PNC Bank 2010 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

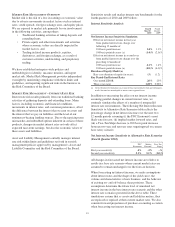

Noninterest Expense

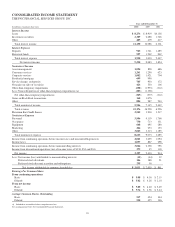

Noninterest expense for 2009 was $9.1 billion compared with

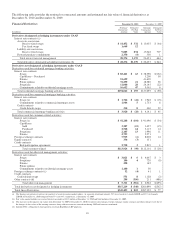

$3.7 billion in 2008. The increase was substantially related to

National City. We also recorded a special FDIC assessment of

$133 million in the second quarter of 2009, which was

intended to build the FDIC’s Deposit Insurance Fund.

Integration costs included in noninterest expense totaled

$421 million in 2009 compared with $122 million in 2008.

Our quarterly run rate of acquisition cost savings related to

National City increased to $300 million in the fourth quarter

of 2009, or $1.2 billion per year. Acquisition cost savings

totaled $800 million in 2009.

Effective Tax Rate

Our effective tax rate was 26.9% for 2009 and 27.2% for

2008.

C

ONSOLIDATED

B

ALANCE

S

HEET

R

EVIEW

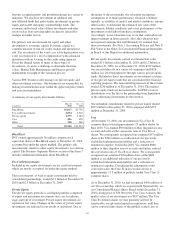

Loans

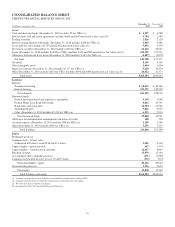

Loans decreased $17.9 billion, or 10%, as of December 31,

2009 compared with December 31, 2008. Loans represented

58% of total assets at December 31, 2009 and 60% of total

assets at December 31, 2008. The decline in loans during 2009

was driven primarily by lower utilization levels for

commercial lending among middle market and large corporate

clients, although this trend in utilization rates appeared to have

eased in the fourth quarter of 2009.

Commercial lending represented 53% of the loan portfolio and

consumer lending represented 47% at December 31, 2009.

Commercial lending declined 17% at December 31, 2009

compared with December 31, 2008. Commercial loans, which

comprised 65% of total commercial lending, declined 21%

due to reduced demand for new loans, lower utilization levels

and paydowns as clients continued to deleverage their balance

sheets. Total consumer lending decreased slightly at

December 31, 2009 from December 31, 2008.

Investment Securities

Total investment securities at December 31, 2009 were

$56.0 billion compared with $43.5 billion at December 31,

2008. Securities represented 21% of total assets at

December 31, 2009 compared with 15% of total assets at

December 31, 2008. The increase in securities of $12.6 billion

since December 31, 2008 primarily reflected the purchase of

US Treasury and government agency securities as well as

price appreciation in the available for sale portfolio, partially

offset by maturities, prepayments and sales.

At December 31, 2009, the securities available for sale

portfolio included a net unrealized loss of $2.3 billion, which

represented the difference between fair value and amortized

cost. The comparable amount at December 31, 2008 was a net

unrealized loss of $5.4 billion. The expected weighted-average

life of investment securities (excluding corporate stocks and

other) was 4.1 years at December 31, 2009 and 3.1 years at

December 31, 2008.

Loans Held For Sale

Loans held for sale totaled $2.5 billion at December 31, 2009

compared with $4.4 billion at December 31, 2008. We stopped

originating commercial mortgage loans held for sale

designated at fair value during the first quarter of 2008 and

intend to continue pursuing opportunities to reduce these

positions at appropriate prices. For commercial mortgages

held for sale carried at the lower of cost or market, strong

origination volumes partially offset sales to government

agencies during 2009. Residential mortgage loans held for sale

decreased during 2009 despite strong refinancing volumes,

especially in the first quarter.

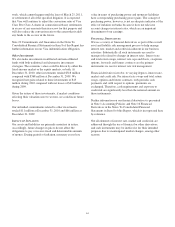

Asset Quality

Nonperforming assets increased $4.1 billion to $6.3 billion at

December 31, 2009 compared with $2.2 billion at

December 31, 2008. The increase resulted from recessionary

conditions in the economy and reflected a $2.6 billion increase

in commercial lending nonperforming loans and a $1.4 billion

increase in consumer lending nonperforming loans. The

increase in nonperforming commercial lending was primarily

from real estate, including residential real estate development

and commercial real estate exposure; manufacturing; and

service providers. The increase in nonperforming consumer

lending was mainly due to residential mortgage loans. While

nonperforming assets increased across all applicable business

segments during 2009, the largest increases were $2.0 billion

in Corporate & Institutional Banking and $854 million in

Distressed Assets Portfolio.

At December 31, 2009, our largest nonperforming asset was

approximately $49 million and our average nonperforming

loan associated with commercial lending was approximately

$1 million.

Goodwill and Other Intangible Assets

Goodwill increased $637 million and other intangible assets

increased $584 million at December 31, 2009 compared with

December 31, 2008. During 2009, adjustments were made to

the estimated fair values of assets acquired and liabilities

assumed as part of the National City acquisition. This resulted

in the recognition of $451 million of core deposit and other

relationship intangibles at December 31, 2009. In addition, the

purchase price allocation for the National City acquisition was

completed as of December 31, 2009 with goodwill of

$647 million recognized.

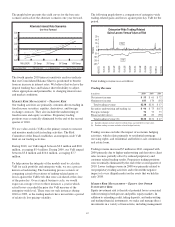

Funding Sources

Total funding sources were $226.2 billion at December 31,

2009 and $245.1 billion at December 31, 2008. Funding

sources decreased $18.9 billion, driven by declines in other

time deposits, retail certificates of deposit and Federal Home

Loan Bank borrowings, partially offset by increases in money

market and demand deposits.

87