PNC Bank 2010 Annual Report Download - page 169

Download and view the complete annual report

Please find page 169 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

used to hedge the fair value of residential mortgage servicing

rights include interest rate futures, swaps and options,

including caps, floors, and swaptions, and forward contracts to

purchase mortgage-backed securities. Gains and losses on

residential mortgage servicing rights and the related

derivatives used for hedging are included in residential

mortgage noninterest income.

Commercial mortgage loans are also sold into the secondary

market as part of our commercial mortgage banking activities

and are accounted for at fair value. Commitments related to

loans that will be sold are considered derivatives and are also

accounted for at fair value. Derivatives used to economically

hedge these loans and commitments from changes in fair

value due to interest rate risk and credit risk include forward

loan sale contracts, interest rate swaps, and credit default

swaps. Gains and losses on the commitments, loans and

derivatives are included in other noninterest income.

The residential and commercial loan commitments associated

with loans to be sold which are accounted for as derivatives

are valued based on the estimated fair value of the underlying

loan and the probability that the loan will fund within the

terms of the commitment. The fair value also takes into

account the fair value of the embedded servicing right.

We offer derivatives to our customers in connection with their

risk management needs. These derivatives primarily consist of

interest rate swaps, interest rate caps, floors, swaptions, and

foreign exchange and equity contracts. We primarily manage

our market risk exposure from customer transactions by

entering into offsetting derivative transactions with third-party

dealers. Gains and losses on customer-related derivatives are

included in other noninterest income.

The derivatives portfolio also includes derivatives used for

other risk management activities. These derivatives are

entered into based on stated risk management objectives.

This segment of the portfolio includes credit default swaps

(CDS) used to mitigate the risk of economic loss on a portion

of our loan exposure. We also sell loss protection to mitigate

the net premium cost and the impact of mark-to-market

accounting on CDS purchases to hedge the loan portfolio. The

fair values of these derivatives typically are based on related

credit spreads. Gains and losses on the derivatives entered into

for other risk management are included in other noninterest

income.

Included in the customer, mortgage banking risk management,

and other risk management portfolios are written interest-rate

caps and floors entered into with customers and for risk

management purposes. We receive an upfront premium from

the counterparty and are obligated to make payments to the

counterparty if the underlying market interest rate rises above

or falls below a certain level designated in the contract. At

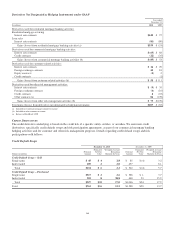

both December 31, 2010 and 2009, the fair value of the

written caps and floors liability on our Consolidated Balance

Sheet was $15 million. Our ultimate obligation under written

options is based on future market conditions and is only

quantifiable at settlement.

Further detail regarding the derivatives not designated in

hedging relationships is presented in the tables that follow.

D

ERIVATIVE

C

OUNTERPARTY

C

REDIT

R

ISK

By entering into derivative contracts we are exposed to credit

risk. We seek to minimize credit risk through internal credit

approvals, limits, monitoring procedures, executing master

netting agreements and collateral requirements. We generally

enter into transactions with counterparties that carry high

quality credit ratings. Nonperformance risk including credit

risk is included in the determination of the estimated net fair

value.

We generally have established agreements with our major

derivative dealer counterparties that provide for exchanges of

marketable securities or cash to collateralize either party’s

positions. At December 31, 2010, we held cash, US

government securities and mortgage-backed securities totaling

$837 million under these agreements. We pledged cash and

mortgage-backed securities of $699 million under these

agreements. To the extent not netted against derivative fair

values under a master netting agreement, cash pledged is

included in Other assets and cash held is included in Other

borrowed funds on our Consolidated Balance Sheet.

The credit risk associated with derivatives executed with

customers is essentially the same as that involved in extending

loans and is subject to normal credit policies. We may obtain

collateral based on our assessment of the customer’s credit

quality.

We periodically enter into risk participation agreements to

share some of the credit exposure with other counterparties

related to interest rate derivative contracts or to take on credit

exposure to generate revenue. We will make/receive payments

under these agreements if a customer defaults on its obligation

to perform under certain derivative swap contracts. Risk

participation agreements are included in the derivatives table

that follows. Our exposure related to risk participations where

we sold protection is discussed in the Credit Derivatives

section below.

C

ONTINGENT

F

EATURES

Some of PNC’s derivative instruments contain provisions that

require PNC’s debt to maintain an investment grade credit

rating from each of the major credit rating agencies. If PNC’s

debt ratings were to fall below investment grade, it would be

in violation of these provisions, and the counterparties to the

derivative instruments could request immediate payment or

demand immediate and ongoing full overnight

collateralization on derivative instruments in net liability

positions.

161