PNC Bank 2010 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

During 2010 and 2009, unresolved and settled investor

indemnification and repurchase claims were primarily related

to one of the following alleged breaches in representations and

warranties: 1) misrepresentation of income, assets or

employment; 2) property evaluation or status issues (e.g.,

appraisal, title, etc.); or 3) underwriting guideline violations.

Additionally during these years, the frequency and timing of

unresolved and settled investor indemnification and

repurchase claims increased as a result of higher loan

delinquencies which have been impacted by the deterioration

in the overall economy and the prolonged weak residential

housing sector. The increased volume of claims was also

reflective of an industry trend where investors implemented

certain strategies to aggressively reduce their exposure to

losses on purchased loans.

For the first and second-lien mortgage balances of unresolved

and settled claims contained in the tables above, a significant

amount of these claims were associated with sold loans

originated through correspondent lender and broker

origination channels. For the home equity loans/lines sold

portfolio, all unresolved and settled claims relate to loans

originated through the broker origination channel. In certain

instances when indemnification or repurchase claims are

settled for these types of sold loans, we have recourse back to

the correspondent lenders, brokers and other third-parties

(e.g., contract underwriting companies, closing agents,

appraisers, etc.). Depending on the underlying reason for the

investor claim, we determine our ability to pursue recourse

with these parties and file claims with them accordingly. Our

historical recourse recovery rate has been insignificant as our

efforts have been impacted by the inability of such parties to

reimburse us for their recourse obligations (e.g., their capital

availability or whether they remain in business) or contractual

limitations that limit our ability to pursue recourse with these

parties (e.g., loss caps, statutes of limitations, etc.). All of

these factors are considered in the determination of our

estimated indemnification and repurchase liability detailed

below.

Origination and sale of residential mortgages is an ongoing

business activity and, accordingly, management continually

assesses the need for indemnification and repurchase liabilities

pursuant to the associated investor sale agreements. We

establish indemnification and repurchase liabilities for

estimated losses on sold first and second-lien mortgages and

home equity loans/lines for which indemnification is expected

to be provided or for loans that are expected to be

repurchased. For the first and second-lien mortgage sold

portfolio, we have established an indemnification and

repurchase liability pursuant to investor sale agreements based

on claims made and our estimate of future claims on a loan by

loan basis. These relate primarily to loans originated during

2006-2008. For the home equity loans/lines sold portfolio, we

have established indemnification and repurchase liabilities

based upon this same methodology for loans sold during

2005-2007.

Indemnification and repurchase liabilities are initially

recognized when loans are sold to investors and are

subsequently evaluated for adequacy by management. Initial

recognition and subsequent adjustments to the indemnification

and repurchase liability for the first and second-lien mortgage

sold portfolio are recognized in Residential mortgage revenue

on the Consolidated Income Statement. Since PNC is no

longer engaged in the brokered home equity lending business,

only subsequent adjustments are recognized to the home

equity loans/lines indemnification and repurchase liability.

These adjustments are recognized in other noninterest income

on the Consolidated Income Statement.

Management’s subsequent evaluation of these indemnification

and repurchase liabilities is based upon trends in

indemnification and repurchase requests, actual loss

experience, known and inherent risks in the underlying

serviced loan portfolios, and current economic conditions. As

part of its evaluation, management considers estimated loss

projections over the life of the subject loan portfolio. At

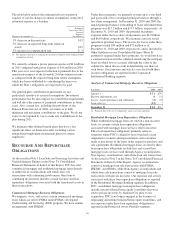

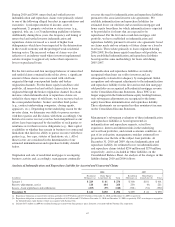

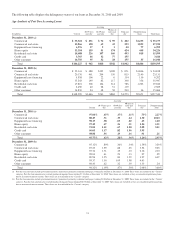

December 31, 2010 and 2009, the total indemnification and

repurchase liability for estimated losses on indemnification

and repurchase claims totaled $294 million and $270 million,

respectively, and was included in Other liabilities on the

Consolidated Balance Sheet. An analysis of the changes in this

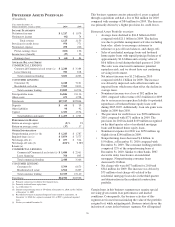

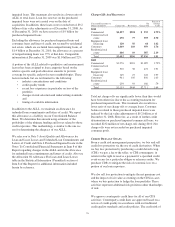

liability during 2010 and 2009 follows:

Analysis of Indemnification and Repurchase Liability for Asserted and Unasserted Claims

2010 2009

In millions

Residential

Mortgages (a)

Home Equity

Loans/Lines (b) Total

Residential

Mortgages (a)

Home Equity

Loans/Lines (b) Total

January 1 $ 229 $ 41 $ 270 $ 300 $101 $ 401

Reserve adjustments, net (c) 120 144 264 230 (9) 221

Losses – loan repurchases and settlements (205) (35) (240) (301) (51) (352)

December 31 $ 144 $150 $ 294 $ 229 $ 41 $ 270

(a) Repurchase obligation associated with sold loan portfolios of $139.8 billion and $157.2 billion at December 31, 2010 and December 31, 2009, respectively.

(b) Repurchase obligation associated with sold loan portfolios of $6.5 billion and $7.5 billion at December 31, 2010 and December 31, 2009, respectively. PNC is no longer in engaged in

the brokered home equity business which was acquired with National City.

(c) Includes $157 million in 2009 for residential mortgages related to the final purchase price allocation associated with the National City acquisition.

67