PNC Bank 2010 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

Regulation E related to overdraft fees and to be negatively

impacted by the potential limits related to interchange rates on

debit card transactions proposed in Dodd-Frank. The

incremental negative impact of these two aspects of regulatory

reform on fees may be approximately $400 million in 2011 if

limits to interchange rates are implemented consistent with

rules currently proposed by the Federal Reserve Board.

Changes in the proposed interchange rules could impact this

estimate. Further, this estimate does not include any additional

impact to revenue of other or additional regulatory

requirements. There could be other aspects of regulatory

reform that further impact these or other areas of our business

as regulatory agencies, including the new CFPB, issue

proposed and final regulations pursuant to Dodd-Frank and

other legislation. See additional information regarding

legislative and regulatory developments in the Executive

Summary section of this Item 7.

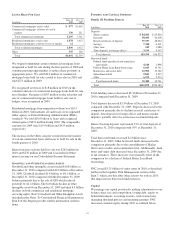

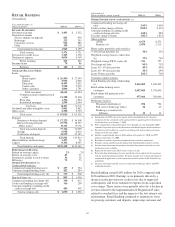

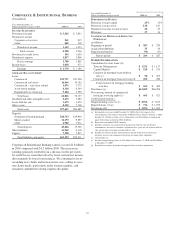

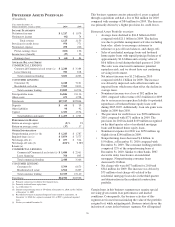

The provision for credit losses was $1.1 billion in 2010

compared with $1.3 billion in 2009. Net charge-offs were $1.1

billion in 2010 and essentially flat when compared with the

same period last year. These comparisons both benefited from

overall improved credit quality which was partially offset by

the previously mentioned consolidation of $1.6 billion in

credit card loans as of January 1, 2010. Credit quality has

shown signs of stabilization during 2010 with a declining net

charge-off trend in each of the last four quarters. The

improvement in net charge-off trends was predominately

driven by the small business commercial lending and credit

card portfolios. The increase in non-performing assets over the

prior year was primarily due to an increase in modified loans

reflecting continued efforts to work with borrowers

experiencing financial difficulties.

Noninterest expense for the year declined $115 million from

the same period last year. Expenses were well-managed as

continued investments in distribution channels were more than

offset by acquisition cost savings and the required branch

divestitures.

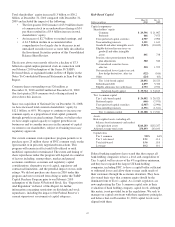

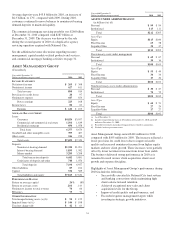

Growing core checking deposits as a lower-cost funding

source and as the cornerstone product to build customer

relationships is the primary objective of our deposit strategy.

Furthermore, core checking accounts are critical to our

strategy of expanding our payments business. The deposit

strategy of Retail Banking is to remain disciplined on pricing,

target specific products and markets for growth, and focus on

the retention and growth of balances for relationship

customers.

In 2010, average total deposits decreased $8.2 billion, or 6%,

compared with 2009.

• Average demand deposits increased $2.3 billion, or

7%, over 2009. The increase was primarily driven by

customer growth and customer preferences for

liquidity.

• Average money market deposits increased $731

million, or 2%, from 2009. The increase was

primarily due to core money market growth as

customers generally prefer more liquid deposits in a

low rate environment.

• In 2010, average certificates of deposit decreased

$11.6 billion from last year. This decline is expected

to continue in 2011, although at a slower pace, due to

the continued run off of higher rate certificates of

deposit that were primarily obtained through the

National City acquisition.

Currently, we plan to maintain our focus on a relationship-

based lending strategy that targets specific customer sectors

(mass consumers, homeowners, students, small businesses and

auto dealerships) and our moderate risk lending approach. In

2010, average total loans were $58.8 billion, an increase of

$2.1 billion, or 4%, over last year.

• Average education loans grew $2.9 billion compared

with 2009 primarily due to increases in federal loan

volumes as a result of non-bank competitors exiting

from the business, portfolio purchases, and the

impact of our current strategy of holding education

loans on the balance sheet. As previously noted, the

federally guaranteed portion of this business was

essentially eliminated going forward beginning

July 1, 2010 due to HCERA.

• Average credit card balances increased $1.7 billion

over 2009. The increase was primarily the result of

the consolidation of the securitized credit card

portfolio effective January 1, 2010.

• Average home equity loans declined $953 million

over 2009. Consumer loan demand remained soft in

the current economic climate. The decline is driven

by loan demand being outpaced by paydowns,

refinancings, and charge-offs. Retail Banking’s home

equity loan portfolio is relationship based, with 96%

of the portfolio attributable to borrowers in our

primary geographic footprint. The nonperforming

assets and charge-offs that we have experienced are

within our expectations given current market

conditions.

• Average commercial and commercial real estate

loans declined $1.1 billion compared with 2009. The

decline was primarily due to loan demand being

outpaced by refinancings, paydowns, charge-offs and

the required branch divestitures (approximately $0.2

billion of the decline on average).

51