Sallie Mae 2015 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2015 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

|

|

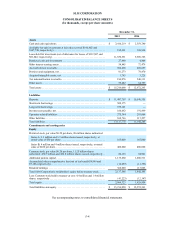

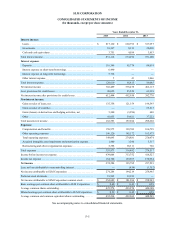

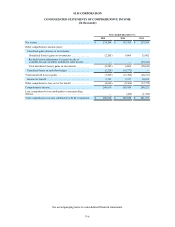

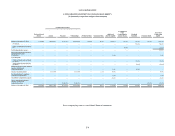

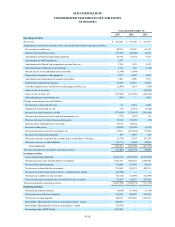

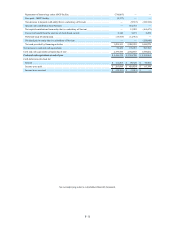

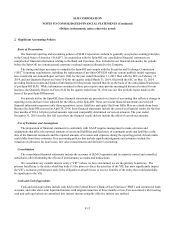

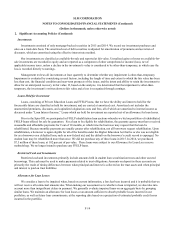

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, unless otherwise noted)

2. Significant Accounting Policies (Continued)

F-14

Investments

Investments consisted of only mortgage-backed securities in 2015 and 2014. We record our investment purchases and

sales on a trade date basis. The amortized cost of debt securities is adjusted for amortization of premiums and accretion of

discounts, which are amortized using the effective interest rate method.

Our investments are classified as available-for-sale and reported at fair value. Unrealized gains or losses on available-for-

sale investments are recorded in equity and are reported as a component of other comprehensive income/(loss), net of

applicable income taxes, unless a decline in the investment’s value is considered to be other-than-temporary, in which case the

loss is recorded directly to earnings.

Management reviews all investments at least quarterly to determine whether any impairment is other-than-temporary.

Impairment is evaluated by considering several factors, including the length of time and extent to which the fair value has been

less than cost, the financial condition and near-term prospects of the issuer, and the intent and ability to retain the investment to

allow for an anticipated recovery in fair value. If, based on the analysis, it is determined that the impairment is other-than-

temporary, the investment is written down to fair value and a loss is recognized through earnings.

Loans Held for Investment

Loans, consisting of Private Education Loans and FFELP loans, that we have the ability and intent to hold for the

foreseeable future are classified as held for investment, and are carried at amortized cost. Amortized cost includes the

unamortized premiums, discounts, and capitalized origination costs and fees, all of which are amortized to interest income as

discussed under “Loan Interest Income.” Loans which are held for investment are reported net of an allowance for loan losses.

Prior to the Spin-Off, we participated in FFELP rehabilitation loan auctions whereby we bid on portfolios of rehabilitated

FFELP loans offered for sale by guarantors. For a loan to be eligible for rehabilitation, the guaranty agency must have received

reasonable and affordable payments for 9 out of 10 months, at which time the borrower may request that the loan be

rehabilitated. Because monthly payments are usually greater after rehabilitation, not all borrowers request rehabilitation. Upon

rehabilitation, a borrower is again eligible for all of the benefits under the Higher Education Act that he or she was not eligible

for as a borrower on a defaulted loan, such as new federal aid, and the default on the borrower’s credit record is expunged. No

student loan may be rehabilitated more than once. We did not purchase any of these loans in 2015. In 2014, we purchased

$7.5 million of these loans, at 102 percent of par value. These loans were subject to our Allowance for Loan Loss reserve

methodology. We no longer intend to purchase any FFELP loans.

Restricted Cash and Investments

Restricted cash and investments primarily include amounts held in student loan securitization trusts and other secured

borrowings. This cash must be used to make payments related to trust obligations. Amounts on deposit in these accounts are

primarily the result of timing differences between when principal and interest is collected on the trust assets and when principal

and interest is paid on trust liabilities.

Allowance for Loan Losses

We consider a loan to be impaired when, based on current information, a loss has been incurred and it is probable that we

will not receive all contractual amounts due. When making our assessment as to whether a loan is impaired, we also take into

account more than insignificant delays in payment. We generally evaluate impaired loans on an aggregate basis by grouping

similar loans. We maintain an allowance for loan losses at an amount sufficient to absorb probable losses incurred in our

portfolios, as well as future loan commitments, at the reporting date based on a projection of estimated probable credit losses

incurred in the portfolio.