PNC Bank 2010 Annual Report Download - page 159

Download and view the complete annual report

Please find page 159 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

Statement, including the updated target allocations and

allowable ranges shown below, on August 13, 2008. On

February 25, 2010, the Committee amended the investment

policy to include a dynamic asset allocation approach and also

updated target allocation ranges for certain asset categories.

The long-term investment strategy for pension plan assets is

to:

• Meet present and future benefit obligations to all

participants and beneficiaries,

• Cover reasonable expenses incurred to provide such

benefits, including expenses incurred in the

administration of the Trust and the Plan,

• Provide sufficient liquidity to meet benefit and

expense payment requirements on a timely basis, and

• Provide a total return that, over the long term,

maximizes the ratio of trust assets to liabilities by

maximizing investment return, at an appropriate level

of risk.

Under the dynamic asset allocation strategy, scenarios are

outlined in which the Committee has the ability to make short

to intermediate term asset allocation shifts based on factors

such as the Plan’s funded status, the Committee’s view of

return on equities relative to long term expectations, the

Committee’s view on the direction of interest rates and credit

spreads, and other relevant financial or economic factors

which would be expected to impact the ability of the Trust to

meet its obligation to beneficiaries. Accordingly, the

allowable asset allocation ranges have been updated to

incorporate the flexibility required by the dynamic allocation

policy.

The Plan’s specific investment objective is to meet or exceed

the investment policy benchmark over the long term. The

investment policy benchmark compares actual performance to

a weighted market index, and measures the contribution of

active investment management and policy implementation.

This investment objective is expected to be achieved over the

long term (one or more market cycles) and is measured over

rolling five-year periods. Total return calculations are time-

weighted and are net of investment-related fees and expenses.

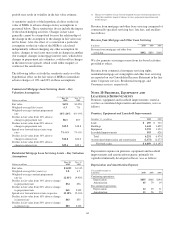

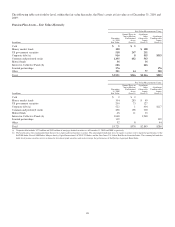

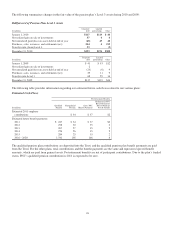

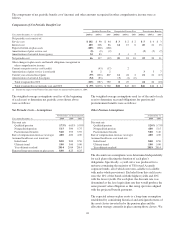

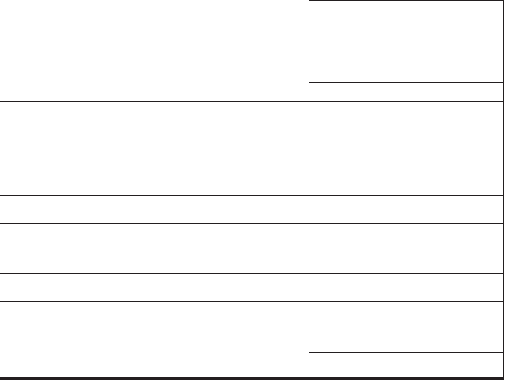

The asset strategy allocations for the Trust at the end of 2010

and 2009, and the target allocation range at the end of 2010,

by asset category, are as follows:

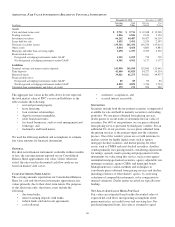

Asset Strategy Allocations

Target

Allocation

Range

Percentage

of Plan

Assets by

Strategy at

December 31

PNC Pension Plan 2010 2009

Asset Category

Domestic Equity 32-38% 40% 39%

International Equity 17-23% 21% 18%

Private Equity 0-8% 2% 2%

Total Equity 40-70% 63% 59%

Domestic Fixed Income 22-28% 24% 29%

High Yield Fixed Income 2-12% 10% 6%

Total Fixed Income 24-40% 34% 35%

Real estate 0-8% 3% 5%

Other 0-1% 0% 1%

Total 100% 100%

The asset category represents the allocation of Plan assets in

accordance with the investment objective of each of the Plan’s

investment managers. Certain domestic equity investment

managers utilize derivatives and fixed income securities as

described in their Investment Management Agreements to

achieve their investment objective under the Investment

Policy Statement. Other investment managers may invest in

eligible securities outside of their assigned asset category to

meet their investment objectives. The actual percentage of the

fair value of total plan assets held as of December 31, 2010 for

equity securities, fixed income securities, real estate and all

other assets are 56%, 36%, 3%, and 5%, respectively.

We believe that, over the long term, asset allocation is the

single greatest determinant of risk. Asset allocation will

deviate from the target percentages due to market movement,

cash flows, investment manager performance and

implementation of shifts under the dynamic allocation policy.

Material deviations from the asset allocation targets can alter

the expected return and risk of the Trust. On the other hand,

frequent rebalancing to the asset allocation targets may result

in significant transaction costs, which can impair the Trust’s

ability to meet its investment objective. Accordingly, the Trust

portfolio is periodically rebalanced to maintain asset

allocation within the target ranges described above.

In addition to being diversified across asset classes, the Trust

is diversified within each asset class. Secondary

diversification provides a reasonable basis for the expectation

that no single security or class of securities will have a

disproportionate impact on the total risk and return of the

Trust.

The Committee selects investment managers for the Trust

based on the contributions that their respective investment

151