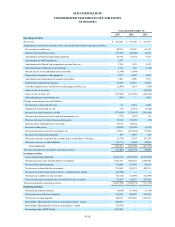

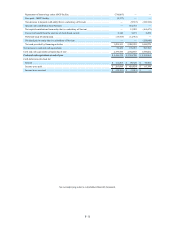

Sallie Mae 2015 Annual Report Download - page 110

Download and view the complete annual report

Please find page 110 of the 2015 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

|

|

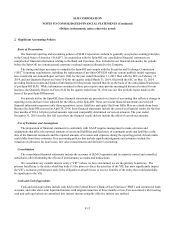

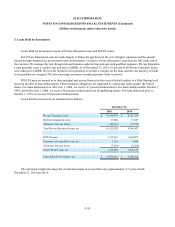

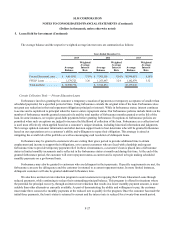

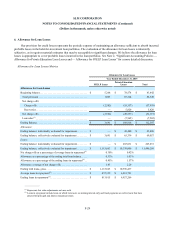

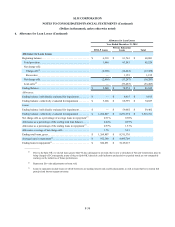

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, unless otherwise noted)

2. Significant Accounting Policies (Continued)

F-20

(including Navient) resulting in a net gain on sale of loans of $135 million and $85 million for the years ended December 31,

2015 and 2014, respectively. See Note 16, “Arrangements with Navient Corporation,” for further discussion regarding loan

purchase agreements.

Other Income

Our Upromise subsidiary has a number of programs that encourage consumers to save for the cost of college education.

We have established a consumer savings network, which is designed to promote college savings by consumers who are

members of this program by encouraging them to purchase goods and services from the merchants that participate in the

program. Participating merchants generally pay Upromise fees based on member purchase volume, either online or in stores

depending on the contractual arrangement with the merchant. We recognize revenue as marketing and administrative services

are rendered, based upon contractually determined rates and member purchase volumes.

Securitization Accounting

Our securitizations transactions use a two-step structure with a special purpose entity (variable interest entity (“VIE”))

that legally isolates the transferred assets from us in the event of bankruptcy or receivership. Transactions receiving sale

treatment are also structured to ensure that the holders of the beneficial interests issued are not constrained from pledging or

exchanging their interests, and that we do not maintain effective control over the transferred assets. If these criteria are not met,

then the transaction is accounted for as an on-balance sheet secured borrowing. If a securitization qualifies as a sale, we then

assess whether we are the primary beneficiary of the securitization trust and are required to consolidate such trust. We are

considered the primary beneficiary if we have both: (1) the power to direct the activities of the VIE that most significantly

impact the VIE’s economic performance and (2) the obligation to absorb losses or receive benefits of the entity that could

potentially be significant to the VIE. There can be considerable judgment as it relates to determining the primary beneficiary of

the VIEs. There are no “bright line” tests. Rather, the assessment of who has the power to direct the activities of the VIE that

most significantly affect the VIE’s economic performance and who has the obligation to absorb losses or receive benefits of the

entity that could potentially be significant to the VIE can be very qualitative and judgmental in nature. If we are the primary

beneficiary then no gain or loss is recognized.

We have determined that as the sponsor and servicer of Sallie Mae securitization trusts, we meet the first primary

beneficiary criterion because we have the power to direct the activities of the VIE that most significantly impact the VIE’s

economic performance.

Irrespective of whether a securitization receives sale or on-balance sheet treatment, our continuing involvement with our

securitization trusts is generally limited to:

• Owning the equity certificates of certain trusts.

• The servicing of the student loan assets within the securitization trusts, on both a pre- and post-default basis.

• Our acting as administrator for the securitization transactions we sponsored.

• Our responsibilities relative to representation and warranty violations.

• The option to exercise the clean-up call and purchase the student loans from the trust when the pool balance is 10

percent or less of the original pool balance.

In 2015 and 2014, we executed both secured financing and securitized loan sale transactions. Based upon our

relationships with these securitizations, we believe the consolidation assessment is straightforward. We consolidated our

secured financing transactions because either we did not meet the accounting criterion for sales treatment or we determined we

were the primary beneficiary of the VIE because we retained (a) the residual interest in the securitization and therefore had the

obligation to absorb losses or receive benefits of the entity that could potentially be significant to the VIE as well as (b) the

power to direct the activities of the VIE in our role as servicer. For those accounted for as securitized loan sales, we were not