PNC Bank 2010 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

C

ONSOLIDATED

I

NCOME

S

TATEMENT

R

EVIEW

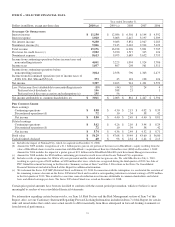

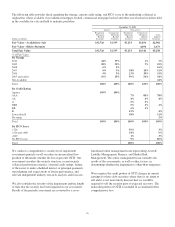

Net income for 2010 was $3.4 billion compared with

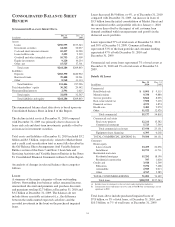

$2.4 billion for 2009. Results for 2010 include the impact of a

$328 million after-tax gain related to our sale of GIS. Results

for 2009 include the impact of a $687 million after-tax gain

resulting from BlackRock’s acquisition of BGI. Our

Consolidated Income Statement is presented in Item 8 of this

Report.

N

ET

I

NTEREST

I

NCOME AND

N

ET

I

NTEREST

M

ARGIN

Year ended December 31

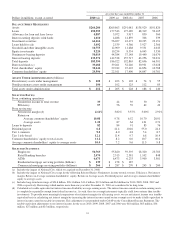

Dollars in millions 2010 2009

Net interest income $9,230 $9,083

Net interest margin 4.14% 3.82%

Changes in net interest income and margin result from the

interaction of the volume and composition of interest-earning

assets and related yields, interest-bearing liabilities and related

rates paid, and noninterest-bearing sources of funding. See the

Statistical Information (Unaudited) – Analysis Of

Year-To-Year Changes In Net Interest Income and Average

Consolidated Balance Sheet And Net Interest Analysis in

Item 8 of this Report for additional information.

The increase in net interest income for 2010 compared with

2009 resulted primarily from the impact of lower deposit and

borrowing costs somewhat offset by lower purchase

accounting accretion, lower loan volume and lower revenue

from our investment securities portfolio. Our deposit strategy

included the retention and repricing at lower rates of

relationship-based certificates of deposit and the planned run

off of maturing non-relationship certificates of deposit and

brokered deposits.

As further discussed in the Retail Banking section of the

Business Segments Review portion of this Item 7, the Credit

CARD Act of 2009 negatively impacted 2010 revenues by

approximately $75 million, largely in net interest income.

The net interest margin was 4.14% for 2010 and 3.82% for

2009. The following factors impacted the comparison:

• A decrease in the rate accrued on interest-bearing

liabilities of 49 basis points. The rate accrued on

interest-bearing deposits, the largest component,

decreased 47 basis points.

• A decrease in the yield on interest-earning assets of

10 basis points. The yield on loans, the largest

portion of our interest-earning assets, increased only

1 basis point and was more than offset by the 102

basis point decline in yield on investment securities.

• The benefit of noninterest-bearing sources of funding

decreased 7 basis points primarily due to the decline

in interest rates.

We expect that our purchase accounting accretion will

decrease by as much as $700 million in 2011. Excluding the

impact of this factor, we expect our net interest income to

increase in 2011. Overall, we also expect that our net interest

margin will decline in 2011.

N

ONINTEREST

I

NCOME

Summary

Noninterest income was $5.9 billion in 2010, a decline of

$1.2 billion from $7.1 billion in 2009. Noninterest income for

2009 included the $1.1 billion pretax gain recognized on our

portion of the increase in BlackRock’s equity resulting from

the value of BlackRock shares issued in connection with

BlackRock’s acquisition of BGI.

Aside from the impact of the 2009 BlackRock/BGI gain,

lower noninterest income in 2010 reflected the impact of

decreases in the following: residential mortgage loan sales

revenue, the value of commercial mortgage servicing rights,

net hedging gains on residential mortgage servicing rights,

service charges on deposits including the negative impact of

the new Regulation E rules, and net gains on sales of

securities. Partially offsetting these items were lower OTTI

charges, higher asset management revenue, a fourth quarter

2010 gain on 7.5 million BlackRock common shares sold by

PNC as part of a BlackRock secondary common stock

offering and higher revenue from capital markets-related

products and services including merger and acquisition

advisory fees.

Additional Analysis

Asset management revenue was $1.1 billion in 2010 compared

with $858 million in 2009. This increase reflected higher

equity earnings from our BlackRock investment, improved

equity markets and client growth. Discretionary assets under

management at December 31, 2010 totaled $108 billion

compared with $103 billion at December 31, 2009.

Consumer services fees totaled $1.3 billion in both 2010 and

2009. Consumer service fees for 2010 reflected higher

volume-related transaction fees offset by lower brokerage fees

and the impact of the consolidation of the securitized credit

card portfolio.

Corporate services revenue totaled $1.1 billion in 2010 and

$1.0 billion in 2009. The increase was largely the result of

higher merger and acquisition advisory and ancillary

commercial mortgage servicing fees partially offset by a

reduction in the value of commercial mortgage servicing

rights largely driven by lower interest rates. Corporate

services fees include the noninterest component of treasury

management fees, which continued to be a strong contributor

to revenue.

Residential mortgage revenue totaled $699 million in 2010

compared with $990 million in 2009. The decline in 2010

reflected reduced loan sales revenue following the strong loan

origination refinance volume in 2009 and lower net hedging

gains on mortgage servicing rights.

31