PNC Bank 2010 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

risks at pool and exposure levels while we estimate the

remaining risk types at an institution or business segment

level. We routinely compare the output of our economic

capital model with industry benchmarks.

Risk Control Strategies

Risk management is not about eliminating risks, but about

identifying and accepting risks and then working to effectively

manage them so as to optimize shareholder value.

We centrally manage policy development and exception

approval and oversight through corporate-level risk

management. Some of these policies express our risk appetite

through limits to the acceptable level of risk. We are in excess

of certain limits and are progressively managing to bring our

risks within policy. We are also reviewing and revising certain

policies to better reflect our larger and more complex

organization. Corporate risk management is authorized to take

action to either prevent or mitigate unapproved exceptions to

policies and is responsible for monitoring compliance with

risk management policies. The Corporate Audit function

performs an independent assessment of the internal control

environment. Corporate Audit plays a critical role in risk

management, testing the operation of the internal control

system and reporting findings to management and to the Audit

Committee of the Board.

Risk Monitoring

Corporate Risk Management reports on a regular basis to our

Board regarding the enterprise risk profile of the Corporation.

These reports aggregate and present the level of risk by type

of risk and communicate significant risk issues, including

performance relative to risk tolerance limits. Both the Board

and the EC provide guidance on actions to address key risk

issues as identified in these reports.

C

REDIT

R

ISK

M

ANAGEMENT

Credit risk represents the possibility that a customer,

counterparty or issuer may not perform in accordance with

contractual terms. Credit risk is inherent in the financial

services business and results from extending credit to

customers, purchasing securities, and entering into financial

derivative transactions and certain guarantee contracts. Credit

risk is one of our most significant risks.

Approved risk tolerances, in addition to credit policies and

procedures, set portfolio objectives for the level of credit risk.

We have established guidelines for problem loans, acceptable

levels of total borrower exposure, and other credit measures.

We seek to achieve our credit portfolio objectives by

maintaining a customer base that is diverse in borrower

exposure and industry types. We use loan sales and

syndications and the purchase of credit derivatives to reduce

risk concentrations. Corporate Credit personnel also

participate in loan underwriting and approval processes to

help ensure that newly approved loans meet policy and

portfolio objectives.

The credit granting businesses maintain direct responsibility

for monitoring credit risk within PNC. The Corporate Credit

Policy area provides independent oversight to the

measurement, monitoring and reporting of our credit risk and

reports to the Chief Risk Officer. Corporate Audit also

provides an independent assessment of the effectiveness of the

credit risk management process. We also manage credit risk in

accordance with regulatory guidance.

N

ONPERFORMING

A

SSETS

,T

ROUBLED

D

EBT

R

ESTRUCTURINGS

A

ND

L

OAN

D

ELINQUENCIES

Credit quality showed signs of improvement during 2010 and

delinquency measures improved compared with prior periods.

During 2010, we continued to see an improvement in credit

migration for performing loans and a reduction in overall

credit exposure.

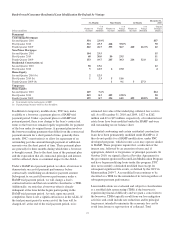

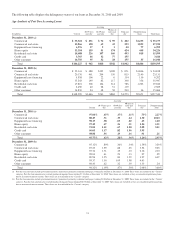

Nonperforming assets decreased $1.0 billion to $5.3 billion at

December 31, 2010 compared with $6.3 billion at

December 31, 2009. Nonperforming loans decreased

$1.2 billion to $4.5 billion since December 31, 2009 while

foreclosed and other assets increased $190 million to

$835 million. The decrease in nonperforming loans was

primarily due to improvements in our commercial lending and

residential real estate portfolios, partially offset by increases

in our consumer home equity portfolio. These consumer home

equity nonperforming loan increases were largely due to

increases in troubled debt restructurings (TDRs), as discussed

in more detail below. Our foreclosed and other assets levels

remained elevated as additions exceeded the ongoing high

level of asset sales and other reductions. As of year-end,

approximately 58% of our foreclosed and other assets are

composed of single family residential properties.

Nonperforming assets fell to 3.50% of total loans and

foreclosed and other assets at December 31, 2010 compared

with 3.99% at December 31, 2009. Loans held for sale are

excluded from nonperforming loans.

Nonperforming assets at December 31, 2010 declined in the

Corporate & Institutional Banking, Asset Management Group,

Residential Mortgage Banking, and Distressed Assets

Portfolio business segments compared with the balances at

December 31, 2009 and increased 18% in the Retail Banking

business segment. Increases in Retail Banking nonperforming

assets largely reflect the addition of consumer TDRs.

At December 31, 2010, our largest nonperforming asset was

$35 million in the Accommodation and Food Services

Industry and our average nonperforming loan associated with

commercial lending was approximately $1 million.

Purchased impaired loans are excluded from nonperforming

loans. These loans are considered performing, even if

contractually past due (or if we do not expect to receive

payment in full based on the original contractual terms), as we

are currently accreting interest income over the expected life

of the loans. The accretable yield represents the excess of the

69