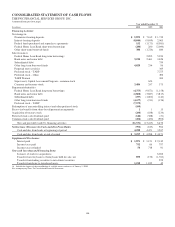

PNC Bank 2010 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

amended standard clarifies that an entity must consider all

arrangements or agreements made contemporaneously with or

in contemplation of a transfer even if not entered into at the

time of the transfer when applying surrender of control

conditions. See Recent Accounting Pronouncements in this

Note 1 for further details.

L

OANS

H

ELD

F

OR

S

ALE

We designate loans as held for sale when we have the intent to

sell them. We transfer loans to the Loans held for sale

category at the lower of cost or estimated fair value less cost

to sell. At the time of transfer, write-downs on the loans are

recorded as charge-offs. We establish a new cost basis upon

transfer. Any subsequent lower-of-cost-or-market adjustment

is determined on an individual loan basis and is recognized as

a valuation allowance with any charges included in Other

noninterest income. Gains or losses on the sale of these loans

are included in Other noninterest income when realized.

We have elected to account for certain commercial mortgage

loans held for sale at fair value. The changes in the fair value

of these loans are measured and recorded in Other noninterest

income each period. See Note 8 Fair Value for additional

information. Also, we elected to account for residential real

estate loans held for sale and securitizations acquired from

National City, which were not purchased impaired loans, at

fair value.

Interest income with respect to loans held for sale classified as

performing is accrued based on the principal amount

outstanding using a constant effective yield method.

In certain circumstances, loans designated as held for sale may

be transferred to held for investment based on a change in

strategy. We transfer these loans at the lower of cost or

estimated fair value; however, any loans held for sale and

designated at fair value will remain at fair value for the life of

the loan.

N

ONPERFORMING

A

SSETS

Nonperforming assets include:

• Nonaccrual loans,

• Troubled debt restructurings, and

• Foreclosed assets.

Nonperforming loans are those loans that have deteriorated in

credit quality to the extent that full collection of original

contractual principal and interest is doubtful. When a loan is

determined to be nonperforming (and as a result is impaired),

the accrual of interest is ceased and the loan is classified as

nonaccrual. The current year accrued and uncollected interest

is reversed out of net interest income.

A loan acquired and accounted for under ASC Sub-Topic

310-30 – Loans and Debt Securities Acquired with

Deteriorated Credit Quality is reported as an accruing loan and

a performing asset.

We generally classify Commercial Lending (Commercial,

Commercial Real Estate, and Equipment Lease Financing)

loans as nonaccrual (and therefore nonperforming) when we

determine that the collection of interest or principal is doubtful

or when delinquency of interest or principal payments has

existed for 90 days or more and the loans are not well-secured

and in the process of collection. A loan is considered well-

secured when the collateral in the form of liens on (or pledges

of) real or personal property, including marketable securities,

has a realizable value sufficient to discharge the debt in full,

including accrued interest. Such factors that would lead to

nonperforming status and subject to an impairment test would

include, but are not limited to, the following:

• Deterioration in the financial position of the borrower

resulting in the loan moving from accrual to cash

basis,

• The collection of principal or interest is 90 days or

more past due unless the asset is both well-secured

and in the process of collection,

• Reasonable doubt exists as to the certainty of the

future debt service ability, whether 90 days have

passed or not,

• Customer has filed or will likely file for bankruptcy,

• The bank advances additional funds to cover

principal or interest,

• We are in the process of liquidation of a commercial

borrower, or

• We are pursuing remedies under a guaranty.

We charge off commercial nonaccrual loans based on the facts

and circumstances of the individual loans.

Additionally, in general, small business commercial term

loans of less than $1 million and small business commercial

revolving loans are placed on nonaccrual status at 90 days past

due and charged off at 120 and 180 days past due,

respectively.

Home equity installment loans and lines of credit, as well as

residential real estate loans, that are well secured are classified

as nonaccrual at 180 days past due. A consumer loan is

considered well-secured when the collateral in the form of

liens on (or pledges of) real or personal property, including

marketable securities, have a realizable value sufficient to

discharge the debt in full, including accrued interest.

Home equity installment loans and lines of credit and

residential real estate loans that are not well secured and/or are

in the process of collection are charged off at 180 days past

due to the estimated fair value of the collateral less cost to sell.

The remaining portion of the loan is placed on nonaccrual

status.

106