PNC Bank 2010 Annual Report Download - page 152

Download and view the complete annual report

Please find page 152 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

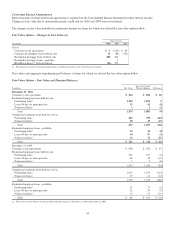

|

|

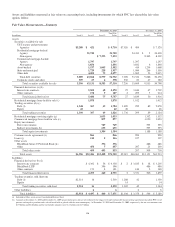

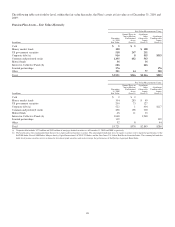

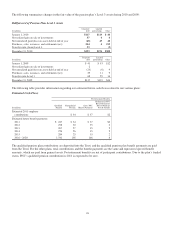

Amortization expense on existing intangible assets, net of

impairment reversal (charge) follows:

Amortization Expense on Existing Intangible Assets (a)

In millions

2008 $210

2009 296

2010 264

Estimated:

2011 256

2012 218

2013 205

2014 197

2015 186

(a) Net of impairment reversal (charge).

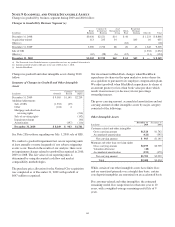

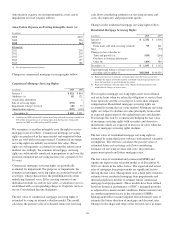

Changes in commercial mortgage servicing rights follow:

Commercial Mortgage Servicing Rights

In millions 2010 2009

January 1 $ 921 $ 864

Additions (a) 83 121

Acquisition adjustment 1

Sale of servicing rights (192)

Impairment (charge) reversal (40) 35

Amortization expense (107) (100)

December 31 $ 665 $ 921

(a) Additions for 2010 included $45 million from loans sold with servicing retained and

$38 million from purchases of servicing rights from third parties. Comparable

amounts for 2009 were $92 million and $29 million.

We recognize as an other intangible asset the right to service

mortgage loans for others. Commercial mortgage servicing

rights are purchased in the open market and originated when

loans are sold with servicing retained. Commercial mortgage

servicing rights are initially recorded at fair value. These

rights are subsequently accounted for using the amortization

method. Accordingly, the commercial mortgage servicing

rights are substantially amortized in proportion to and over the

period of estimated net servicing income over a period of 5 to

10 years.

Commercial mortgage servicing rights are periodically

evaluated for impairment. For purposes of impairment, the

commercial mortgage servicing rights are stratified based on

asset type, which characterizes the predominant risk of the

underlying financial asset. If the carrying amount of any

individual stratum exceeds its fair value, a valuation reserve is

established with a corresponding charge to Corporate services

on our Consolidated Income Statement.

The fair value of commercial mortgage servicing rights is

estimated by using an internal valuation model. The model

calculates the present value of estimated future net servicing

cash flows considering estimates on servicing revenue and

costs, discount rates and prepayment speeds.

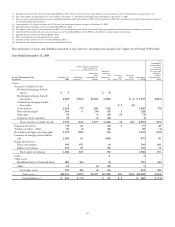

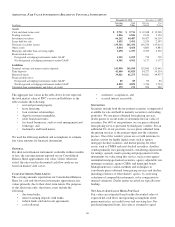

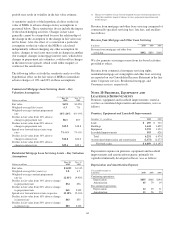

Changes in the residential mortgage servicing rights follow:

Residential Mortgage Servicing Rights

In millions 2010 2009

January 1 $ 1,332 $ 1,008

Additions:

From loans sold with servicing retained 95 261

Sales (74)

Changes in fair value due to:

Time and payoffs (a) (185) (264)

Purchase accounting adjustments 17

Other (b) (209) 384

December 31 $ 1,033 $ 1,332

Unpaid principal balance of loans serviced

for others at December 31 $125,806 $146,050

(a) Represents decrease in mortgage servicing rights value due to passage of time,

including the impact from both regularly scheduled loan principal payments and

loans that paid down or paid off during the period.

(b) Represents mortgage servicing rights value changes resulting primarily from

market-driven changes in interest rates.

We recognize mortgage servicing right assets on residential

real estate loans when we retain the obligation to service these

loans upon sale and the servicing fee is more than adequate

compensation. Residential mortgage servicing rights are

accounted for using the fair value method. Mortgage servicing

rights are subject to declines in value principally from actual

or expected prepayment of the underlying loans and defaults.

We manage this risk by economically hedging the fair value

of mortgage servicing rights with securities and derivative

instruments which are expected to increase in value when the

value of mortgage servicing rights declines.

The fair value of residential mortgage servicing rights is

estimated by using third party software with internal valuation

assumptions. The software calculates the present value of

estimated future net servicing cash flows considering

estimates on servicing revenue and costs, discount rates,

prepayment speeds and future mortgage rates.

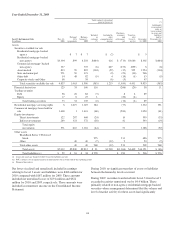

The fair value of residential and commercial MSRs and

significant inputs to the valuation model as of December 31,

2010 are shown in the tables below. The expected and actual

rates of mortgage loan prepayments are significant factors

driving the fair value. Management uses a third party model to

estimate future residential mortgage loan prepayments and

internal proprietary models to estimate future commercial

mortgage loan prepayments. These models have been refined

based on historical performance of PNC’s managed portfolio,

as adjusted for current market conditions. Future interest rates

are another important factor in the valuation of MSRs.

Management utilizes market implied forward interest rates to

estimate the future direction of mortgage and discount rates.

Changes in the shape and slope of the forward curve in future

144