PNC Bank 2010 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

B

ALANCE

S

HEET

H

IGHLIGHTS

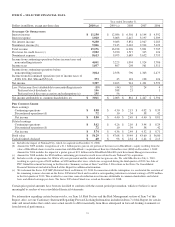

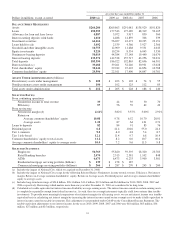

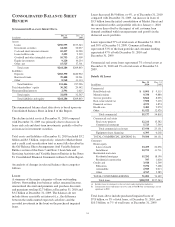

Total assets were $264.3 billion at December 31, 2010

compared with $269.9 billion at December 31, 2009. The

decline from year end 2009 resulted from a decline in loans,

other assets and short-term investments and cash somewhat

offset by an increase in investment securities.

Various seasonal and other factors impact our period-end

balances whereas average balances are generally more

indicative of underlying business trends apart from the impact

of acquisitions, divestitures and consolidations of variable

interest entities.

The Consolidated Balance Sheet Review section of this Item 7

provides information on changes in selected Consolidated

Balance Sheet categories at December 31, 2010 compared

with December 31, 2009.

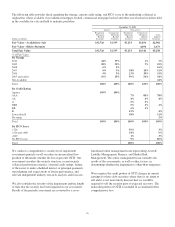

Total average assets were $264.9 billion for 2010 compared

with $276.9 billion for 2009.

Average interest-earning assets were $224.7 billion for 2010,

compared with $238.5 billion in 2009. Decreases of $11.9

billion in loans and $6.5 billion in other interest-earning

assets, partially offset by a $5.7 billion increase in investment

securities, drove the decrease in this comparison.

The decrease in average total loans reflected a decline in

commercial loans of $6.8 billion, commercial real estate loans

of $4.3 billion and residential mortgage loans of $3.4 billion,

partially offset by an increase of $2.6 billion in consumer

loans. Loans represented 68% of average interest-earning

assets for 2010 and 69% for 2009.

Average securities available for sale increased $2.7 billion, to

$50.8 billion, in 2010 compared with 2009. Average US

Treasury and government agencies securities increased

$3.1 billion while agency residential mortgage-backed

securities increased $1.5 billion and other debt securities

increased $1.5 billion in the comparison. These increases were

partially offset by a decline of $2.8 billion in average

non-agency residential mortgage-backed securities and a

decline of $1.1 billion in commercial mortgage-backed

securities.

Average securities held to maturity increased $3.0 billion, to

$7.2 billion, in 2010 compared with 2009. The increase

reflected purchases of asset-backed and non-agency

commercial mortgage-backed securities, the transfer of

non-agency commercial mortgage-backed securities from the

available for sale portfolio, and the impact of the Market

Street Funding LLC (Market Street) consolidation effective

January 1, 2010.

Total investment securities comprised 26% of average

interest-earning assets for 2010 and 22% for 2009.

Average noninterest-earning assets totaled $40.2 billion in

2010 compared with $38.4 billion in the prior year period.

Average total deposits were $181.9 billion for 2010 compared

with $189.9 billion for 2009. Average deposits declined from

the prior year period primarily as a result of decreases in retail

certificates of deposit and other time deposits, which were

partially offset by an increase in transaction deposits. Average

transaction deposits were $128.4 billion for 2010 compared

with $120.2 billion for 2009 reflecting our strategy to grow

demand and money market deposits. Total deposits at

December 31, 2010 were $183.4 billion compared with $186.9

billion at December 31, 2009 and are further discussed within

the Consolidated Balance Sheet Review section of this Report.

Average total deposits represented 69% of average total assets

for both 2010 and 2009.

Average borrowed funds were $40.2 billion for 2010

compared with $44.1 billion for 2009. A $6.2 billion decline

in Federal Home Loan Bank borrowings drove the decline in

the comparison, partially offset by higher average commercial

paper borrowings that reflected the consolidation of Market

Street.

Total borrowed funds at December 31, 2010 were $39.5

billion compared with $39.3 billion at December 31, 2009 and

are further discussed within the Consolidated Balance Sheet

Review section of this Item 7. In addition, the Liquidity Risk

Management portion of the Risk Management section of this

Item 7 includes additional information regarding our sources

and uses of borrowed funds.

29