PNC Bank 2010 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

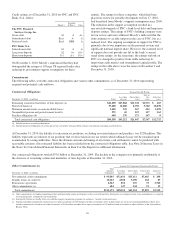

|

|

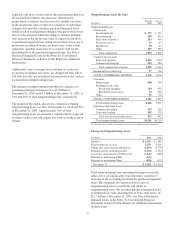

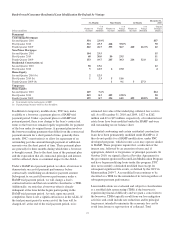

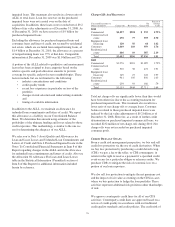

Bank-Owned Consumer Residential Loan Modification Re-Default by Vintage

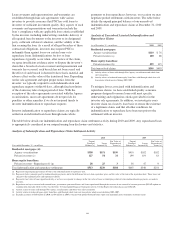

Six Months Nine Months 12 Months

December 31,

2010

Dollars in millions

Number of

Accounts

%of

Vintage

Modified

Number of

Accounts

%of

Vintage

Modified

Number of

Accounts

%of

Vintage

Modified

Unpaid

Principal

Balance

Permanent

Conforming Mortgages

Second Quarter 2010 354 23.9% $57

First Quarter 2010 312 23.3 468 35.0% 70

Fourth Quarter 2009 242 26.7 333 36.7 420 46.3% 62

Non-Prime Mortgages

Second Quarter 2010 104 23.5 15

First Quarter 2010 68 20.0 80 23.5 11

Fourth Quarter 2009 133 19.7 205 30.3 216 32.0 22

Residential Construction (a)

Second Quarter 2010 38 13.6 12

First Quarter 2010 5 12.5 6 15.0 4

Home Equity

Second Quarter 2010 (b) 2 12.5

First Quarter 2010 (b) 1 2.3 5 11.6

Fourth Quarter 2009 (b) 1 9.1 3 27.3

Temporary

Home Equity

Second Quarter 2010 169 7.6% $14

First Quarter 2010 243 8.3 402 13.8% 30

Fourth Quarter 2009 199 8.7 334 14.5 432 18.8% 30

(a) No re-defaults for the fourth quarter of 2009.

(b) Unpaid principal balance totals less than $1 million.

In addition to temporary modifications, PNC may make

available to a borrower a payment plan or a HAMP trial

payment period. Under a payment plan or a HAMP trial

payment period, there is no change to the loan’s contractual

terms so the borrower remains legally responsible for payment

of the loan under its original terms. A payment plan involves

the borrower making payments that differ from the contractual

payment amount for a short period of time, generally three

months. PNC’s motivation is to allow for repayment of an

outstanding past due amount through payment of additional

amounts over the short period of time. These payment plans

are generally for three months during which time a borrower

is brought current. Due to the short term of the payment plan

and the expectation that all contractual principal and interest

will be collected, there is a minimal impact to the ALLL.

Under a HAMP trial payment period, we allow a borrower to

demonstrate successful payment performance before

contractually establishing an alternative payment amount.

Subsequent to successful borrower performance under a

HAMP trial payment period, we will change a loan’s

contractual terms and the loan would be classified as a TDR.

Additionally, we note that a borrower often is already

delinquent at the time he/she begins participating in the

HAMP trial payment period. As such, upon successful

completion, there is not a significant increase in the ALLL. If

the trial payment period is unsuccessful, the loan will be

charged-off, at the end of the trial payment period, to its

estimated fair value of the underlying collateral less costs to

sell. As of December 31, 2010 and 2009, 1,027 or $262

million and 42 or $15 million, respectively, of residential real

estate loans have been modified under the HAMP and were

still outstanding on our balance sheet.

Residential conforming and certain residential construction

loans have been permanently modified under HAMP or, if

they do not qualify for a HAMP modification, under PNC

developed programs, which in some cases may operate similar

to HAMP. These programs require first, a reduction of the

interest rate, followed by an extension of term and, if

appropriate, deferral or forgiveness of principal payments. In

October 2010, we signed a Service Provider Agreement for

the government-sponsored Second Lien Modification Program

and have begun modifying loans under this program. PNC

does not re-modify a defaulted modified loan except for

subsequent significant life events, as defined by the OCC in

Memorandum 2009-7. A re-modified loan continues to be

classified as a TDR for the remainder of its term regardless of

subsequent payment performance.

Loan modifications are evaluated and subject to classification

as a troubled debt restructuring (TDR) if the borrower is

experiencing financial difficulty and we grant a concession to

the borrower. TDRs typically result from our loss mitigation

activities and could include rate reductions and/or principal

forgiveness intended to minimize the economic loss and to

avoid foreclosure or repossession of collateral. Total

72