PNC Bank 2010 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

We are committed to providing credit and liquidity to

qualified borrowers. Total loan originations and new

commitments and renewals totaled $149 billion for 2010.

Our loan portfolio continued to be diversified among

numerous industries and types of businesses. The loans that

we hold are also concentrated in, and diversified across, our

principal geographic markets.

Commercial lending is the largest category and is the most

sensitive to changes in assumptions and judgments underlying

the determination of the ALLL. This estimate also considers

other relevant factors such as:

• Actual versus estimated losses,

• Regional and national economic conditions,

• Business segment and portfolio concentrations,

• Industry conditions,

• The impact of government regulations, and

• Risk of potential estimation or judgmental errors,

including the accuracy of risk ratings.

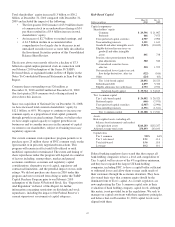

Higher Risk Loans

Our loan portfolio includes certain loans deemed to be higher

risk and therefore more likely to result in credit losses. We

established specific and pooled reserves on the total

commercial lending category of $2.6 billion at December 31,

2010. This commercial lending reserve included what we

believe to be adequate and appropriate loss coverage on the

higher risk commercial loans in the total commercial portfolio.

The commercial lending reserve represented 53% of the total

ALLL of $4.9 billion at that date. The remaining 47% of the

ALLL pertained to the total consumer lending category. This

category of loans is more homogenous in nature and has

certain characteristics that can be assessed at a total portfolio

level in terms of loans representing higher risk. We do not

consider government insured/government guaranteed loans to

be higher risk as we do not believe these loans will result in a

significant loss because of their structure. Additional

information regarding our higher risk loans is included in Note

5 Asset Quality and Allowances for Loan and Lease Losses

and Unfunded Loan Commitments and Letters of Credit in the

Notes To Consolidated Financial Statements included in

Item 8 of this Report.

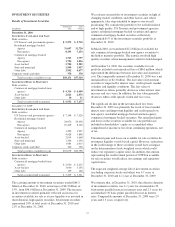

Information related to purchased impaired loans, purchase

accounting accretion and accretable net interest recognized

during 2010 and 2009 in connection with our acquisition of

National City follows.

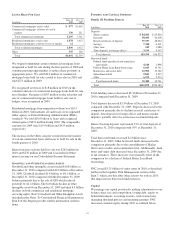

Valuation of Purchased Impaired Loans

December 31, 2008 December 31, 2009 December 31, 2010

Dollars in billions Balance Net Investment Balance Net Investment Balance Net Investment

Commercial and commercial real estate loans:

Unpaid principal balance $ 6.3 $ 3.5 $ 1.8

Purchased impaired mark (3.4) (1.3) (.4)

Recorded investment 2.9 2.2 1.4

Allowance for loan losses (.2) (.3)

Net investment 2.9 46% 2.0 57% 1.1 61%

Consumer and residential mortgage loans:

Unpaid principal balance 15.6 11.7 7.9

Purchased impaired mark (5.8) (3.6) (1.5)

Recorded investment 9.8 8.1 6.4

Allowance for loan losses (.3) (.6)

Net investment 9.8 63% 7.8 67% 5.8 73%

Total purchased impaired loans:

Unpaid principal balance 21.9 15.2 9.7

Purchased impaired mark (9.2) (4.9) (1.9)

Recorded investment 12.7 10.3 7.8

Allowance for loan losses (.5) (.9)(a)

Net investment $12.7 58% $ 9.8 64% $ 6.9 71%

(a) Impairment reserves of $.9 billion at December 31, 2010 reflect impaired loans with further credit quality deterioration since acquisition. This deterioration was more than offset by

the cash received to date in excess of recorded investment of $.7 billion and the net reclassification to accretable net interest, to be recognized over time, of $1.1 billion.

35