PNC Bank 2010 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

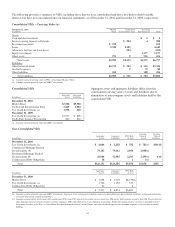

|

|

Dodd-Frank requires the Federal Reserve Board to establish

capital requirements that would, among other things, eliminate

the Tier 1 treatment of trust preferred securities following a

phase-in period expected to begin in 2013. Accordingly, PNC

will evaluate its alternatives, including the potential for early

redemption of some or all of its trust preferred securities,

based on such considerations it may consider relevant,

including dividend rates, the specifics of the future capital

requirements, capital market conditions and other factors.

PNC is also subject to replacement capital covenants with

respect to certain of its trust preferred securities as discussed

in Note 13 Capital Securities of Subsidiary Trusts and

Perpetual Trust Securities in the Notes To Consolidated

Financial Statements in Item 8 of this Report.

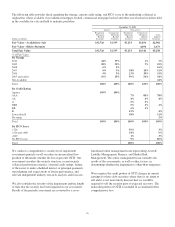

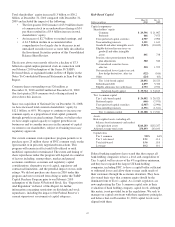

Our Tier 1 common capital ratio was 9.8% at December 31,

2010, an increase of 380 basis points compared with 6.0% at

December 31, 2009. Our Tier 1 risk-based capital ratio

increased 70 basis points to 12.1% at December 31, 2010 from

11.4% at December 31, 2009. Increases in both ratios were

attributable to retention of earnings in 2010, the first quarter

2010 equity offering, the third quarter 2010 sale of GIS, and

lower risk-weighted assets. The increases in the Tier 1 risk-

based capital ratio noted above were offset by the impact of

the $7.6 billion first quarter 2010 redemption of the Series N

(TARP) Preferred Stock. See Note 18 Equity in the Notes To

Consolidated Financial Statements in Item 8 of this Report for

additional information regarding the Series N Preferred Stock

redemption.

At December 31, 2010, PNC Bank, N.A., our domestic bank

subsidiary, was considered “well capitalized” based on US

regulatory capital ratio requirements. To qualify as “well-

capitalized”, regulators currently require banks to maintain

capital ratios of at least 6% for tier 1 risk-based, 10% for total

risk-based, and 5% for leverage. See the Supervision And

Regulation section of Item 1 of this Report and Note 21

Regulatory Matters in the Notes To Consolidated Financial

Statements in Item 8 of this Report for additional information.

We believe PNC Bank, N.A. will continue to meet these

requirements during 2011.

The access to, and cost of, funding for new business initiatives

including acquisitions, the ability to engage in expanded

business activities, the ability to pay dividends, the level of

deposit insurance costs, and the level and nature of regulatory

oversight depend, in part, on a financial institution’s capital

strength.

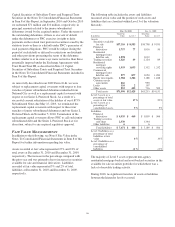

O

FF

-B

ALANCE

S

HEET

A

RRANGEMENTS

A

ND

V

ARIABLE

I

NTEREST

E

NTITIES

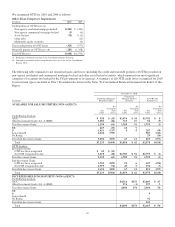

We engage in a variety of activities that involve

unconsolidated entities or that are otherwise not reflected in

our Consolidated Balance Sheet that are generally referred to

as “off-balance sheet arrangements.” Additional information

on these types of activities is included in the following

sections of this Report:

• Commitments, including contractual obligations and

other commitments, included within the Risk

Management section of this Financial Review,

• Note 3 Loan Sale and Servicing Activities and

Variable Interest Entities in the Notes To

Consolidated Financial Statements included in Item 8

of this Report,

• Note 13 Capital Securities of Subsidiary Trusts and

Perpetual Trust Securities in the Notes To

Consolidated Financial Statements included in Item 8

of this Report, and

• Note 23 Commitments and Guarantees in the Notes

To Consolidated Financial Statements included in

Item 8 of this Report.

On January 1, 2010, we adopted ASU 2009-17 –

Consolidations (Topic 810) – Improvements to Financial

Reporting by Enterprises Involved with Variable Interest

Entities. This guidance removes the scope exception for

qualifying special-purpose entities, contains new criteria for

determining the primary beneficiary of a variable interest

entity (VIE) and increases the frequency of required

reassessments to determine whether an entity is the primary

beneficiary of a VIE. VIEs are assessed for consolidation

under Topic 810 when we hold variable interests in these

entities. PNC consolidates VIEs when we are deemed to be

the primary beneficiary. The primary beneficiary of a VIE is

determined to be the party that meets both of the following

criteria: (1) has the power to make decisions that most

significantly affect the economic performance of the VIE and

(2) has the obligation to absorb losses or the right to receive

benefits that in either case could potentially be significant to

the VIE. Effective January 1, 2010, we consolidated Market

Street, a credit card securitization trust, and certain Low

Income Housing Tax Credit (LIHTC) investments. We

recorded consolidated assets of $4.2 billion, consolidated

liabilities of $4.2 billion, and an after-tax cumulative effect

adjustment to retained earnings of $92 million upon adoption.

43