PNC Bank 2010 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

Subprime mortgage loans for first liens with a LTV ratio of

equal to or greater than 90% and second liens are classified as

nonaccrual at 90 days past due. These loans are charged off as

discussed above.

Most consumer loans and lines of credit, not secured by

residential real estate, are charged off after 120 to 180 days

past due. Generally, they are not placed on nonaccrual status

as permitted by regulatory guidance.

If payment is received on a nonperforming loan, the payment

is first applied to the past due principal; once this principal

obligation has been fulfilled, payments are applied to recover

any partial charge-off related to the impaired loan that might

exist. Finally, if both past due principal and any partial

charge-off have been recovered, then the payment will result

in the recognition and recording of interest income. This

process is followed for impaired loans with the exception of

performing troubled debt restructurings (TDRs). Payments

received on performing TDRs and other modified loans will

be applied in accordance with the terms of the modified loan.

A loan is categorized as a TDR if a concession is granted due

to deterioration in the financial condition of the borrower.

TDRs may include certain modifications of terms of loans,

receipts of assets from debtors in partial or full satisfaction of

loans, or a combination thereof. Modified loans classified as

TDRs are included in nonperforming loans until returned to

performing status through the fulfilling of contractual terms

for a reasonable period of time (generally 6 months).

See Note 5 Asset Quality and Allowances for Loan and Lease

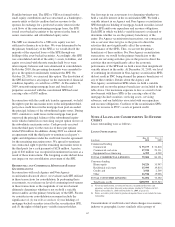

Losses and Unfunded Loan Commitments and Letters of

Credit for additional TDR information.

Nonperforming loans are generally not returned to performing

status until the obligation is brought current and the borrower

has performed in accordance with the contractual terms for a

reasonable period of time and collection of the contractual

principal and interest is no longer in doubt.

Foreclosed assets are comprised of any asset seized or

property acquired through a foreclosure proceeding or

acceptance of a deed-in-lieu of foreclosure. Other real estate

owned is comprised principally of commercial real estate and

residential real estate properties obtained in partial or total

satisfaction of loan obligations. When legal proceedings are

initiated, and no remedies arise from the legal proceedings, the

property will be sold. When we acquire the deed, we transfer

the loan to other real estate owned included in Other assets on

our Consolidated Balance Sheet. Property obtained in

satisfaction of a loan is recorded at the lower of recorded

investment or estimated fair value less cost to sell. We

estimate fair values primarily based on appraisals, when

available, or quoted market prices on liquid assets.

Anticipated recoveries and government guarantees are also

considered in evaluating the potential impairment of loans at

the date of transfer. If the estimated fair value less cost to sell

is less than the recorded investment, a charge-off is

recognized against the ALLL.

Subsequently, foreclosed assets are valued at the lower of the

amount recorded at acquisition date or estimated fair value

less cost to sell. Valuation adjustments on these assets and

gains or losses realized from disposition of such property are

reflected in Other noninterest expense.

See Note 5 Asset Quality and Allowances for Loan and Lease

Losses and Unfunded Loan Commitments and Letters of

Credit for additional information.

A

LLOWANCE

F

OR

L

OAN

A

ND

L

EASE

L

OSSES

We maintain the ALLL at a level that we believe to be

adequate to absorb estimated probable credit losses incurred in

the loan portfolio as of the balance sheet date. Our

determination of the adequacy of the allowance is based on

periodic evaluations of the loan and lease portfolios and other

relevant factors. This evaluation is inherently subjective as it

requires material estimates, all of which may be susceptible to

significant change, including, among others:

• Probability of default (PD),

• Loss given default (LGD),

• Exposure at date of default (EAD),

• Amounts and timing of expected future cash flows,

• Value of collateral, and

• Qualitative factors such as changes in economic

conditions that may not be reflected in historical

results.

While our reserve methodologies strive to reflect all relevant

risk factors, there continues to be uncertainty associated with,

but not limited to, potential imprecision in the estimation

process due to the inherent time lag of obtaining information

and normal variations between estimates and actual outcomes.

We provide additional reserves that are designed to provide

coverage for losses attributable to such risks. The ALLL also

includes factors which may not be directly measured in the

determination of specific or pooled reserves. Such qualitative

factors include:

• Recent Credit quality trends,

• Recent Loss experience in particular portfolios,

• Recent Macro economic factors, and

• Changes in risk selection and underwriting standards.

In determining the adequacy of the ALLL, we make specific

allocations to impaired loans and allocations to portfolios of

commercial and consumer loans. We also allocate reserves to

provide coverage for probable losses incurred in the portfolio

at the balance sheet date based upon current market

conditions, which may not be reflected in historical loss data.

While allocations are made to specific loans and pools of

loans, the total reserve is available for all credit losses.

Nonperforming loans are considered impaired under ASC

310-Receivables and are allocated a specific reserve.

107