PNC Bank 2010 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

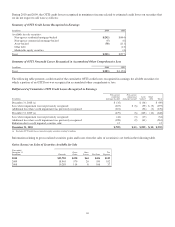

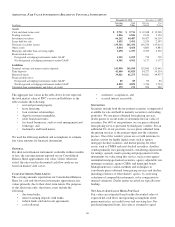

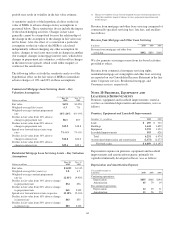

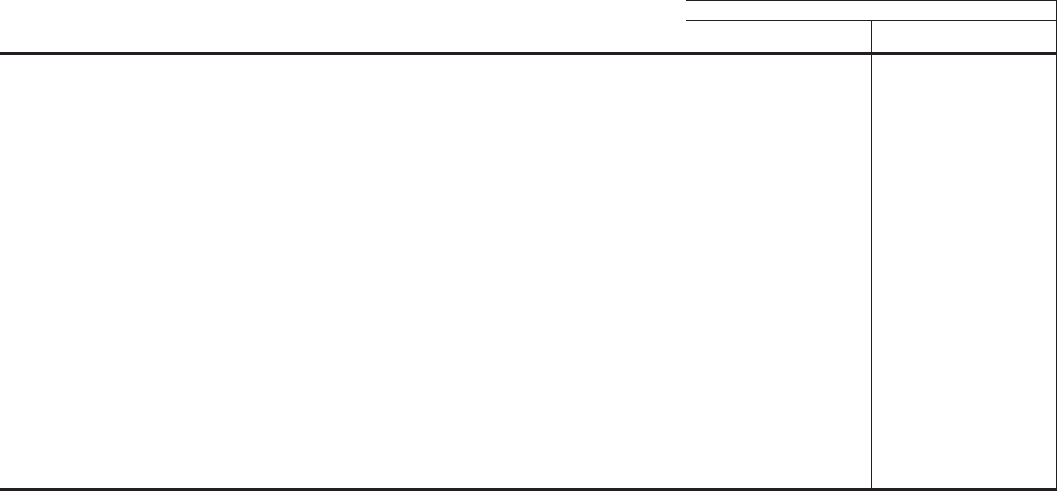

|

|

A

DDITIONAL

F

AIR

V

ALUE

I

NFORMATION

R

ELATED TO

F

INANCIAL

I

NSTRUMENTS

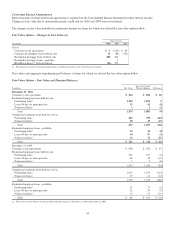

December 31, 2010 December 31, 2009

In millions

Carrying

Amount

Fair

Value

Carrying

Amount

Fair

Value

Assets

Cash and short-term assets $ 9,711 $ 9,711 $ 12,248 $ 12,248

Trading securities 1,826 1,826 2,124 2,124

Investment securities 64,262 64,487 56,027 56,319

Loans held for sale 3,492 3,492 2,539 2,597

Net loans (excludes leases) 139,316 141,431 146,270 145,014

Other assets 4,664 4,664 4,883 4,883

Mortgage and other loan servicing rights 1,698 1,707 2,253 2,352

Financial derivatives

Designated as hedging instruments under GAAP 1,255 1,255 739 739

Not designated as hedging instruments under GAAP 4,502 4,502 3,177 3,177

Liabilities

Demand, savings and money market deposits 141,990 141,990 132,645 132,645

Time deposits 41,400 41,825 54,277 54,534

Borrowed funds 39,821 41,273 39,621 39,977

Financial derivatives

Designated as hedging instruments under GAAP 85 85 95 95

Not designated as hedging instruments under GAAP 4,850 4,850 3,744 3,744

Unfunded loan commitments and letters of credit 173 173 290 290

The aggregate fair values in the table above do not represent

the total market value of PNC’s assets and liabilities as the

table excludes the following:

• real and personal property,

• lease financing,

• loan customer relationships,

• deposit customer intangibles,

• retail branch networks,

• fee-based businesses, such as asset management and

brokerage, and

• trademarks and brand names.

We used the following methods and assumptions to estimate

fair value amounts for financial instruments.

G

ENERAL

For short-term financial instruments realizable in three months

or less, the carrying amount reported on our Consolidated

Balance Sheet approximates fair value. Unless otherwise

stated, the rates used in discounted cash flow analyses are

based on market yield curves.

C

ASH

A

ND

S

HORT

-T

ERM

A

SSETS

The carrying amounts reported on our Consolidated Balance

Sheet for cash and short-term investments approximate fair

values primarily due to their short-term nature. For purposes

of this disclosure only, short-term assets include the

following:

• due from banks,

• interest-earning deposits with banks,

• federal funds sold and resale agreements,

• cash collateral,

• customers’ acceptances, and

• accrued interest receivable.

S

ECURITIES

Securities include both the investment securities (comprised of

available for sale and held to maturity securities) and trading

portfolios. We use prices obtained from pricing services,

dealer quotes or recent trades to determine the fair value of

securities. For 60% of our positions, we use prices obtained

from pricing services provided by third party vendors. For an

additional 8% of our positions, we use prices obtained from

the pricing services as the primary input into the valuation

process. One of the vendors’ prices are set with reference to

market activity for highly liquid assets such as agency

mortgage-backed securities, and matrix pricing for other

assets, such as CMBS and asset-backed securities. Another

vendor primarily uses pricing models considering adjustments

for ratings, spreads, matrix pricing and prepayments for the

instruments we value using this service, such as non-agency

residential mortgage-backed securities, agency adjustable rate

mortgage securities, agency CMOs and municipal bonds.

Management uses various methods and techniques to

corroborate prices obtained from pricing services and dealers,

including reference to other dealers’ quotes, by reviewing

valuations of comparable instruments, or by comparison to

internal valuations. Dealer quotes received are typically non-

binding.

N

ET

L

OANS

A

ND

L

OANS

H

ELD

F

OR

S

ALE

Fair values are estimated based on the discounted value of

expected net cash flows incorporating assumptions about

prepayment rates, net credit losses and servicing fees. For

purchased impaired loans, fair value is assumed to equal

141