PNC Bank 2010 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

employee satisfaction, investing in the business for future

growth, and disciplined expense management during this

period of market and economic uncertainty.

Information for 2010 reflects the impact of the consolidation

in our financial statements of the securitized credit card

portfolio of approximately $1.6 billion of credit card loans as

of January 1, 2010. This consolidation impacted primarily the

loan, borrowings, and other liabilities categories on the

balance sheet and nearly all major categories of our income

statement.

In January 2011, PNC reached a definitive agreement to

acquire 19 branches and the associated deposits from

BankAtlantic Bancorp, Inc. located in the Tampa, Florida

area. The transaction is expected to close in June 2011, subject

to regulatory approval and customary closing conditions. PNC

will convert the branches and customer accounts to the PNC

brand and systems at that time. This transaction is expected to

provide Retail Banking with the opportunity to establish a

foothold in the Tampa area and leverage those branches to

help grow other business activities, such as wealth

management and corporate banking.

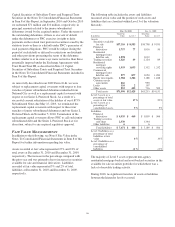

Highlights of Retail Banking’s performance for 2010 include

the following:

• PNC successfully completed the conversion of

customers at over 1,300 branches across nine states

from National City Bank to PNC, providing further

growth opportunities throughout our expanded

footprint.

• Success in implementing Retail Banking’s deposit

strategy resulted in growth in average demand

deposits of $2.3 billion, or 7%, over the prior year.

Excluding approximately $0.7 billion of average

demand deposits from 2009 balances related to the 61

required branch divestitures completed in early

September 2009, average demand deposits increased

$3.0 billion, or 9%, over the prior year.

• For the second consecutive year, the Retail Bank was

named a Gallup Great WorkPlace Award Winner.

PNC was the only U.S. Bank to be recognized. This

recognition reflects our commitment to having an

engaged workforce and a unified culture.

• Implementing the business model in the acquired

markets and building on strengths in the core

franchise resulted in the growth of 75,000 checking

relationships in 2010, a solid gain considering the

first half of the year was dominated by the customer

conversion process and 2010 was a difficult

environment. The majority of this growth came in the

second half of the year as strength in customer

retention from the converted markets was coupled

with sales momentum in channels and products such

as Workplace and University Banking and Virtual

Wallet. Our investment in online banking capabilities

continued to pay off as active online bill payment

customers grew by 25% in 2010.

• PNC’s expansive branch footprint covers nearly

one-third of the U.S. population with a network of

2,470 branches and 6,673 ATM machines at

December 31, 2010. We continued to invest in the

branch network. In 2010, we opened 21 traditional

and 27 in-store branches, and consolidated 91

branches. The decrease in branches was primarily

driven by acquisition-related branch consolidations.

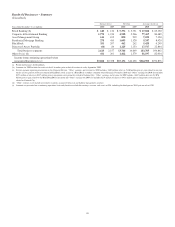

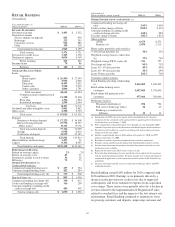

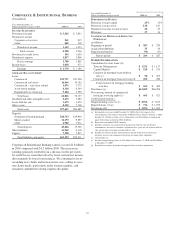

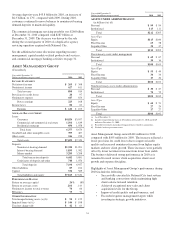

Total revenue for 2010 was $5.4 billion compared with $5.7

billion in 2009. Net interest income of $3.4 billion declined

$89 million compared with 2009. Net interest income was

negatively impacted by lower interest credits assigned to

deposits, reflective of the rate environment, and benefited

from the consolidation of the securitized credit card portfolio,

higher transaction deposits, and increased education loans.

Noninterest income for 2010 was $1.9 billion, a decline of

$256 million over the prior year. The decrease was due to a

decrease in service charges on deposits related to lower

overdraft fees, the negative impact of the consolidation of the

securitized credit card portfolio, lower brokerage fees, and the

impact of the required branch divestitures partially offset by,

higher transaction volume-related fees within consumer

services.

In 2010, Retail Banking revenues were negatively impacted

by the implementation of new federal regulations. These

regulations include: 1) the new rules set forth in Regulation E

related to overdraft fees, 2) the Credit CARD Act of 2009, and

3) the education lending portions of the Health Care and

Education Reconciliation Act of 2010 (HCERA).

The negative impact of Regulation E on revenue for 2010 was

approximately $145 million. Additionally, the Credit CARD

Act had a negative impact on revenue of approximately $75

million, largely in net interest income. These estimates do not

include additional impacts to revenue for other changes that

were made in 2010 responding to market conditions, or other/

additional regulatory requirements, or any offsetting impact of

changes to products and/or pricing.

The education lending business was adversely impacted by

provisions of HCERA that went into effect on July 1, 2010.

The law essentially eliminates the Federal Family Education

Loan Program (FFELP), the federally guaranteed portion of

this business available to private lenders. We originated $2.6

billion of federally guaranteed loans under FFELP in 2009 and

$1.0 billion in 2010, the majority of which were originated in

the first half of the year. We plan to continue to provide

private education loans as another source of funding for

students and families.

Additionally, in 2011 Retail Banking revenue is expected to

continue to be negatively impacted by the rules set forth in

50