Sallie Mae 2015 Annual Report Download - page 152

Download and view the complete annual report

Please find page 152 of the 2015 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

|

|

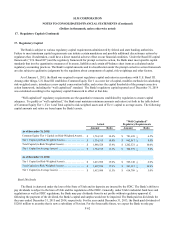

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, unless otherwise noted)

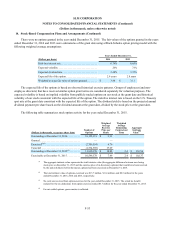

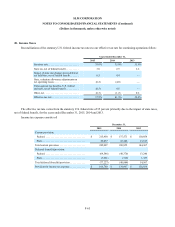

17. Regulatory Capital (Continued)

F-62

17. Regulatory Capital

The Bank is subject to various regulatory capital requirements administered by federal and state banking authorities.

Failure to meet minimum capital requirements can initiate certain mandatory and possibly additional discretionary actions by

regulators that, if undertaken, could have a direct material adverse effect on our financial condition. Under the Basel III capital

framework (“U.S. Basel III”) and the regulatory framework for prompt corrective action, the Bank must meet specific capital

standards that involve quantitative measures of its assets, liabilities and certain off-balance sheet items as calculated under

regulatory accounting practices. The Bank’s capital amounts and its classification under the prompt corrective action framework

are also subject to qualitative judgments by the regulators about components of capital, risk weightings and other factors.

As of January 1, 2015, the Bank was required to report regulatory capital and ratios in accordance with U.S. Basel III.

Among other things, U.S. Basel III establishes Common Equity Tier 1 as a new tier of capital, modifies methods for calculating

risk-weighted assets, introduces a new capital conservation buffer, and revises the capital thresholds of the prompt corrective

action framework, including the “well capitalized” standard. The Bank’s regulatory capital reported as of December 31, 2014

was calculated according to the regulatory capital framework in effect at that date.

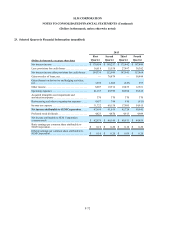

“Well capitalized” regulatory requirements are the quantitative measures established by regulation to ensure capital

adequacy. To qualify as “well capitalized,” the Bank must maintain minimum amounts and ratios (set forth in the table below)

of Common Equity Tier 1, Tier 1 and Total capital to risk-weighted assets and of Tier 1 capital to average assets. The following

capital amounts and ratios are based upon the Bank's assets.

Actual "Well Capitalized"

Regulatory Requirements

Amount Ratio Amount Ratio

As of December 31, 2015:

Common Equity Tier 1 Capital (to Risk-Weighted Assets). . $ 1,734,315 14.4% $ 781,638 > 6.5%

Tier 1 Capital (to Risk-Weighted Assets). . . . . . . . . . . . . . . . $ 1,734,315 14.4% $ 962,017 > 8.0%

Total Capital (to Risk-Weighted Assets). . . . . . . . . . . . . . . . $ 1,848,528 15.4% $ 1,202,521 > 10.0%

Tier 1 Capital (to Average Assets). . . . . . . . . . . . . . . . . . . . . $ 1,734,315 12.3% $ 704,979 > 5.0%

As of December 31, 2014:

Tier 1 Capital (to Risk-Weighted Assets). . . . . . . . . . . . . . . . $ 1,413,988 15.0% $ 565,148 > 6.0%

Total Capital (to Risk-Weighted Assets). . . . . . . . . . . . . . . . $ 1,497,830 15.9% $ 941,913 > 10.0%

Tier 1 Capital (to Average Assets). . . . . . . . . . . . . . . . . . . . . $ 1,413,988 11.5% $ 614,709 > 5.0%

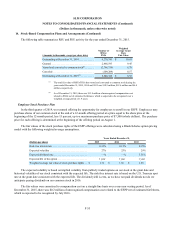

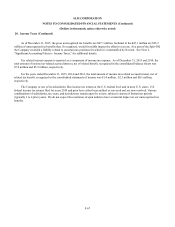

Bank Dividends

The Bank is chartered under the laws of the State of Utah and its deposits are insured by the FDIC. The Bank’s ability to

pay dividends is subject to the laws of Utah and the regulations of the FDIC. Generally, under Utah’s industrial bank laws and

regulations as well as FDIC regulations, the Bank may pay dividends from its net profits without regulatory approval if,

following the payment of the dividend, the Bank’s capital and surplus would not be impaired. The Bank paid no dividends for

the years ended December 31, 2015 and 2014, respectively. For the year ended December 31, 2013, the Bank paid dividends of

$120.0 million to an entity that is now a subsidiary of Navient. For the foreseeable future, we expect the Bank to only pay