PNC Bank 2010 Annual Report Download - page 133

Download and view the complete annual report

Please find page 133 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

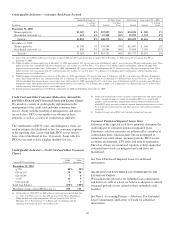

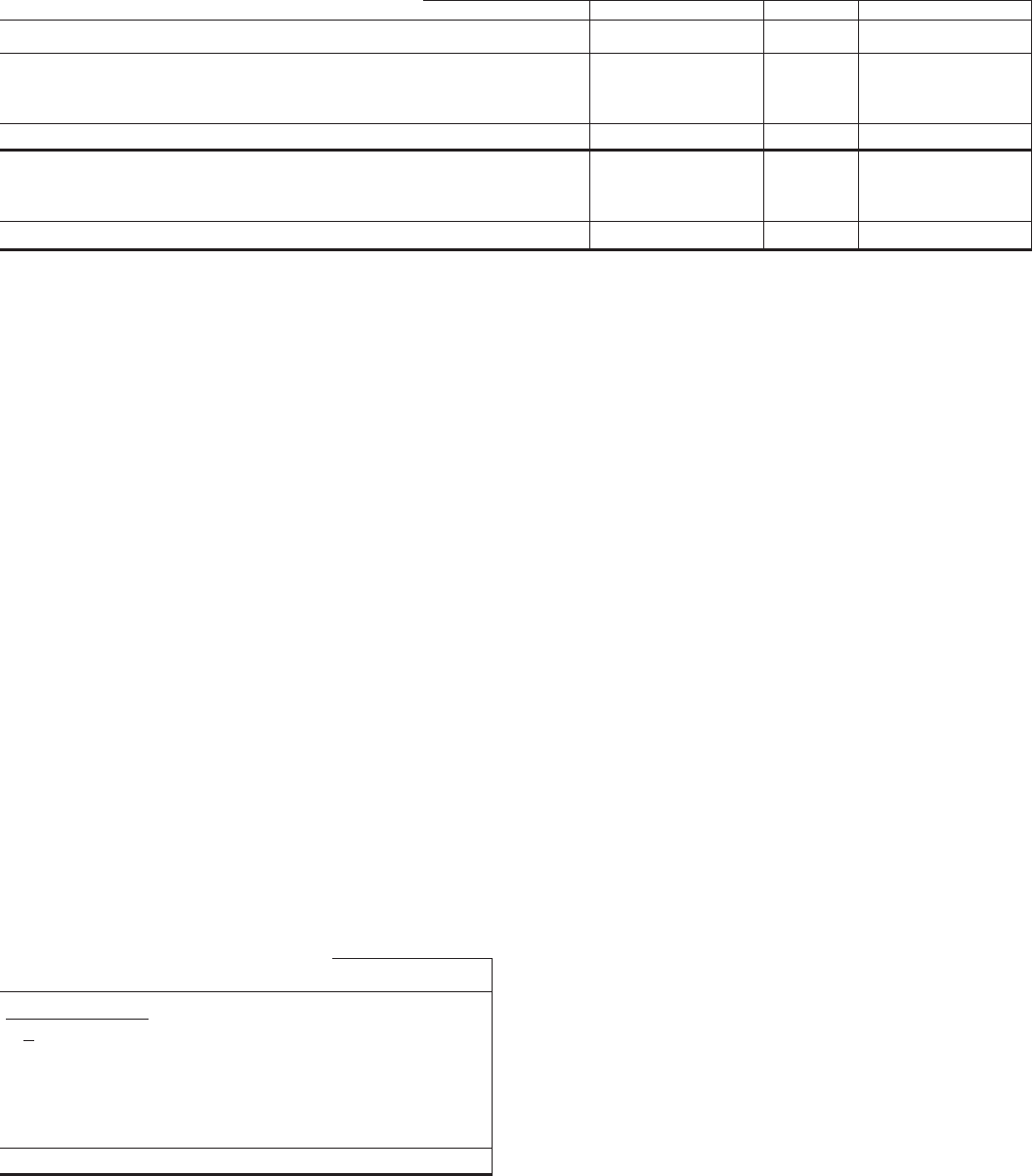

Credit Quality Indicators – Consumer Real Estate Secured

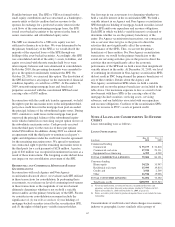

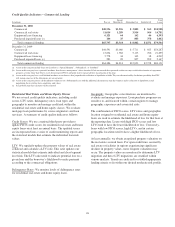

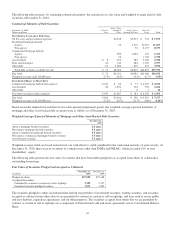

Higher Risk Loans (a) All Other Loans Total Loans Loans with LTV > 100%

In millions Amount

% of Total

Loans Amount

% of Total

Loans Amount Amount

% of Total

Loans

December 31, 2010

Home equity (b) $1,203 4% $33,023 96% $34,226 $ 285 1%

Residential real estate (c) 651 4% 15,348 96% 15,999 1,331 8%

Total (d) $1,854 4% $48,371 96% $50,225 $1,616 3%

December 31, 2009

Home equity (b) $1,198 3% $34,749 97% $35,947 $ 306 1%

Residential real estate (c) 826 4% 18,984 96% 19,810 2,385 12%

Total (d) $2,024 4% $53,733 96% $55,757 $2,691 5%

(a) Loans with a recent FICO credit score of less than or equal to 660 and a LTV ratio greater than or equal to 90% at December 31, 2010, and a LTV ratio greater than 90% at

December 31, 2009.

(b) Within the higher risk home equity class at December 31, 2010, approximately 10% were in some stage of delinquency and 6% were in late stage (90+ days) delinquency status. These

higher risk loans were concentrated with 28% in Pennsylvania, 13% in Ohio, 11% in New Jersey, 7% in Illinois, 6% in Michigan and 5% in Kentucky, with the remaining loans

dispersed across several other states. At December 31, 2009, approximately 10% were in some stage of delinquency and 5% were in late stage (90+ days) delinquency status. These

higher risk loans were concentrated with 28% in Pennsylvania, 14% in Ohio, 11% in New Jersey, 7% in Illinois, 6% in Michigan and 5% in Kentucky, with the remaining loans

dispersed across several other states.

(c) Within the higher risk residential real estate class at December 31, 2010, approximately 48% were in some stage of delinquency and 36% were in late stage (90+ days) delinquency

status. These higher risk loans were concentrated with 24% in California, 11% in Florida, 11% in Illinois, 8% in Maryland, 4% in Pennsylvania, 4% in New Jersey, and 4% in Ohio,

with the remaining loans dispersed across several other states. At December 31, 2009, approximately 61% were in some stage of delinquency and 49% were in late stage (90+ days)

delinquency status. These higher risk loans were concentrated with 22% in California, 13% in Florida, 10% in Illinois, 8% in Maryland, 5% in Pennsylvania, and 5% in New Jersey,

with the remaining loans dispersed across several other states.

(d) Includes purchased impaired loans of $5.9 billion at December 31, 2010 and $8.0 billion at December 31, 2009.

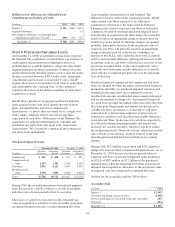

Credit Card and Other Consumer (Education, Automobile,

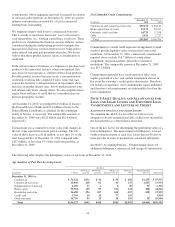

and Other Secured and Unsecured Lines and Loans) Classes

We monitor a variety of credit quality information in the

management of the credit card and other consumer loan

classes. Along with the trending of delinquencies and losses

for each class, FICO score updates are obtained at least

annually, as well as a variety of credit bureau attributes.

The combination of FICO scores and delinquency status are

used to estimate the likelihood of loss for consumer exposure

at the reporting date. Loans with high FICO scores tend to

have a lower likelihood of loss. Conversely, loans with low

FICO scores tend to have a higher likelihood of loss.

Credit Quality Indicators – Credit Card and Other Consumer

Classes

Current FICO Score Range

Credit

Card (a)

Other

Consumer

December 31, 2010

> 720 48% 58%

650 to 719 29 28

620 to 649 54

< 620 11 9

Unscored (b) 71

Total loan balance 100% 100%

Weighted average current FICO score (c) 709 713

(a) At December 31, 2010, PNC has $70 million of credit card loans that are high risk

(i.e., loans with FICO scores less than 660 and greater than 90 day delinquency).

Within the high risk credit card portfolio, 20% are located in Ohio, 14% in

Michigan, 14% in Pennsylvania, 8% in Illinois and 7% in Indiana, with the

remaining loans dispersed across several other states.

(b) Credit card unscored refers to new accounts issued to borrowers with limited credit

history, accounts for which we cannot get an updated FICO (e.g., recent profile

changes), cards issued with a business name, and/ or collateral secured cards for

which FICO scores were not available or required. Management proactively assesses

the risk and size of unscored loans and, when necessary, takes actions to mitigate

credit risk.

(c) Weighted average current FICO score excludes accounts with no score.

Consumer Purchased Impaired Loans Class

Estimates of the expected cash flows primarily determine the

credit impacts of consumer purchased impaired loans.

Consumer cash flow estimates are influenced by a number of

credit related items which include, but are not limited to,

estimated real estate values, payment patterns, FICO scores,

economic environment, LTV ratios and time of origination.

These key drivers are monitored regularly to help ensure that

concentrations of risk are mitigated and cash flows are

maximized.

See Note 6 Purchased Impaired Loans for additional

information.

A

LLOWANCE FOR

U

NFUNDED

L

OAN

C

OMMITMENTS AND

L

ETTERS OF

C

REDIT

We maintain the allowance for unfunded loan commitments

and letters of credit at a level we believe is adequate to absorb

estimated probable losses related to these unfunded credit

facilities.

See Note 1 Accounting Policies – Allowance For Unfunded

Loan Commitments and Letters of Credit for additional

information.

125