PNC Bank 2010 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

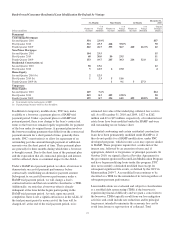

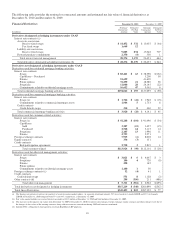

liquidity available to offset projected uses. We calculate

funding gaps for the overnight, thirty-day, ninety-day, one

hundred eighty-day and one-year time intervals. Risk limits

are established within our Liquidity Risk Policy.

Management’s Asset and Liability Committee regularly

reviews compliance with the established limits.

Parent company liquidity guidelines are designed to help

ensure that sufficient liquidity is available to meet our parent

company obligations over the succeeding 24-month period.

Risk limits for parent company liquidity are established within

our Enterprise Capital Management Policy. The Board of

Directors’ Risk Committee regularly reviews compliance with

the established limits.

Bank Level Liquidity – Uses

Obligations requiring the use of liquidity can generally be

characterized as either contractual or discretionary. At the

bank level, primary contractual obligations include funding

loan commitments, satisfying deposit withdrawal requests and

maturities and debt service related to bank borrowings. We

also maintain adequate bank liquidity to meet future potential

loan demand and provide for other business needs, as

necessary.

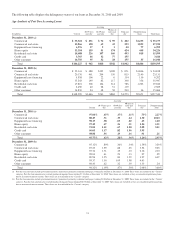

As of December 31, 2010, there were approximately $5.3

billion of bank borrowings with maturities of less than one

year.

Bank Level Liquidity – Sources

Our largest source of bank liquidity on a consolidated basis is

the deposit base that comes from our retail and commercial

businesses. Liquid assets and unused borrowing capacity from

a number of sources are also available to maintain our

liquidity position. Borrowed funds come from a diverse mix

of short and long-term funding sources.

At December 31, 2010, our liquid assets consisted of short-

term investments (Federal funds sold, resale agreements,

trading securities, and interest-earning deposits with banks)

totaling $7.1 billion and securities available for sale totaling

$57.3 billion. Of our total liquid assets of $64.4 billion, we

had $28.0 billion pledged as collateral for borrowings, trust,

and other commitments. The level of liquid assets fluctuates

over time based on many factors, including market conditions,

loan and deposit growth and active balance sheet

management.

In addition to the customer deposit base, which has

historically provided the single largest source of relatively

stable and low-cost funding and liquid assets, the bank also

obtains liquidity through the issuance of traditional forms of

funding including long-term debt (senior notes and

subordinated debt and Federal Home Loan Bank (FHLB)

advances) and short-term borrowings (Federal funds

purchased, securities sold under repurchase agreements,

commercial paper issuances, and other short-term

borrowings).

PNC Bank, N.A. has the ability to offer up to $20 billion in

senior and subordinated unsecured debt obligations with

maturities of more than nine months. Through December 31,

2010, PNC Bank, N.A. had issued $6.9 billion of debt under

this program. Total senior and subordinated debt declined to

$5.5 billion at December 31, 2010 from $7.4 billion at

December 31, 2009 due to maturities.

PNC Bank, N.A. is a member of the FHLB-Pittsburgh and as

such has access to advances from FHLB-Pittsburgh secured

generally by residential mortgage and other mortgage-related

loans. At December 31, 2010, our unused secured borrowing

capacity was $13.0 billion with FHLB-Pittsburgh. Total

FHLB borrowings declined to $6.0 billion at December 31,

2010 from $10.8 billion at December 31, 2009 due to

maturities.

PNC Bank, N.A. has the ability to offer up to $3.0 billion of

its commercial paper. As of December 31, 2010, there were no

issuances outstanding under this program. Commercial paper

included in Other borrowed funds on our Consolidated

Balance Sheet is issued by Market Street as described in

Off-Balance Sheet Arrangements and Variable Interest

Entities in this Financial Review.

PNC Bank, N.A. can also borrow from the Federal Reserve

Bank of Cleveland’s (Federal Reserve Bank) discount window

to meet short-term liquidity requirements. The Federal

Reserve Bank, however, is not viewed as the primary means

of funding our routine business activities, but rather as a

potential source of liquidity in a stressed environment or

during a market disruption. These potential borrowings are

secured by securities and commercial loans. At December 31,

2010, our unused secured borrowing capacity was $24.7

billion with the Federal Reserve Bank.

Parent Company Liquidity – Uses

Obligations requiring the use of liquidity can generally be

characterized as either contractual or discretionary. The parent

company’s contractual obligations consist primarily of debt

service related to parent company borrowings and funding

non-bank affiliates. Additionally, the parent company

maintains adequate liquidity to fund discretionary activities

such as paying dividends to PNC shareholders, share

repurchases, and acquisitions.

As of December 31, 2010, there were approximately $2.3

billion of parent company borrowings with maturities of less

than one year.

78