PNC Bank 2010 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

impaired loans. This treatment also results in a lower ratio of

ALLL to total loans. Loan loss reserves on the purchased

impaired loans were not carried over on the date of

acquisition. In addition, these loans were recorded net of $9.2

billion of fair value adjustments as of December 31, 2008. As

of December 31, 2010, we have reserves of $.9 billion for

purchased impaired loans.

Excluding the allowance for purchased impaired loans and

consumer loans and lines of credit, not secured by residential

real estate, which are excluded from nonperforming loans, of

$1.4 billion at December 31, 2010, the allowance as a percent

of nonperforming loans was 77% at that date. Comparable

information at December 31, 2009 was $1.0 billion and 72%.

A portion of the ALLL related to qualitative and measurement

factors has been assigned to loan categories based on the

relative specific and pool allocation amounts to provide

coverage for specific and pool reserve methodologies. These

factors include, but are not limited to, the following:

• industry concentrations and conditions

• credit quality trends

• recent loss experience in particular sectors of the

portfolio

• changes in risk selection and underwriting standards

and

• timing of available information.

In addition to the ALLL, we maintain an allowance for

unfunded loan commitments and letters of credit. We report

this allowance as a liability on our Consolidated Balance

Sheet. We determine this amount using estimates of the

probability of the ultimate funding and losses related to those

credit exposures. This methodology is similar to the one we

use for determining the adequacy of our ALLL.

We refer you to Note 5 Asset Quality and Allowances for

Loan and Lease Losses and Unfunded Loan Commitments and

Letters of Credit and Note 6 Purchased Impaired Loans in the

Notes To Consolidated Financial Statements in Item 8 of this

Report regarding changes in the ALLL and in the allowance

for unfunded loan commitments and letters of credit. Also see

the Allocation Of Allowance For Loan And Lease Losses

table in the Statistical Information (Unaudited) section of

Item 8 of this Report for additional information included

herein by reference.

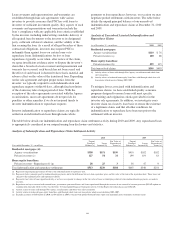

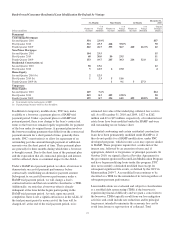

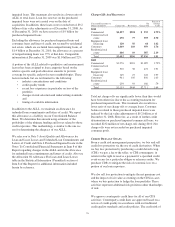

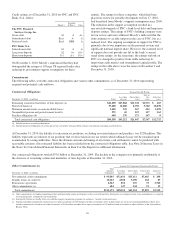

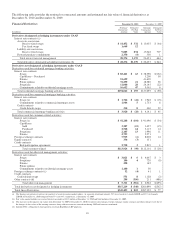

Charge-Offs And Recoveries

Year ended December 31

Dollars in millions Charge-offs Recoveries

Net

Charge-offs

Percent of

Average

Loans

2010

Commercial $1,227 $294 $ 933 1.72%

Commercial real

estate 670 77 593 2.90

Equipment lease

financing 120 56 64 1.02

Consumer 1,069 110 959 1.74

Residential real

estate 406 19 387 2.19

Total $3,492 $556 $2,936 1.91

2009

Commercial $1,276 $181 $1,095 1.79%

Commercial real

estate 510 38 472 1.91

Equipment lease

financing 149 27 122 1.97

Consumer 961 105 856 1.63

Residential real

estate 259 93 166 .79

Total $3,155 $444 $2,711 1.64

Total net charge-offs are significantly lower than they would

have been otherwise due to the accounting treatment for

purchased impaired loans. This treatment also results in a

lower ratio of net charge-offs to average loans. Customer

balances related to these purchased impaired loans were

reduced by the fair value adjustments of $9.2 billion as of

December 31, 2008. However, as a result of further credit

deterioration on purchased impaired commercial loans, we

recorded $232 million of net charge-offs during 2010. Net

charge-offs were not recorded on purchased impaired

consumer pools.

C

REDIT

D

EFAULT

S

WAPS

From a credit risk management perspective, we buy and sell

credit loss protection via the use of credit derivatives. When

we buy loss protection by purchasing a credit default swap

(CDS), we pay a fee to the seller, or CDS counterparty, in

return for the right to receive a payment if a specified credit

event occurs for a particular obligor or reference entity. We

purchase CDSs to mitigate the risk of economic loss on a

portion of our loan exposures.

We also sell loss protection to mitigate the net premium cost

and the impact of fair value accounting on the CDS in cases

where we buy protection to hedge the loan portfolio. These

activities represent additional risk positions rather than hedges

of risk.

We approve counterparty credit lines for all of our CDS

activities. Counterparty credit lines are approved based on a

review of credit quality in accordance with our traditional

credit quality standards and credit policies. The credit risk of

76