PNC Bank 2010 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

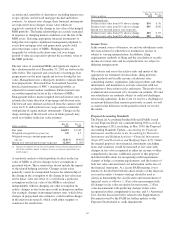

expected cash flows on the loans at the measurement date over

the recorded investment. Any decrease, other than for

prepayments or interest rate decreases for variable rate notes,

in the net present value of expected cash flows of individual

commercial or pooled consumer purchased impaired loans

would result in an impairment charge to the provision for loan

losses in the period in which the change is deemed probable.

Any increase in the net present value of expected cash flows

of purchased impaired loans would first result in a recovery of

previously recorded allowance for loan losses, to the extent

applicable, and then an increase to accretable yield for the

remaining life of the purchased impaired loans. See Note 6

Purchased Impaired Loans in the Notes To Consolidated

Financial Statements in Item 8 of this Report for additional

information.

Additionally, most consumer loans and lines of credit, not

secured by residential real estate, are charged off after 120 to

180 days past due, are not placed on nonaccrual status, and are

excluded from nonperforming loans.

The amount of nonperforming loans that was current as to

remaining principal and interest was $1.0 billion at

December 31, 2010 and $1.7 billion at December 31, 2009, or

22% and 30% of total nonperforming loans, respectively.

The portion of the ALLL allocated to commercial lending

nonperforming loans was 28% at December 31, 2010 and 29%

at December 31, 2009. Approximately 76% of total

nonperforming loans are secured by collateral that is expected

to reduce credit losses and require less reserves in the event of

default.

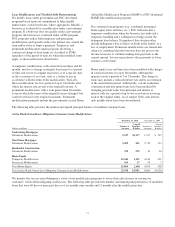

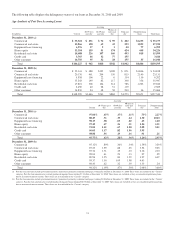

Nonperforming Assets By Type

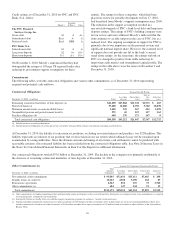

In millions

Dec. 31

2010

Dec. 31

2009

Nonperforming loans

Commercial

Retail/wholesale $ 197 $ 231

Manufacturing 250 423

Real estate related (a) 263 419

Financial services 16 117

Health care 50 41

Other 477 575

Total commercial 1,253 1,806

Commercial real estate

Real estate projects 1,422 1,754

Commercial mortgage 413 386

Total commercial real estate 1,835 2,140

Equipment lease financing 77 130

TOTAL COMMERCIAL LENDING 3,165 4,076

Consumer

Home equity 448 356

Residential real estate

Residential mortgage 764 955

Residential construction 54 248

Other 35 36

TOTAL CONSUMER LENDING 1,301 1,595

Total nonperforming loans 4,466 5,671

Foreclosed and other assets

Commercial lending 353 266

Consumer lending 482 379

Total foreclosed and other assets 835 645

Total nonperforming assets $5,301 $6,316

(a) Includes loans related to customers in the real estate and construction industries.

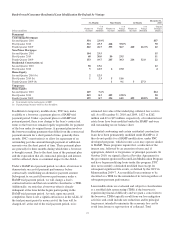

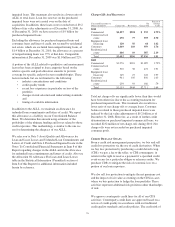

Change In Nonperforming Assets

In millions 2010 2009

January 1 $ 6,316 $ 2,181

Transferred from accrual 5,279 8,501

Charge-offs and valuation adjustments (2,071) (1,770)

Principal activity including payoffs (1,316) (1,127)

Asset sales and transfers to held for sale (1,446) (798)

Returned to performing-TDRs (543)

Returned to performing-Other (918) (671)

December 31 $ 5,301 $ 6,316

Total nonperforming loans and nonperforming assets in the

tables above are significantly lower than they would have

been due to the accounting treatment for purchased impaired

loans. This treatment also results in lower ratios of

nonperforming loans to total loans and ALLL to

nonperforming loans. We recorded purchased impaired loans

at estimated fair value, including life of loan credit losses, of

$12.7 billion at December 31, 2008. See Note 6 Purchased

Impaired Loans in the Notes To Consolidated Financial

Statements in Item 8 of this Report for additional information

on those loans.

70