PNC Bank 2010 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

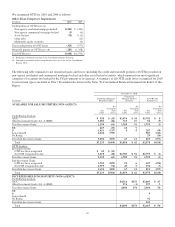

|

|

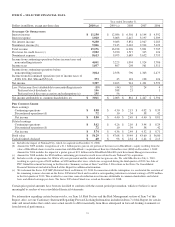

Service charges on deposits totaled $705 million for 2010 and

$950 million for 2009. The decrease in 2010 was due to lower

overdraft charges and required branch divestitures in the third

quarter of 2009. As further discussed in the Retail Banking

section of the Business Segments Review portion of this

Item 7, the new Regulation E rules related to overdraft charges

negatively impacted our 2010 revenue by approximately

$145 million.

Net gains on sales of securities were $426 million for 2010

and $550 million for 2009. OTTI credit losses on securities

recognized in earnings totaled $325 million in 2010 and $577

million in 2009. We expect the level of credit-related OTTI

charges to decline in 2011 compared with 2010.

Gains on BlackRock related transactions included a fourth

quarter 2010 pretax gain of $160 million from our sale of

7.5 million BlackRock common shares as part of a BlackRock

secondary common stock offering. During the fourth quarter

of 2009, we recognized a $1.1 billion pretax gain on PNC’s

portion of the increase in BlackRock’s equity resulting from

the value of BlackRock shares issued by BlackRock in

connection with its acquisition of BGI.

Other noninterest income totaled $884 million for 2010

compared with $987 million for 2009. Other noninterest

income for 2009 included gains of $103 million primarily

related to our BlackRock LTIP shares obligation. Other

noninterest income for 2010 included net gains on private

equity and alternative investments of $258 million, compared

with net losses on private equity and alternative investments

of $93 million in 2009. Gains on sales of loans were

$73 million in 2010 and $220 million in 2009.

Other noninterest income typically fluctuates from period to

period depending on the nature and magnitude of transactions

completed. Further details regarding our trading activities are

included in the Market Risk Management – Trading Risk

portion of the Risk Management section of this Item 7, further

details regarding private equity and alternative investments are

included in the Market Risk Management-Equity And Other

Investment Risk section, and further details regarding gains or

losses related to our equity investment in BlackRock are

included in the Business Segments Review section.

Looking to 2011, we see momentum in our fee-based revenues

resulting from client growth and depth in our expanded

franchise. At the same time, we will see the continued impact

of ongoing regulatory reforms. Excluding the expected

incremental negative impact of two aspects of anticipated

regulatory changes on fees related to Regulation E and

interchange rates of approximately $400 million in 2011 as

further discussed in the Retail Banking section of Business

Segments Review in this Item 7, we expect noninterest

income in 2011 to increase in the low-to-mid single digits

compared with 2010.

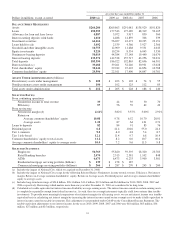

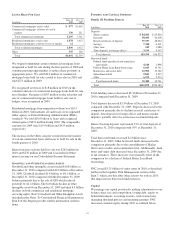

P

RODUCT

R

EVENUE

In addition to credit and deposit products for commercial

customers, Corporate & Institutional Banking offers other

services, including treasury management, commercial real

estate, and capital markets-related products and services that

are marketed by several businesses primarily to commercial

customers.

Treasury management revenue, which includes fees as well as

net interest income from customer deposit balances, totaled

$1.2 billion for 2010 and $1.1 billion for 2009. The increase

was primarily related to deposit growth and continued growth

in purchasing cards and lockbox as well as services provided

to the Federal government and healthcare customers.

Revenue from capital markets-related products and services

totaled $618 million in 2010 compared with $533 million in

2009. The increase was due to higher merger and acquisition

advisory, underwriting and syndications fees, partially offset by

lower gains on loan sales from portfolio management activities.

Commercial mortgage banking activities include revenue

derived from commercial mortgage servicing (including net

interest income and noninterest income from loan servicing

and ancillary services), and revenue derived from commercial

mortgage loans intended for sale and related hedges (including

loan origination fees, net interest income, valuation

adjustments and gains or losses on sales).

Commercial mortgage banking activities resulted in revenue

of $262 million in 2010 compared with $485 million in 2009.

This decline was primarily due to sales of servicing and a

decrease in the net carrying amount of commercial mortgage

servicing rights. These decreases were partially offset by

higher ancillary commercial mortgage servicing fees.

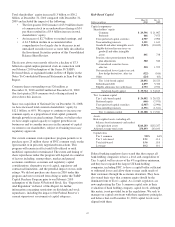

P

ROVISION

F

OR

C

REDIT

L

OSSES

The provision for credit losses totaled $2.5 billion for 2010

compared with $3.9 billion for 2009. The lower provision in

2010 reflected credit exposure reductions and overall

improved credit migration during 2010.

We anticipate an overall improvement in credit migration in

2011 and a continued reduction in our nonperforming loans

assuming modest GDP growth. As a result, we expect that our

average quarterly provision for credit losses in 2011 to be less

than the fourth quarter 2010 provision for credit losses of

$442 million, assuming budgeted loan growth projections. If

our expectations hold, this would result in our full year 2011

provision for credit losses to be at least $800 million less than

our full year 2010 provision for credit losses.

The Credit Risk Management portion of the Risk Management

section of this Item 7 includes additional information regarding

factors impacting the provision for credit losses. See also

Item 1A Risk Factors and the Cautionary Statement Regarding

Forward-Looking Information section of Item 7 of this Report.

32