PNC Bank 2010 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

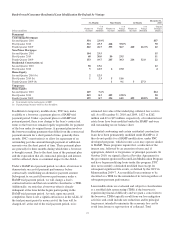

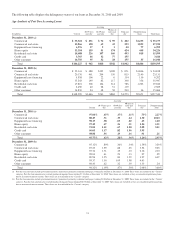

Commercial lending portfolio early stage delinquencies

(accruing loans past due 30 to 89 days) decreased substantially

from December 31, 2009 to December 31, 2010, generally due

to the improved economic environment and active portfolio

management. Consumer lending portfolio early stage

delinquencies improved modestly from December 31, 2009 to

December 31, 2010, due to declines in residential real estate

delinquencies.

Accruing loans past due 90 days or more are referred to as late

stage delinquencies and totaled $542 million at December 31,

2010, compared to $884 million at December 31, 2009,

reflecting the same factors as early stage delinquencies noted

above. These loans are not included in nonperforming loans

because they are well secured by collateral and in the process

of collection.

Additional information regarding accruing loans past due is

included in Note 5 Asset Quality and Allowances for Loan

and Lease Losses and Unfunded Loan Commitments and

Letters of Credit in the Notes To Consolidated Financial

Statements in Item 8 of this Report.

Our Special Asset Committee closely monitors loans that are

not included in nonperforming or past due categories and for

which we are uncertain about the borrower’s ability to comply

with existing repayment terms over the next six months. These

loans totaled $574 million at December 31, 2010 and $811

million at December 31, 2009.

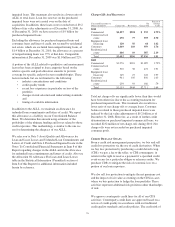

A

LLOWANCES FOR

L

OAN AND

L

EASE

L

OSSES AND

U

NFUNDED

L

OAN

C

OMMITMENTS AND

L

ETTERS OF

C

REDIT

We maintain an ALLL to absorb losses from the loan portfolio

and determine this allowance based on quarterly assessments

of the estimated probable credit losses incurred in the loan

portfolio. While we make allocations to specific loans and

pools of loans, the total reserve is available for all loan and

lease losses. There were no significant changes during 2010 to

the process and procedures we follow to determine our ALLL.

The ALLL was $4.9 billion at December 31, 2010 and $5.1

billion at December 31, 2009. The allowance as a percent of

nonperforming loans was 109% at December 31, 2010 and

89% at December 31, 2009. The allowance as a percent of

total loans was 3.25% at December 31, 2010 and 3.22% at

December 31, 2009.

We establish specific allowances for loans considered

impaired using a method prescribed by GAAP. All impaired

loans are subject to individual analysis, except leases and

large groups of smaller-balance homogeneous loans which

may include but are not limited to credit card, residential

mortgage, and consumer installment loans. Specific

allowances for individual loans are determined by our Special

Asset Committee based on an analysis of the present value of

expected future cash flows from the loans discounted at their

effective interest rate, observable market price, or the fair

value of the underlying collateral.

Allocations to commercial loan classes (pool reserve

methodology) are assigned to pools of loans as defined by our

business structure and are based on internal probability of

default and loss given default credit risk ratings.

Key elements of the pool reserve methodology include:

• Probability of default (PD), which is primarily based

on historical default analyses and is derived from the

borrower’s internal PD credit risk rating;

• Exposure at default (EAD), which is derived from

historical default data; and

• Loss given default (LGD), which is based on

historical loss data, collateral value and other

structural factors that may affect our ultimate ability

to collect on the loan and is derived from the loan’s

internal LGD credit risk rating.

Our pool reserve methodology is sensitive to changes in key

risk parameters such as PDs, LGDs and EADs. In general, a

given change in any of the major risk parameters will have a

corresponding change in the pool reserve allocations for

non-impaired commercial loans. Our commercial loans are the

largest category of credits and are most sensitive to changes in

the key risk parameters and pool reserve loss rates. To

illustrate, if we increase the pool reserve loss rates by 5% for

all categories of non-impaired commercial loans, then the

aggregate of the ALLL and allowance for unfunded loan

commitments and letters of credit would increase by $69

million. Additionally, other factors such as the rate of

migration in the severity of problem loans will contribute to

the final pool reserve allocations.

The majority of the commercial portfolio is secured by

collateral, including loans to asset-based lending customers

that continue to show demonstrably lower loss given default.

Further, the large investment grade or equivalent portion of

the loan portfolio has performed well and has not been subject

to significant deterioration. Additionally, guarantees on loans

greater than $1 million and owner guarantees for small

business loans do not significantly impact our ALLL.

Allocations to consumer loan classes are based upon a roll-

rate model based on statistical relationships, calculated from

historical data that estimate the movement of loan

outstandings through the various stages of delinquency and

ultimately charge-off. In general, the estimated rates at which

loan outstandings roll from one stage of delinquency to

another are dependent on various factors such as FICO, LTV

ratios, the current economic environment, and geography.

The ALLL is significantly lower than it would have been

otherwise due to the accounting treatment for purchased

75