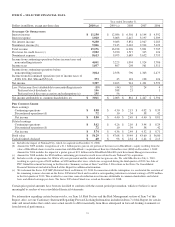

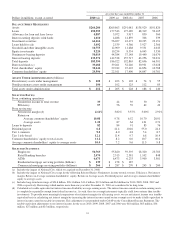

PNC Bank 2010 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

for PNC. It includes provisions that could increase regulatory

fees and deposit insurance assessments and impose heightened

capital and prudential standards, while at the same time

impacting the nature and costs of PNC’s businesses, including

consumer lending, private equity investment, derivatives

transactions, interchange fees on debit card transactions, and

asset securitizations.

Until such time as the regulatory agencies issue final

regulations implementing all of the numerous provisions of

Dodd-Frank, a process that will extend at least over the next

year and might last several years, PNC will not be able to fully

assess the impact the legislation will have on its businesses.

However, we believe that the expected changes will be

manageable for PNC and will have a smaller impact on us

than on our larger peers.

Included in these recent legislative and regulatory

developments are evolving regulatory capital standards for

financial institutions. Dodd-Frank requires the Federal

Reserve Board to establish capital requirements that would,

among other things, eliminate the Tier 1 treatment of trust

preferred securities following a phase-in period expected to

begin in 2013. Evolving standards also include the so-called

“Basel III” initiatives that are part of the Basel II effort by

international banking supervisors to update the original

international bank capital accord (Basel I), which has been in

effect since 1988. The recent Basel III capital initiative, which

has the support of US banking regulators, includes heightened

capital requirements for major banking institutions in terms of

both higher quality capital and higher regulatory capital ratios.

Basel III capital standards will require implementing

regulations by the banking regulators. These regulations will

become effective under a phase-in period beginning January 1,

2013, and will become fully effective January 1, 2019.

Dodd-Frank also establishes, as an independent agency that is

organized as a bureau within the Federal Reserve, the Bureau

of Consumer Financial Protection (CFPB). Starting July 21,

2011, the CFPB will have the authority to prescribe rules

governing the provision of consumer financial products and

services, and it is expected that the CFPB will issue new

regulations, and amend existing regulations, regarding

consumer protection practices. Also on that date, the authority

of the OCC to examine PNC Bank, N.A. for compliance with

consumer protection laws, and to enforce such laws, will

transfer to CFPB.

Additionally, new provisions concerning the applicability of

state consumer protection laws will become effective on

July 21, 2011. Questions may arise as to whether certain state

consumer financial laws that may have previously been

preempted are no longer preempted after this date. Depending

on how such questions are resolved, we may experience an

increase in regulation of our retail banking business and

additional compliance obligations, revenue impacts, and costs.

Dodd-Frank and its implementation, as well as other statutory

and regulatory initiatives that will be ongoing, will introduce

numerous regulatory changes over the next several years.

While we believe that we are well positioned to navigate

through this process, we cannot predict the ultimate impact of

these actions on PNC’s business plans and strategies.

R

ESIDENTIAL

M

ORTGAGE

F

ORECLOSURE

M

ATTERS

Beginning in the third quarter of 2010, mortgage foreclosure

documentation practices among US financial institutions

received heightened attention by regulators and the media.

PNC’s US market share for residential servicing is less than

2%. The vast majority of our servicing business is on behalf of

other investors, principally the Federal Home Loan Mortgage

Corporation (FHLMC) and the Federal National Mortgage

Association (FNMA). Following the initial reports regarding

these practices, we conducted an internal review of our

foreclosure procedures. Based upon our review, we believe

that PNC has systems designed to ensure that no foreclosure

proceeds unless the loan is genuinely in default. On average,

our residential mortgage loans are delinquent approximately

six months before foreclosure proceedings are initiated.

Similar to other banks, however, we identified issues

regarding some of our foreclosure practices. Accordingly, we

delayed pursuing individual foreclosures and are moving

forward on such matters only when we are confident that any

pending documentation issues had been resolved. We are also

proceeding with new foreclosures under enhanced procedures

designed as part of this review to minimize the risk of errors

related to the processing of documentation in foreclosure

cases.

In addition, the Federal Reserve and the OCC, together with

the FDIC and others, commenced a publicly-disclosed

interagency horizontal review of residential mortgage

servicing operations at PNC and thirteen other federally

regulated mortgage servicers. That review is expected to result

in formal enforcement actions against many or all of the

companies subject to review, which actions are expected to

incorporate remedial requirements, heightened mortgage

servicing standards and potential civil money penalties. In

particular, PNC expects that it will enter into a consent order

with the Federal Reserve and that PNC Bank will enter into a

consent order with the OCC. PNC anticipates that the consent

orders will require, among other things, that PNC undertake

certain actions described below. PNC expects that the orders

will discuss certain purported deficiencies regarding, among

other things, the manner in which PNC Bank handled various

loan servicing activities relating to residential mortgage

foreclosures, the resources and controls for, and risk

management of, such servicing activities and oversight of

certain third-party providers. PNC further expects that the

orders will require commitments regarding a range of

remedial actions, some of which we will already have

undertaken as a result of our recent review of residential

mortgage servicing procedures.

26