PNC Bank 2010 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

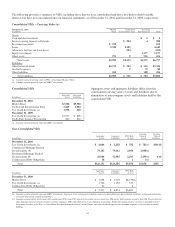

Average deposits were $43.8 billion for 2010, an increase of

$6.3 billion, or 17%, compared with 2009. During 2010,

customers continued to move balances to noninterest-bearing

demand deposits to maintain liquidity.

The commercial mortgage servicing portfolio was $266 billion

at December 31, 2010 compared with $287 billion at

December 31, 2009. The decrease was driven by the sale

during the second quarter of 2010 of a duplicative agency

servicing operation acquired with National City.

See the additional revenue discussion regarding treasury

management, capital markets-related products and services,

and commercial mortgage banking activities on page 32.

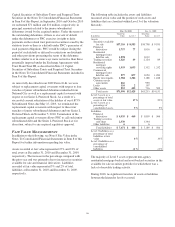

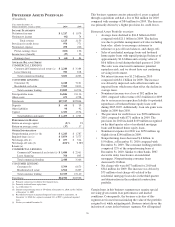

A

SSET

M

ANAGEMENT

G

ROUP

(Unaudited)

Year ended December 31

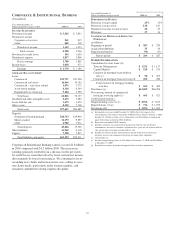

Dollars in millions except as noted 2010 2009

I

NCOME

S

TATEMENT

Net interest income $ 263 $ 308

Noninterest income 627 611

Total revenue 890 919

Provision for credit losses 20 97

Noninterest expense 647 654

Pretax earnings 223 168

Income taxes 82 63

Earnings $ 141 $ 105

A

VERAGE

B

ALANCE

S

HEET

Loans

Consumer $4,026 $3,957

Commercial and commercial real estate 1,501 1,639

Residential mortgage 850 1,078

Total loans 6,377 6,674

Goodwill and other intangible assets 399 407

Other assets 246 239

Total assets $7,022 $7,320

Deposits

Noninterest-bearing demand $1,324 $1,091

Interest-bearing demand 1,835 1,582

Money market 3,283 3,208

Total transaction deposits 6,442 5,881

Certificates of deposit and other 748 1,076

Total deposits 7,190 6,957

Other liabilities 89 104

Capital 534 569

Total liabilities and equity $7,813 $7,630

P

ERFORMANCE

R

ATIOS

Return on average capital 26% 18%

Return on average assets 2.01 1.43

Noninterest income to total revenue 70 66

Efficiency 73 71

O

THER

I

NFORMATION

Total nonperforming assets (a) (b) $90$ 155

Impaired loans (a) (c) $ 146 $ 198

Total net charge-offs $42$63

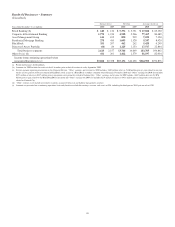

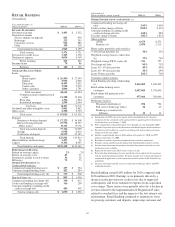

Year ended December 31

Dollars in millions except as noted 2010 2009

ASSETS UNDER ADMINISTRATION

(in billions) (a) (d)

Personal $99 $94

Institutional 113 111

Total $212 $205

Asset Type

Equity $115 $100

Fixed Income 63 58

Liquidity/Other 34 47

Total $212 $205

Discretionary assets under management

Personal $69 $67

Institutional 39 36

Total $108 $103

Asset Type

Equity $55 $49

Fixed Income 36 34

Liquidity/Other 17 20

Total $108 $103

Nondiscretionary assets under administration

Personal $30 $27

Institutional 74 75

Total $104 $102

Asset Type

Equity $60 $51

Fixed Income 27 24

Liquidity/Other 17 27

Total $104 $102

(a) As of December 31.

(b) Includes nonperforming loans of $82 million at December 31, 2010 and $149

million at December 31, 2009.

(c) Recorded investment of purchased impaired loans related to acquisitions.

(d) Excludes brokerage account assets.

Asset Management Group earned $141 million for 2010

compared with $105 million for 2009. The increase reflected a

lower provision for credit losses due to improved credit

quality and increased noninterest income from higher equity

markets and new client growth. These increases were partially

offset by lower net interest income from lower loan yields.

The business delivered strong performance in 2010 as it

remained focused on new client acquisition, client asset

growth and expense discipline.

Highlights of Asset Management Group’s performance during

2010 include the following:

• Successfully executed its National City trust system

and banking conversions while maintaining high

client satisfaction and retention,

• Achieved exceptional new sales and client

acquisition levels for the Group,

• Improved credit quality and performance, and

• Exceeded expense management targets while

investing in strategic growth initiatives.

54