PNC Bank 2010 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

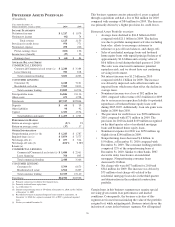

The decrease in the residential mortgages indemnification and

repurchase liability in 2010 and 2009 was reflective of lower

actual repurchase and indemnification losses driven primarily

by higher claim rescission rates. This decrease resulted despite

higher levels of investor indemnification and repurchase claim

activity as described above. The 2009 decrease in the home

equity loans/lines indemnification and repurchase liability

resulted primarily from the reduction in loss exposure

associated with pooled settlement activity. Conversely, the

2010 increase in this liability was attributable to

management’s estimate that higher anticipated losses will

result from higher forecasted volumes of asserted and

unasserted indemnification and repurchase claims.

We believe our indemnification and repurchase liabilities

adequately reflect the estimated losses on anticipated investor

indemnification and repurchase claims at December 31, 2010

and 2009. However, actual losses could be more or less than

our established indemnification and repurchase liability.

Factors that could affect our estimate include the timing and

frequency of investor claims driven by investor strategies and

behavior, our ability to successfully negotiate claims with

investors, the housing markets which drive the estimates made

for loan indemnification and repurchase losses, and other

economic conditions. Accordingly, if we assumed an adverse

change of 10% for the indemnification and repurchase claims,

claim rescission rates, and indemnification and repurchase

loss assumptions in our indemnification and repurchase

liability model, this liability would increase to $334 million at

December 31, 2010.

R

ISK

M

ANAGEMENT

We encounter risk as part of the normal course of our business

and we design risk management processes to help manage

these risks. This Risk Management section describes our risk

management philosophy, principles, governance and various

aspects of our corporate-level risk management program. We

also provide an analysis of our primary areas of risk: credit,

operational, liquidity, and market. The discussion of market

risk is further subdivided into interest rate, trading, and equity

and other investment risk areas. Our use of financial

derivatives as part of our overall asset and liability risk

management process is also addressed within the Risk

Management section of this Item 7. In appropriate places

within this section, historical performance is also addressed.

Risk Management Philosophy

PNC’s risk management philosophy is to manage to an overall

moderate level of risk to capture opportunities and optimize

shareholder value. We dynamically set our strategies and

make distinct risk taking decisions with consideration for the

impact to our aggregate risk profile. While, due to the

National City acquisition and the overall state of the economy,

our enterprise risk profile does not currently meet our desired

moderate risk level, we have made substantial progress in

returning to that level in 2009 and 2010.

Risk Management Principles

• Designed to only take risks consistent with our

strategy and within our capability to manage,

• Limit risk-taking by a set of boundaries,

• Practice disciplined capital and liquidity

management,

• Help ensure that risks and earnings volatility are

appropriately understood, measured and rewarded,

• Avoid excessive concentrations, and

• Help support external stakeholder confidence in

PNC.

We support risk management through a governance structure

involving the Board, senior management and a corporate risk

management organization.

Although our Board as a whole is responsible generally for

oversight of risk management, committees of the Board

provide oversight to specific areas of risk with respect to the

level of risk and risk management structure.

We use management level risk committees to help ensure that

business decisions are executed within our desired risk profile.

The Executive Committee (EC), consisting of senior

management executives, provides oversight for the

establishment and implementation of new comprehensive risk

management initiatives, reviews enterprise level risk profiles

and discusses key risk issues.

Corporate-Level Risk Management Program

The corporate risk management organization has the following

key roles:

• Facilitate the identification, assessment and

monitoring of risk across PNC,

• Provide support and oversight to the businesses,

• Help identify and implement risk management best

practices, as appropriate, and

• Work with the lines of business to shape and define

PNC’s business risk limits.

Risk Measurement

We conduct risk measurement activities specific to each area

of risk. The primary vehicle for aggregation of enterprise-wide

risk is a comprehensive risk management methodology that is

based on economic capital. This primary risk aggregation

measure is supplemented with secondary measures of risk to

arrive at an estimate of enterprise-wide risk. The economic

capital framework is a measure of potential losses above and

beyond expected losses. Potential one year losses are

capitalized to a level commensurate with a financial institution

with an A rating by the credit rating agencies. Economic

capital incorporates risk associated with potential credit losses

(Credit Risk), fluctuations of the estimated market value of

financial instruments (Market Risk), failure of people,

processes or systems (Operational Risk), and losses associated

with declining volumes, margins and/or fees, and the fixed

cost structure of the business. We estimate credit and market

68