PNC Bank 2010 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

counterparties whose aggregate exposure is material in relation

to our total credit exposure. At December 31, 2010, no specific

industry concentration exceeded 6% of total commercial

lending loans outstanding.

We originate interest-only loans to commercial borrowers.

This is usually to match our borrowers’ asset conversion to

cash expectations (i.e., working capital lines, revolvers). These

products are standard in the financial services industry and are

considered during the underwriting process to mitigate the

increased risk that may result in borrowers not being able to

make interest and principal payments when due. We do not

believe that these product features create a concentration of

credit risk.

In the normal course of business, we originate or purchase loan

products with contractual features, when concentrated, that

may increase our exposure as a holder of those loan products.

Possible product features that may create a concentration of

credit risk would include a high LTV ratio, terms that may

expose the borrower to future increases in repayments above

increases in market interest rates, below-market interest rates

and interest-only loans, among others. We also originate home

equity loans and lines of credit that are concentrated in our

primary geographic markets.

At December 31, 2010, we pledged $12.6 billion of loans to

the Federal Reserve Bank and $32.4 billion of loans to the

Federal Home Loan Bank as collateral for the contingent

ability to borrow, if necessary. The comparable amounts at

December 31, 2009 were $18.8 billion and $32.6 billion,

respectively.

Certain loans are accounted for at fair value with changes in

the fair value reported in current period earnings. The fair

value of these loans was $116 million, or less than 1% of the

total loan portfolio, at December 31, 2010 compared with

$107 million, or less than 1% of the total loan portfolio, at

December 31, 2009.

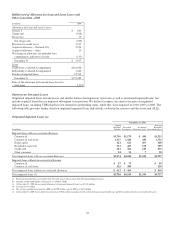

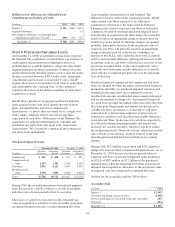

Net Unfunded Credit Commitments

In millions

December 31

2010

December 31

2009

Commercial and commercial real estate $59,256 $ 60,143

Home equity lines of credit 19,172 20,367

Consumer credit card lines 14,725 17,558

Other 2,652 2,727

Total $95,805 $100,795

Commitments to extend credit represent arrangements to lend

funds or provide liquidity subject to specified contractual

conditions. At December 31, 2010, commercial commitments

reported above exclude $16.7 billion of syndications,

assignments and participations, primarily to financial

institutions. The comparable amount at December 31, 2009

was $13.2 billion.

Commitments generally have fixed expiration dates, may

require payment of a fee, and contain termination clauses in

the event the customer’s credit quality deteriorates. Based on

our historical experience, most commitments expire unfunded,

and therefore cash requirements are substantially less than the

total commitment.

N

OTE

5A

SSET

Q

UALITY AND

A

LLOWANCES FOR

L

OAN AND

L

EASE

L

OSSES AND

U

NFUNDED

L

OAN

C

OMMITMENTS AND

L

ETTERS OF

C

REDIT

A

LLOWANCE FOR

L

OAN AND

L

EASE

L

OSSES

We maintain the ALLL at a level that we believe to be

adequate to absorb estimated probable credit losses incurred in

the loan portfolio as of the balance sheet date.

One of the key factors for determining the performing status of a

loan is delinquency. The measurement of delinquency is based

on the contractual terms of each loan. Loans that are 30 days or

more past due in terms of payment are considered delinquent.

See Note 1 Accounting Policies – Nonperforming Assets for

additional delinquency, nonaccrual, and charge-off information.

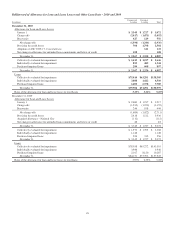

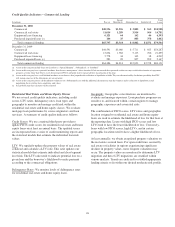

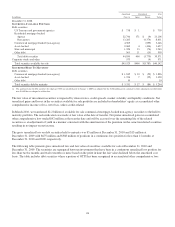

The following table displays the delinquency status of our loans at December 31, 2010.

Age Analysis of Past Due Accruing Loans

Accruing

In millions Current

30-59 days

past due

60-89 days

past due

90 days or

more past due (b)

Total past

due

Nonperforming

loans (c) Total loans

December 31, 2010 (a)

Commercial $ 53,522 $251 $ 92 $ 59 $ 402 $1,253 $ 55,177

Commercial real estate 15,866 128 62 43 233 1,835 17,934

Equipment lease financing 6,276 37 2 1 40 77 6,393

Home equity 33,354 159 91 174 424 448 34,226

Residential real estate 14,688 226 107 160 493 818 15,999

Credit card 3,765 46 32 77 155 3,920

Other consumer 16,756 95 32 28 155 35 16,946

Total $144,227 $942 $418 $542 $1,902 $4,466 $150,595

118