PNC Bank 2010 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

• Customer demand for other products and services,

• Changes in the competitive and regulatory landscape

and in counterparty creditworthiness and

performance as the financial services industry

restructures in the current environment,

• The impact of the extensive reforms enacted in the

Dodd-Frank legislation and other legislative,

regulatory and administrative initiatives, including

those outlined above, and

• The impact of market credit spreads on asset

valuations.

In addition, our success will depend, among other things,

upon:

• Further success in the acquisition, growth and

retention of customers,

• Continued development of the geographic markets

related to our recent acquisitions, including full

deployment of our product offerings,

• Revenue growth,

• A sustained focus on expense management, and

creating positive pre-tax, pre-provision earnings,

• Managing the distressed assets portfolio and other

impaired assets,

• Improving our overall asset quality and continuing to

meet evolving regulatory capital standards,

• Continuing to maintain and grow our deposit base as

a low-cost funding source,

• Prudent risk and capital management related to our

efforts to return to our desired moderate risk profile,

and

• Actions we take within the capital and other financial

markets.

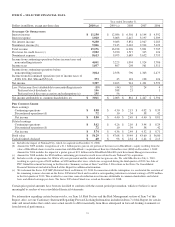

S

UMMARY

F

INANCIAL

R

ESULTS

2010 2009

Net income (millions) $3,397 $2,403

Diluted earnings per common share

Continuing operations $ 5.02 $ 4.26

Discontinued operations .72 .10

Net income $ 5.74 $ 4.36

Return from net income on:

Average common shareholders’ equity 10.88% 9.78%

Average assets 1.28% .87%

Our performance in 2010 included the following:

• Net income for 2010 of $3.4 billion was a record, up

41% from 2009.

• Net interest income of $9.2 billion for 2010 was up

2% from 2009, while the net interest margin rose to

4.14% in 2010 compared with 3.82% for 2009.

• Noninterest income of $5.9 billion in 2010 declined

$1.2 billion compared with 2009. On December 1,

2009, BlackRock acquired Barclays Global Investors

(BGI) from Barclays Bank PLC. PNC recognized a

pretax gain of $1.1 billion, or $687 million after

taxes, in the fourth quarter of 2009 related to this

transaction. Additional information regarding this

transaction is included within the BlackRock section

of our Business Segments Review section of this

Item 7.

• The provision for credit losses declined to $2.5 billion

in 2010 compared with $3.9 billion in 2009 as overall

credit quality continued to improve and as we took

actions to reduce exposure levels during the year.

• Noninterest expense for 2010 declined by 5%

compared with 2009, to $8.6 billion. We were

successful in achieving our acquisition cost savings

goal of $1.8 billion on an annualized basis in the

fourth quarter of 2010, well ahead of the original

target amount and schedule. We also continued to

invest in customer growth and innovation initiatives.

• Overall credit quality continued to improve during

2010. Nonperforming assets declined $1.0 billion to

$5.3 billion as of December 31, 2010 from

December 31, 2009. Accruing loans past due

decreased $1.4 billion, or 42%, during 2010 to $1.9

billion at year end. The allowance for loan and lease

losses (ALLL) was $4.9 billion, or 3.25% of total

loans and 109% of nonperforming loans, as of

December 31, 2010.

• We remain committed to responsible lending to

support economic growth. Loans and commitments

originated and renewed totaled approximately $149

billion for 2010, including $3.5 billion of small

business loans. Total loans were $150.6 billion at

December 31, 2010, a decline of 4% from $157.5

billion at December 31, 2009.

• Total deposits were $183.4 billion at December 31,

2010 compared with $186.9 billion at the prior year

end. Growth in transaction deposits (money market

and demand) continued with an increase of $8.4

billion, or 7%, for the year. Higher cost retail

certificates of deposit were reduced by $11.3 billion,

or 23%, during 2010.

• Our transition to a higher quality balance sheet

during 2010 reflected core funding with a loan to

deposit ratio of 82% at year end and a strong bank

liquidity position to support growth.

• We sold 7.5 million BlackRock common shares for a

pretax gain of $160 million as part of BlackRock’s

secondary common stock offering in November 2010

with the effect of reducing PNC’s economic interest

in BlackRock to approximately 20% from 24% prior

to the offering.

• We grew common equity by $7.6 billion during

2010. The Tier 1 common capital ratio was 9.8% at

December 31, 2010, up 380 basis points from

December 31, 2009.

Our Consolidated Income Statement Review section of this

Item 7 describes in greater detail the various items that

impacted our results for 2010 and 2009.

28