PNC Bank 2010 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

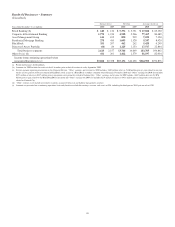

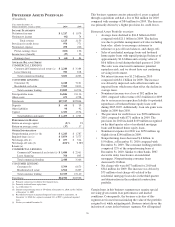

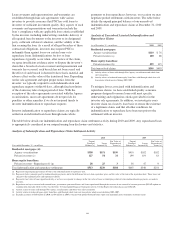

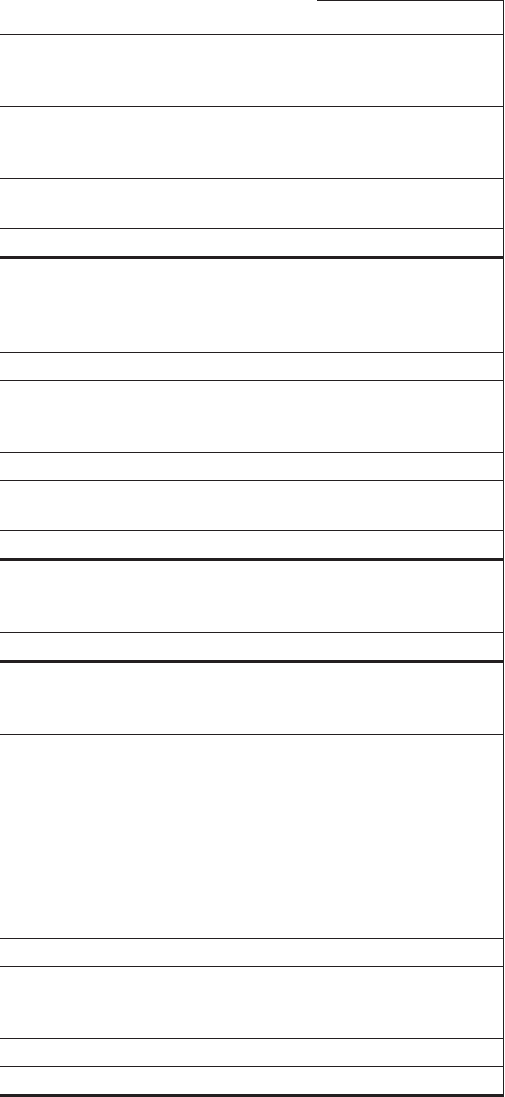

|

|

D

ISTRESSED

A

SSETS

P

ORTFOLIO

(Unaudited)

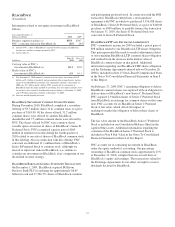

Year ended December 31

Dollars in millions, except as noted 2010 2009

I

NCOME

S

TATEMENT

Net interest income $ 1,217 $ 1,079

Noninterest income (92) 74

Total revenue 1,125 1,153

Provision for credit losses 976 771

Noninterest expense 250 246

Pretax earnings (loss) (101) 136

Income taxes (benefit) (37) 52

Earnings (loss) $ (64) $84

A

VERAGE

B

ALANCE

S

HEET

COMMERCIAL LENDING:

Commercial/Commercial real estate (a) $ 2,240 $ 3,384

Lease financing 781 818

Total commercial lending 3,021 4,202

CONSUMER LENDING:

Consumer (b) 6,240 7,101

Residential real estate 7,585 9,813

Total consumer lending 13,825 16,914

Total portfolio loans 16,846 21,116

Other assets 671 1,728

Total assets $17,517 $22,844

Deposits $64 $39

Other liabilities 90 92

Capital 1,321 1,574

Total liabilities and equity $ 1,475 $ 1,705

P

ERFORMANCE

R

ATIOS

Return on average capital (5)% 5%

Return on average assets (.37) .37

O

THER

I

NFORMATION

Nonperforming assets (c) (d) $ 1,243 $ 1,787

Impaired loans (c) (e) $ 5,879 $ 7,577

Net charge-offs (f) $ 677 $ 544

Net charge-off ratio (f) 4.02% 2.58%

L

OANS

(c)

COMMERCIAL LENDING

Commercial/Commercial real estate (a) $ 1,684 $ 2,561

Lease financing 764 805

Total commercial lending 2,448 3,366

CONSUMER LENDING

Consumer (b) 5,769 6,673

Residential real estate 6,564 8,467

Total consumer lending 12,333 15,140

Total loans $14,781 $18,506

(a) Primarily commercial residential development loans.

(b) Primarily brokered home equity loans.

(c) As of December 31.

(d) Includes nonperforming loans of $.9 billion at December 31, 2010 and $1.5 billion

at December 31, 2009.

(e) Recorded investment of purchased impaired loans related to acquisitions. At

December 31, 2010, this segment contained 76% of PNC’s purchased impaired

loans.

(f) For the year ended December 31.

This business segment consists primarily of assets acquired

through acquisitions and had a loss of $64 million for 2010

compared with earnings of $84 million for 2009. The decrease

was primarily driven by a higher provision for credit losses.

Distressed Assets Portfolio overview:

• Average loans declined to $16.8 billion in 2010

compared with $21.1 billion in 2009. The decline

was due to portfolio management activities including

loan sales, efforts to encourage customers to

refinance or pay off loan balances, and charge-offs.

• Sales of residential mortgage loans and brokered

home equity loans with unpaid principal balances of

approximately $1.6 billion and carrying value of

$0.6 billion closed during the third quarter of 2010.

The sales were structured to minimize potential

repurchase risk, and we do not have any continuing

servicing involvement.

• Net interest income was $1.2 billion in 2010

compared with $1.1 billion for 2009. The increase

was driven by improved cash collection results on

impaired loans which more than offset the decline in

average loans.

• Noninterest income was a loss of $92 million for

2010 compared with revenue of $74 million for 2009

due to an increase in repurchase liability for potential

repurchases of brokered home equity loans sold

during 2005-2007. Additionally, loan sale gains were

higher in 2009 than 2010.

• The provision for credit losses was $976 million in

2010 compared with $771 million in 2009. The

provision for 2010 included $109 million recognized

on the third quarter sales of residential mortgage

loans and brokered home equity loans.

• Noninterest expense for 2010 was $250 million, up

slightly from $246 million in 2009.

• Nonperforming loans decreased $.6 billion, to

$.9 billion, at December 31, 2010 compared with

December 31, 2009. The consumer lending portfolio

comprised 52% of the nonperforming loans at

December 31, 2010. Similar to other banks, PNC

elected to delay foreclosures on residential

mortgages. Nonperforming consumer loans

decreased $.3 billion.

• Net charge-offs were $677 million for 2010 and

$544 million for 2009. The increase was driven by

$75 million of net charge-offs related to the

residential mortgage loan sales in the third quarter

and deterioration in the residential construction

portfolio.

Certain loans in this business segment may require special

servicing given current loan performance and market

conditions. Consequently, the business activities of this

segment are focused on maximizing the value of the portfolio

assigned to it while mitigating risk. Business intent drives the

inclusion of assets in this business segment. Not all impaired

58