PNC Bank 2010 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

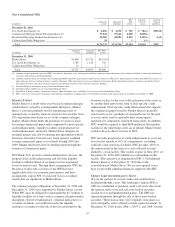

|

|

Specific reserve allocations are determined as follows:

• For nonperforming loans greater than or equal to a

defined dollar threshold and TDRs, specific reserves

are based on an analysis of the present value of the

loan’s expected future cash flows, the loan’s

observable market price or the fair value of the

collateral.

• For nonperforming loans below the defined dollar

threshold, the loans are aggregated for purposes of

measuring specific reserve impairment using the

applicable loan’s LGD percentage multiplied by the

balance of the loans.

When applicable, this process is applied across all the loan

classes in a similar manner. However, as previously discussed,

certain consumer loans and lines of credit, not secured by

residential real estate, are charged off instead of being

classified as nonperforming.

Our credit risk management policies, procedures and practices

are designed to promote sound and fair lending standards

while achieving prudent credit risk management. We have

policies, procedures and practices that address financial

statement requirements, collateral review and appraisal

requirements, advance rates based upon collateral types,

appropriate levels of exposure, cross-border risk, lending to

specialized industries or borrower type, guarantor

requirements, and regulatory compliance.

See Note 5 Asset Quality and Allowances for Loan and Lease

Losses and Unfunded Loan Commitments and Letters of

Credit for additional information.

A

LLOWANCE

F

OR

U

NFUNDED

L

OAN

C

OMMITMENTS

A

ND

L

ETTERS

O

F

C

REDIT

We maintain the allowance for unfunded loan commitments

and letters of credit at a level we believe is adequate to absorb

estimated probable losses related to these unfunded credit

facilities. We determine the adequacy of the allowance based

on periodic evaluations of the unfunded credit facilities,

including an assessment of the probability of commitment

usage, credit risk factors, and the terms and expiration dates of

the unfunded credit facilities. The allowance for unfunded

loan commitments and letters of credit is recorded as a

liability on the Consolidated Balance Sheet. Net adjustments

to the allowance for unfunded loan commitments and letters of

credit are included in the provision for credit losses.

The reserve for unfunded loan commitments is estimated in a

manner similar to the methodology used for determining

reserves for similar funded exposures. However, there is one

important distinction. This distinction lies in the estimation of

the amount of these unfunded commitments that will become

funded. This is determined using a cash conversion factor or

loan equivalency factor, which is a statistical estimate of the

amount of an unfunded commitment that will fund over a

given period of time. Once the future funded amount is

estimated, the calculation of the allowance follows similar

methodologies to those employed for on-balance sheet

exposure.

See Note 5 Asset Quality and Allowances for Loan and Lease

Losses and Unfunded Loan Commitments and Letters of

Credit for additional information.

M

ORTGAGE

A

ND

O

THER

S

ERVICING

R

IGHTS

We provide servicing under various loan servicing contracts

for commercial, residential and other consumer loans. These

contracts are either purchased in the open market or retained

as part of a loan securitization or loan sale. All newly acquired

or originated servicing rights are initially measured at fair

value. Fair value is based on the present value of the expected

future cash flows, including assumptions as to:

• Deposit balances and interest rates for escrow and

reserve earnings,

• Discount rates,

• Stated note rates,

• Estimated prepayment speeds, and

• Estimated servicing costs.

For subsequent measurements of these assets, we have elected

to utilize either the amortization method or fair value

measurement based upon the asset class and our risk

management strategy for managing these assets. For

commercial mortgage loan servicing rights, we use the

amortization method. This election was made based on the

unique characteristics of the commercial mortgage loans

underlying these servicing rights with regard to market inputs

used in determining fair value and how we manage the risks

inherent in the commercial mortgage servicing rights assets.

Specific risk characteristics of commercial mortgages include

loan type, currency or exchange rate, interest rates, expected

cash flows and changes in the cost of servicing. We record

these servicing assets as Other intangible assets and amortize

them over their estimated lives based on estimated net

servicing income. On a quarterly basis, we test the assets for

impairment by categorizing the pools of assets underlying the

servicing rights into various strata. If the estimated fair value

of the assets is less than the carrying value, an impairment loss

is recognized and a valuation reserve is established.

For servicing rights related to residential real estate loans, we

apply the fair value method. This election was made to be

consistent with our risk management strategy to hedge

changes in the fair value of these assets. We manage this risk

by hedging the fair value of this asset with derivatives and

securities which are expected to increase in value when the

value of the servicing right declines. The fair value of these

servicing rights is estimated by using a cash flow valuation

model which calculates the present value of estimated future

net servicing cash flows, taking into consideration actual and

expected mortgage loan prepayment rates, discount rates,

servicing costs, and other economic factors which are

determined based on current market conditions. Expected

108