PNC Bank 2010 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

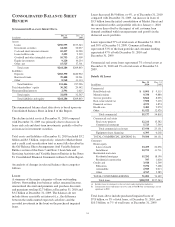

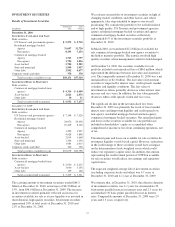

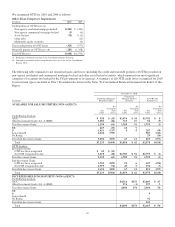

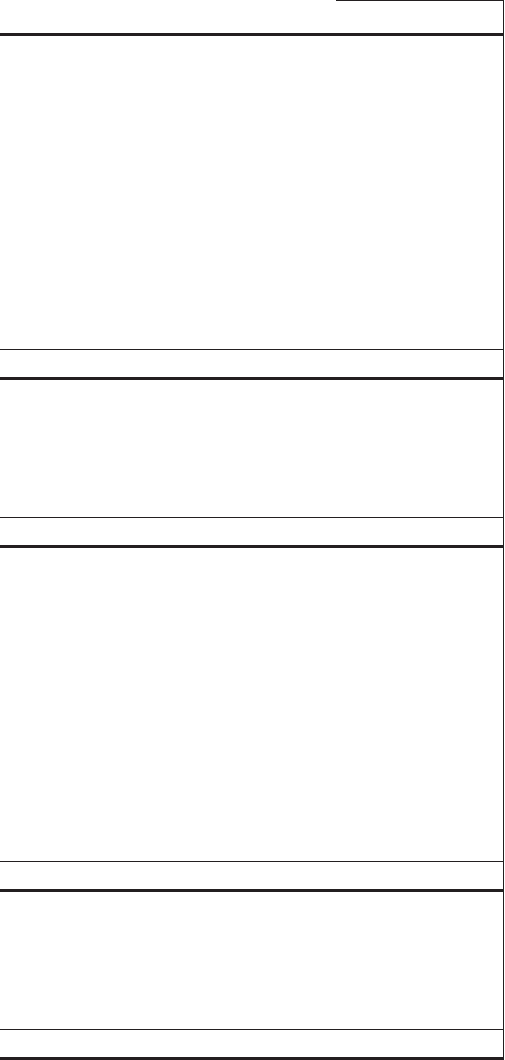

INVESTMENT SECURITIES

Details of Investment Securities

In millions

Amortized

Cost

Fair

Value

December 31, 2010

S

ECURITIES

A

VAILABLE FOR

S

ALE

Debt securities

US Treasury and government agencies $ 5,575 $ 5,710

Residential mortgage-backed

Agency 31,697 31,720

Non-agency 8,193 7,233

Commercial mortgage-backed

Agency 1,763 1,797

Non-agency 1,794 1,856

Asset-backed 2,780 2,582

State and municipal 1,999 1,957

Other debt 3,992 4,077

Corporate stocks and other 378 378

Total securities available for sale $58,171 $57,310

S

ECURITIES

H

ELD TO

M

ATURITY

Debt securities

Commercial mortgage-backed (non-

agency) $ 4,316 $ 4,490

Asset-backed 2,626 2,676

Other debt 10 11

Total securities held to maturity $ 6,952 $ 7,177

December 31, 2009

S

ECURITIES

A

VAILABLE FOR

S

ALE

Debt securities

US Treasury and government agencies $ 7,548 $ 7,520

Residential mortgage-backed

Agency 24,076 24,438

Non-agency 10,419 8,302

Commercial mortgage-backed

Agency 1,299 1,297

Non-agency 4,028 3,848

Asset-backed 2,019 1,668

State and municipal 1,346 1,350

Other debt 1,984 2,015

Corporate stocks and other 360 360

Total securities available for sale $53,079 $50,798

S

ECURITIES

H

ELD TO

M

ATURITY

Debt securities

Commercial mortgage-backed (non-

agency) $ 2,030 $ 2,225

Asset-backed 3,040 3,136

Other debt 159 160

Total securities held to maturity $ 5,229 $ 5,521

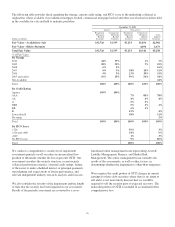

The carrying amount of investment securities totaled $64.3

billion at December 31, 2010, an increase of $8.3 billion, or

15%, from $56.0 billion at December 31, 2009. The increase

in investment securities primarily reflected an increase in

securities available for sale as excess liquidity was invested in

short duration, high quality securities. Investment securities

represented 24% of total assets at December 31, 2010 and

21% at December 31, 2009.

We evaluate our portfolio of investment securities in light of

changing market conditions and other factors and, where

appropriate, take steps intended to improve our overall

positioning. We consider the portfolio to be well-diversified

and of high quality. US Treasury and government agencies,

agency residential mortgage-backed securities and agency

commercial mortgage-backed securities collectively

represented 61% of the investment securities portfolio at

December 31, 2010.

In March 2010, we transferred $2.2 billion of available for

sale commercial mortgage-backed non-agency securities to

the held to maturity portfolio. The transfer involved high

quality securities where management’s intent to hold changed.

At December 31, 2010, the securities available for sale

portfolio included a net unrealized loss of $861 million, which

represented the difference between fair value and amortized

cost. The comparable amount at December 31, 2009 was a net

unrealized loss of $2.3 billion. The fair value of investment

securities is impacted by interest rates, credit spreads, market

volatility and liquidity conditions. The fair value of

investment securities generally decreases when interest rates

increase and vice versa. In addition, the fair value generally

decreases when credit spreads widen and vice versa.

The significant decline in the net unrealized loss from

December 31, 2009 was primarily the result of lower market

interest rates and improving liquidity and credit spreads on

non-agency residential mortgage-backed and non-agency

commercial mortgage-backed securities. Net unrealized gains

and losses in the securities available for sale portfolio are

included in shareholders’ equity as accumulated other

comprehensive income or loss from continuing operations, net

of tax.

Unrealized gains and losses on available for sale securities do

not impact liquidity or risk-based capital. However, reductions

in the credit ratings of these securities would have an impact

on the determination of risk-weighted assets which could

reduce our regulatory capital ratios. In addition, the amount

representing the credit-related portion of OTTI on available

for sale securities would reduce our earnings and regulatory

capital ratios.

The expected weighted-average life of investment securities

(excluding corporate stocks and other) was 4.7 years at

December 31, 2010 and 4.1 years at December 31, 2009.

We estimate that, at December 31, 2010, the effective duration

of investment securities was 3.1 years for an immediate 50

basis points parallel increase in interest rates and 2.9 years for

an immediate 50 basis points parallel decrease in interest

rates. Comparable amounts at December 31, 2009 were 2.9

years and 2.5 years, respectively.

37