PNC Bank 2010 Annual Report Download - page 125

Download and view the complete annual report

Please find page 125 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

Franklin business unit. The SPE or VIE was formed with a

small equity contribution and was structured as a bankruptcy-

remote entity so that its creditors had no recourse to the

sponsor. In exchange for a perfected security interest in the

cash flows of the nonconforming mortgage loans, the SPE

issued asset-backed securities to the sponsor in the form of

senior, mezzanine, and subordinated equity notes.

The SPE was deemed to be a VIE as its equity was not

sufficient to finance its activities. We were determined to be

the primary beneficiary of the SPE as we would absorb the

majority of the expected losses of the SPE through our

holding of the asset-backed securities. Accordingly, this SPE

was consolidated and all of the entity’s assets, liabilities, and

equity associated with the note tranches held by us were

intercompany balances and were eliminated in consolidation.

In October 2010, the governing documents were amended to

give us the option to unilaterally terminate the SPE. On

October 28, 2010, we exercised this option. The dissolution of

the SPE did not have any impact on the statement of financial

condition, liquidity, or cash flows of PNC. At December 31,

2009, nonconforming mortgage loans and foreclosed

properties associated with the consolidated SPE had a net

carrying value of $587 million.

In connection with the credit risk transfer agreement, we held

the right to put the mezzanine notes to the independent third-

party once credit losses in the mortgage loan pool exceeded

the principal balance of the subordinated equity notes. During

2009, cumulative credit losses in the mortgage loan pool

surpassed the principal balance of the subordinated equity

notes which resulted in us exercising our put option on two of

the subordinate mezzanine notes. Cash proceeds received

from the third party for the exercise of these put options

totaled $36 million. In addition, during 2009 we entered into

an agreement with the third party to terminate each party’s

rights and obligations under the credit risk transfer agreement

for the remaining mezzanine notes. We agreed to terminate

our contractual right to put the remaining mezzanine notes to

the third party for a cash payment of $126 million. A pretax

gain of $10 million was recognized in noninterest income as a

result of these transactions. The foregoing events did not have

any impact on our consolidation assessment of the SPE.

R

ESIDENTIAL AND

C

OMMERCIAL

M

ORTGAGE

-B

ACKED

S

ECURITIZATIONS

In connection with each Agency and Non-Agency

securitization discussed above, we evaluate each SPE utilized

in these transactions for consolidation. In performing these

assessments, we evaluate our level of continuing involvement

in these transactions as the magnitude of our involvement

ultimately determines whether or not we hold a variable

interest and/or are the primary beneficiary of the SPE. Factors

we consider in our consolidation assessment include the

significance of (1) our role as servicer, (2) our holdings of

mortgage-backed securities issued by the securitization SPE,

and (3) the rights of third-party variable interest holders.

Our first step in our assessment is to determine whether we

hold a variable interest in the securitization SPE. We hold a

variable interest in an Agency and Non-Agency securitization

SPE through our holding of mortgage-backed securities issued

by the SPE and/or our repurchase and recourse obligations.

Each SPE in which we hold a variable interest is evaluated to

determine whether we are the primary beneficiary of the

entity. For Agency securitization transactions, our contractual

role as servicer does not give us the power to direct the

activities that most significantly affect the economic

performance of the SPEs. Thus, we are not the primary

beneficiary of these entities. For Non-Agency securitization

transactions, we would be the primary beneficiary to the

extent our servicing activities give us the power to direct the

activities that most significantly affect the economic

performance of the SPE and we hold a more than insignificant

variable interest in the entity. At December 31, 2010, our level

of continuing involvement in Non-Agency securitization SPEs

did not result in PNC being deemed the primary beneficiary of

any of these entities. Details about the Agency and

Non-Agency securitization SPEs where we hold a variable

interest and are not the primary beneficiary are included in the

table above. Our maximum exposure to loss as a result of our

involvement with these SPEs is the carrying value of the

mortgage-backed securities, servicing assets, servicing

advances, and our liabilities associated with our repurchase

and recourse obligations. Creditors of the securitization SPEs

have no recourse to PNC’s assets or general credit.

N

OTE

4L

OANS AND

C

OMMITMENTS

T

O

E

XTEND

C

REDIT

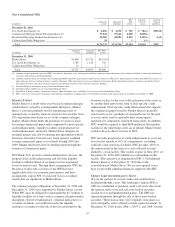

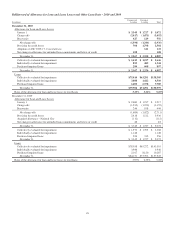

Loans outstanding were as follows:

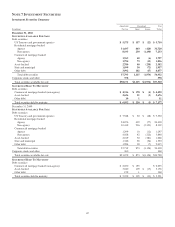

L

OANS

O

UTSTANDING

In millions

Dec. 31

2010

Dec. 31

2009

Commercial lending

Commercial $ 55,177 $ 54,818

Commercial real estate 17,934 23,131

Equipment lease financing 6,393 6,202

TOTAL COMMERCIAL LENDING 79,504 84,151

Consumer lending

Home equity 34,226 35,947

Residential real estate 15,999 19,810

Credit card 3,920 2,569

Other 16,946 15,066

TOTAL CONSUMER LENDING 71,091 73,392

Total loans (a) (b) $150,595 $157,543

(a) Net of unearned income, net deferred loan fees, unamortized discounts and

premiums, and purchase discounts and premiums totaling $2.7 billion and $3.2

billion at December 31, 2010 and December 31, 2009, respectively.

(b) Future accretable yield related to purchased impaired loans is not included in loans

outstanding.

Concentrations of credit risk exist when changes in economic,

industry or geographic factors similarly affect groups of

117