramm-Leach-Bliley Act, have adopted regulations that limit the

ability of banks and other financial institutions to disclose nonpublic information about consumers to nonaffiliated third-parties.

Financial institutions are required to disclose to consumers their policies for collecting and protecting confidential customer

information. Customers generally may prevent financial institutions from sharing nonpublic personal financial information with

nonaffiliated third-parties, with some exceptions, such as the processing of transactions requested by the consumer. Financial

institutions generally may not disclose certain consumer or account information to any nonaffiliated third-party for use in

telemarketing, direct mail marketing or other marketing. The privacy regulations also restrict information sharing among

affiliates for marketing purposes and govern the use and provision of information to consumer reporting agencies. Federal and

state banking agencies have prescribed standards for maintaining the security and confidentiality of consumer information, and

the Bank is subject to such standards, as well as certain federal and state laws or standards for notifying consumers in the event

of a security breach.